The global chemicals sector is entering a period of profound disruption, not from the next breakthrough in material science, but from the unrelenting industrial scale of China’s production machine.

Europe’s chemical industry structural reset

How can companies adapt to the new European reality

The European chemical industry is undergoing a fundamental transformation driven by a convergence of structural forces. Weak domestic demand, combined with limited market pull for sustainable and low‑carbon solutions, is weighing on growth. At the same time, persistently low-capacity utilization across Europe contrasts sharply with rising imports from China, fuelled by global overcapacity. These pressures are compounded by significantly higher energy costs, which continue to erode Europe’s global competitiveness.

Regulatory developments add another layer of complexity. The European Union is advancing impactful regulations - including the Emissions Trading System (ETS1). While the system is currently under review, it remains designed to phase out free carbon allowances by 2039, without yet providing sufficient mechanisms to safeguard European industry or ensure a level playing field. Taken together, these dynamics are placing unprecedented strain on chemical producers across the region, leaving many with little choice but to take decisive and often difficult actions. The impact is already visible.

"This is no longer a normal cyclical downturn. Energy costs, overcapacity, regulatory pressure, and uncertain demand are structurally undermining Europe’s investment case. Understandably, companies are initiating far-reaching transformations, with many decisions being irreversible."

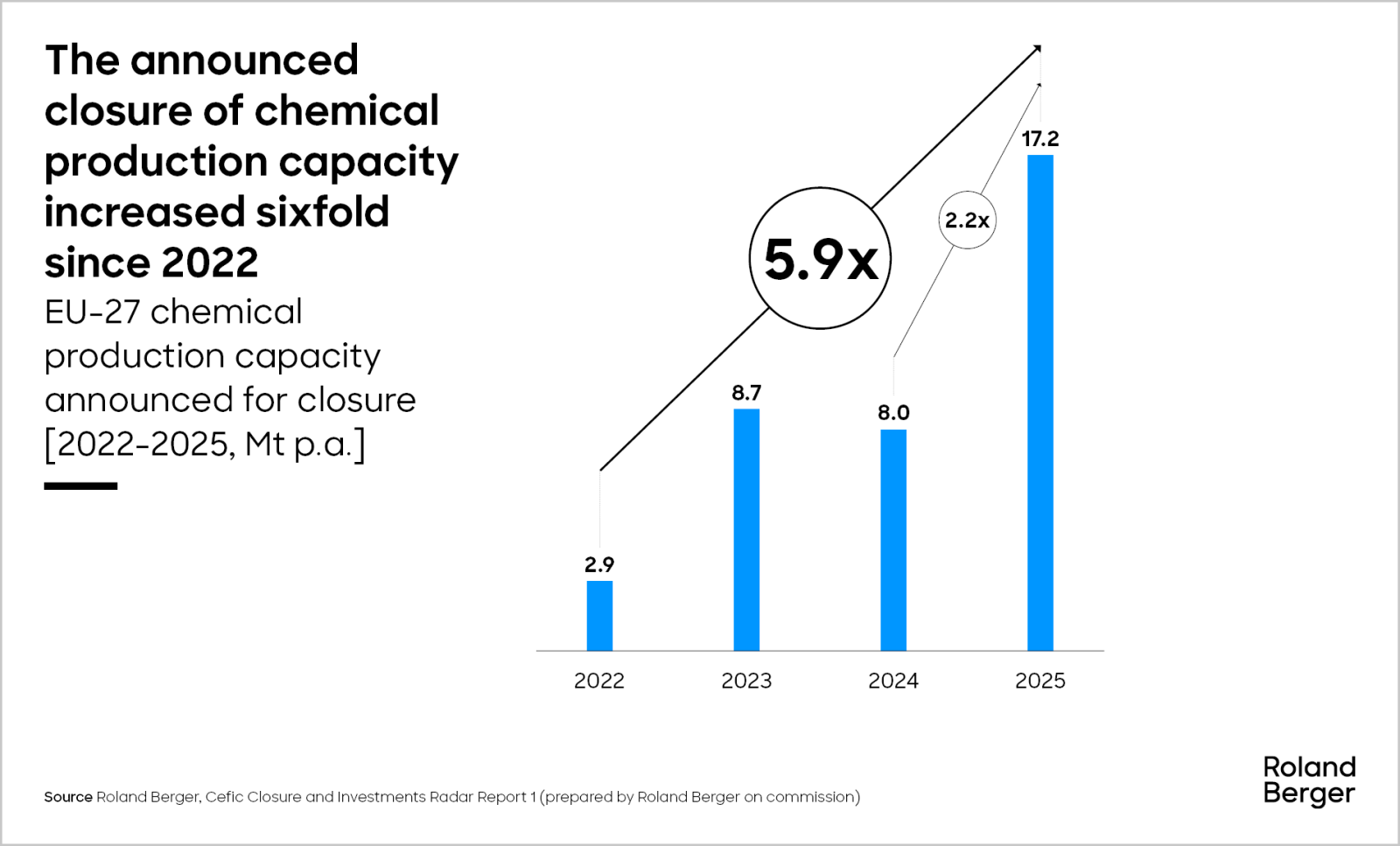

From 2022 to 2025, announced capacity closures increased sixfold to nearly 37 million tons, while new investment announcements have dropped sharply, resulting in a shrinking industrial footprint and a net capacity loss of over 30 million tons. This structural reset is not a temporary downturn but signals a decisive moment for the industry.

