Roland Berger’s 2025 Q3 North American light vehicle xEV forecast

North American light vehicle electrification in flux

Market realities and strategic pivots post-regulatory reset

Roland Berger’s 2026 Q1 North American light vehicle xEV update

The North American light vehicle electrification landscape is being reshaped by a series of decisive policy changes. The US administration has continued to repeal key regulations and incentives supporting light vehicle electrification , fundamentally altering the market environment. As a result, the industry has witnessed an immediate impact in EV sales, with the loss of major subsidies in the US leading to significant declines in adoption. In parallel, OEMs are actively shifting their powertrain strategies – scaling back battery electric vehicle programs and accelerating investment in hybrids and extended range electric vehicles. At the same time, China’s role in North American electrification is evolving, as both governments and automakers explore new partnerships and supply chain opportunities to address affordability and competitiveness.

Regulatory reset: A new policy environment

In early 2026, the US administration continued its efforts to remove regulatory support for automotive electrification. As part of this ongoing policy direction, the Environmental Protection Agency (EPA) rescinded its 2009 Endangerment Finding, which had served as the legal foundation for federal greenhouse gas (GHG) vehicle standards. This move effectively removed the EPA’s authority to regulate vehicle GHG emissions under Section 202(a) of the Clean Air Act. In parallel, the Trump administration introduced the “Freedom Means Affordable Cars” (SAFE III) proposal, which retroactively resets Corporate Average Fuel Economy (CAFE) standards to model year 2022 levels. As a result, fuel economy targets for 2031 are now nearly half of what was planned under the Biden administration. Additionally, most crossovers and small SUVs have been reclassified as “passenger cars,” which eases compliance requirements for automakers.

Canada has also shifted its regulatory approach. The national zero-emission vehicle (ZEV) sales mandate was repealed and replaced by a quota-based system. At the same time, the Canadian government introduced the CAD 2.3 billion EV Affordability Program, which offers up to CAD 5,000 for battery electric vehicles (BEVs) and CAD 2,500 for plug-in hybrids (PHEVs) priced under CAD 50,000. Furthermore, tariffs on 49,000 Chinese EVs per year were reduced from 100% to 6.1%, increasing access to affordable BEVs for Canadian consumers.

Market impact: BEV and hybrid sales under pressure

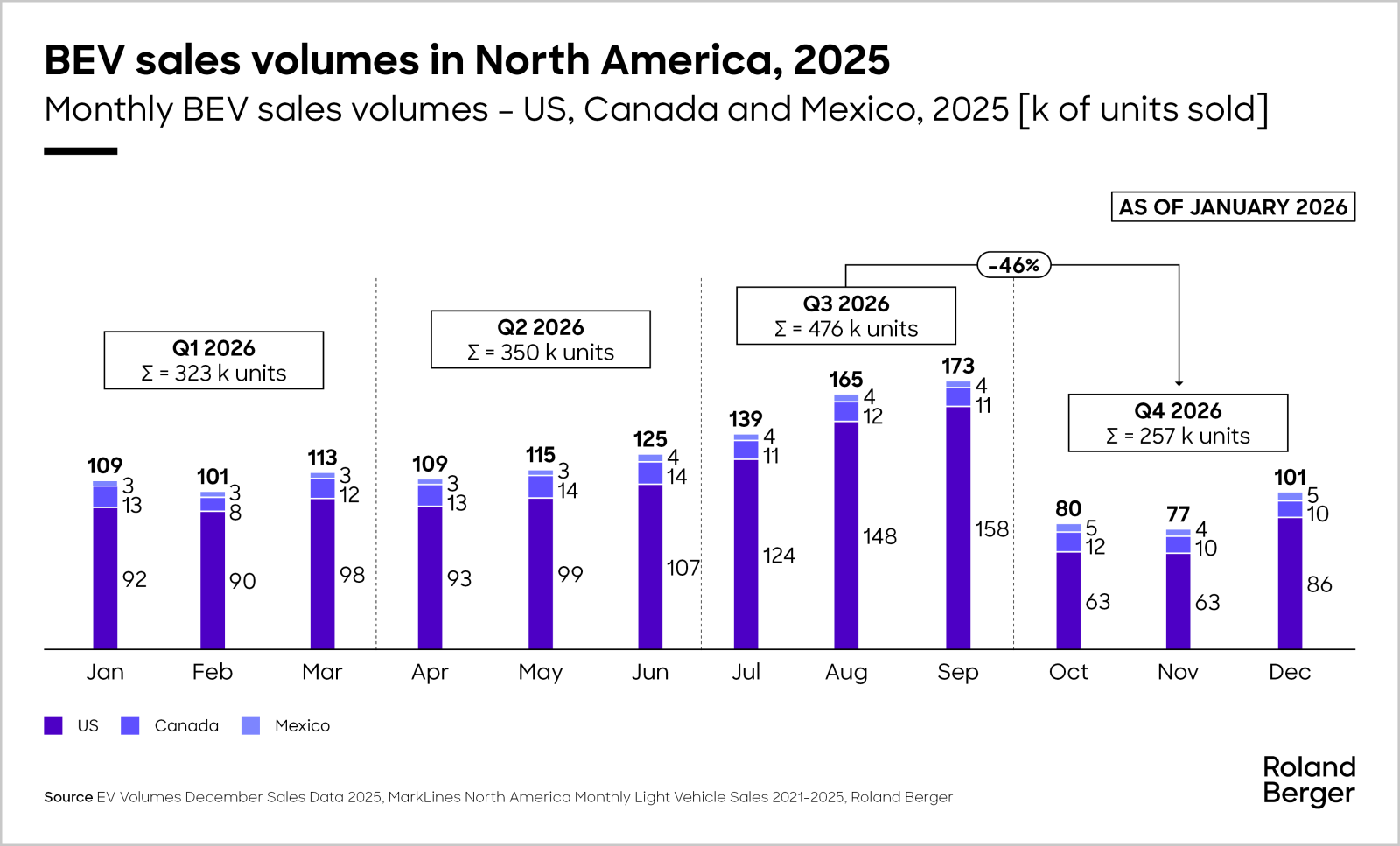

This quarter the US market began to see the impact of previously enacted changes in regulations (e.g., repeal of IRA 30D tax credits). The result of the loss of these incentives was immediate and significant. Battery electric vehicle (BEV) sales in North America experienced a significant decline following the rollback of US federal tax credits in late 2025. In the United States, BEV sales dropped by approximately 51% quarter-over-quarter in Q4 2025, after a brief surge as consumers accelerated purchases ahead of the subsidy expiration. Across North America, BEV sales fell by 46% in the same period. In contrast, Mexico saw continued growth in BEV adoption, driven by the entry of new Chinese brands and favorable trade policies that increased the availability of affordable electric vehicles.

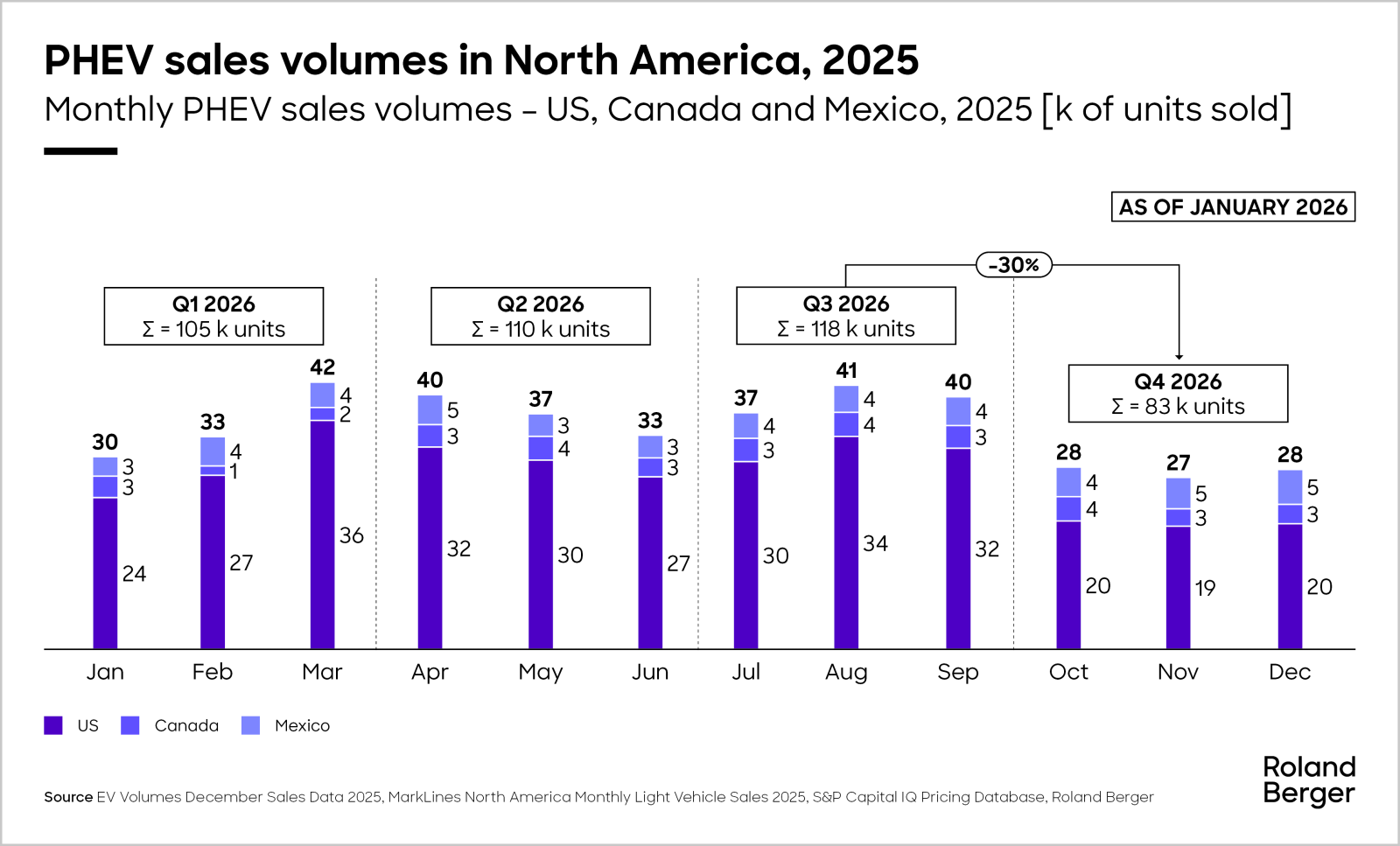

Plug-in hybrid electric vehicle (PHEV) sales followed a similar pattern, with notable declines in the US and Canada. In the United States, PHEV sales fell by 30% in Q4 2025, with the decline amplified by consumers pulling forward purchases before the credits ended. Meanwhile, Mexico experienced a surge in PHEV adoption, supported by the arrival of new market entrants and policies that favored electrified vehicles.

OEM responses and strategy shifts

Meanwhile, automakers have responded decisively to these market shifts and regulatory changes. Major OEMs – including Ford, GM, Stellantis, Honda, and Volkswagen – have written down approximately $73 billion in EV-related investments, canceled planned BEV launches, and shifted their focus toward hybrids and extended range electric vehicles (EREVs). Many companies are dissolving battery joint ventures, delaying BEV programs, and prioritizing multi-powertrain portfolios to hedge against ongoing regulatory and demand uncertainty.

As a result, the number of hybrid models produced in North America is forecasted to more than double by 2033, with 71 PHEV/EREV and 69 full/mild hybrid models expected. EREVs, which offer electric-first driving with the reassurance of a gasoline engine for extended range, are projected to reach approximately 6% of North American xEV production by 2033. This segment is gaining traction due to its ability to leverage BEV platforms, reduce costs, and address consumer concerns about range and charging infrastructure. Automakers such as Stellantis, Hyundai-Kia, Volkswagen, and Ford are investing in EREV architectures, with new models set to launch from 2026 onward.

China’s evolving role in North American electrification

The role of China in North American electrification is also changing rapidly. The Canadian government has lowered trade barriers for Chinese EVs, and the US is considering similar moves, provided that Chinese automakers invest in local manufacturing and job creation. At the same time, North American OEMs are deepening their partnerships with Chinese companies. For example, Ford is in talks with BYD to source batteries for hybrids, Stellantis is introducing Leapmotor models in Mexico, and Rivian has selected a Chinese supplier for LiDAR technology. These partnerships could accelerate electrification, lower costs, and expand supply chain options for North American automakers.

Implications and next steps for OEMs and suppliers

With regulatory support waning and BEV demand under pressure, OEMs should reassess electrification strategies segment-by-segment and ground powertrain decisions at the program-level to clear customer value propositions. To avoid repeating past overinvestment cycles, the current pivot toward hybrids and EREVs should be approached with discipline, without assuming sustained demand. At the same time, as competitiveness becomes increasingly cost-driven, OEMs should accelerate cost-down efforts, including adoption of lower-cost battery solutions, simplification of vehicle architectures, and leaner operating models enabled by AI and other next-generation tools.

Suppliers face a more structural reset. As OEM priorities shift and programs are delayed or canceled, portfolio focus must tighten around platforms with credible volume visibility. Risk management should be embedded more explicitly into product planning and quoting for electrified solutions, reflecting heightened demand volatility, program uncertainty, and pricing pressure. This also requires an honest reassessment of where to participate in electrification, particularly where expected volumes may no longer support a scalable and profitable business.

Across the value chain, prior assumptions on electrified volumes and timelines should be revisited. At the same time, the evolving role of China presents both a cost lever and a strategic risk; targeted, compliant partnerships should be explored to improve access to technology and affordability while navigating regulatory constraints. As the industry recalibrates, those who combine rigorous capital allocation and strict program discipline will set themselves apart from competitors who remain tied to outdated electrification strategies.

Sign up for our newsletter

Further readings