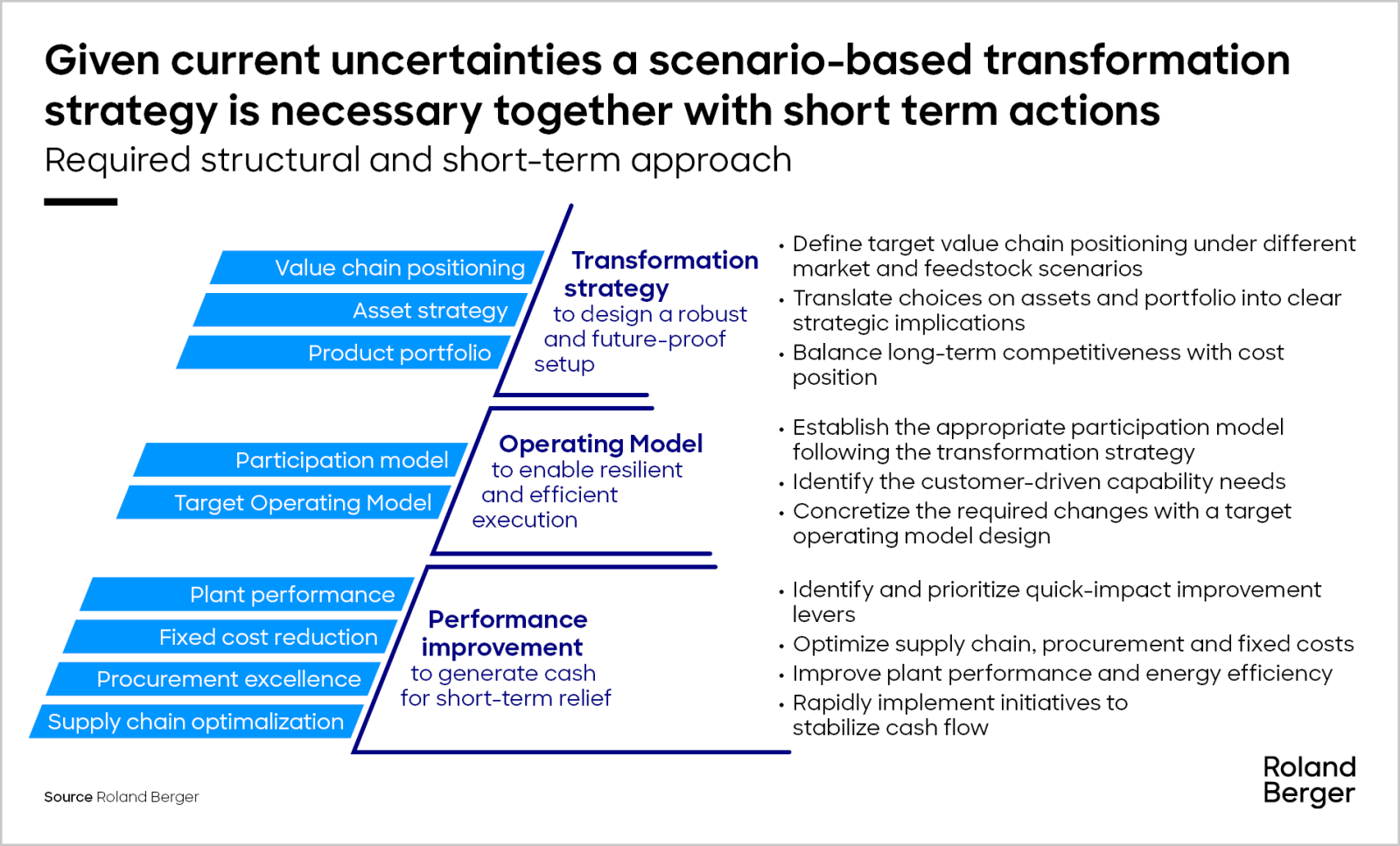

Against this backdrop, companies must navigate deep uncertainty: Will Europe remain an open market or move toward greater protection? Will the transition to a green economy accelerate or slow under economic pressure? To remain competitive and resilient, chemical companies must act across three critical dimensions. (1) Strategically, they must develop a robust transformation strategy based on scenario analysis and value chain positioning. (2) Tactically, they need to define the participation model and redesign their operating model to ensure effective execution and agility. (3) Operationally, drive targeted performance improvements to stabilize short-term results to fund long-term change.

In an environment shaped by geopolitical uncertainty, shifting demand patterns, and the evolving energy transition, scenario‑based decision‑making becomes critical. Strategic footprint choices must be tested against multiple futures, assessing value‑chain resilience through a combination of feedstock‑forward and market‑back analyses. Feedstock‑forward analysis provides insight into future cost curves, competitiveness, and structural resilience, while market‑back analysis assesses customer demand and the fundamental drivers of growth. Only by stress‑testing strategic choices across scenarios can companies ensure robustness in an increasingly volatile landscape.

Incremental optimization is no longer sufficient; only those who act decisively and adapt rapidly will be positioned to succeed in the new reality.

The structural reset of the European chemical industry

As detailed in our recent study commissioned for Cefic, between 2022 and 2025, the European chemical industry experienced an unprecedented wave of announced capacity closures, increasing sixfold over the period and reaching roughly 37 million tons, close to 9% of total production capacity. In 2025 the announced closured even doubled compared with the previous year.

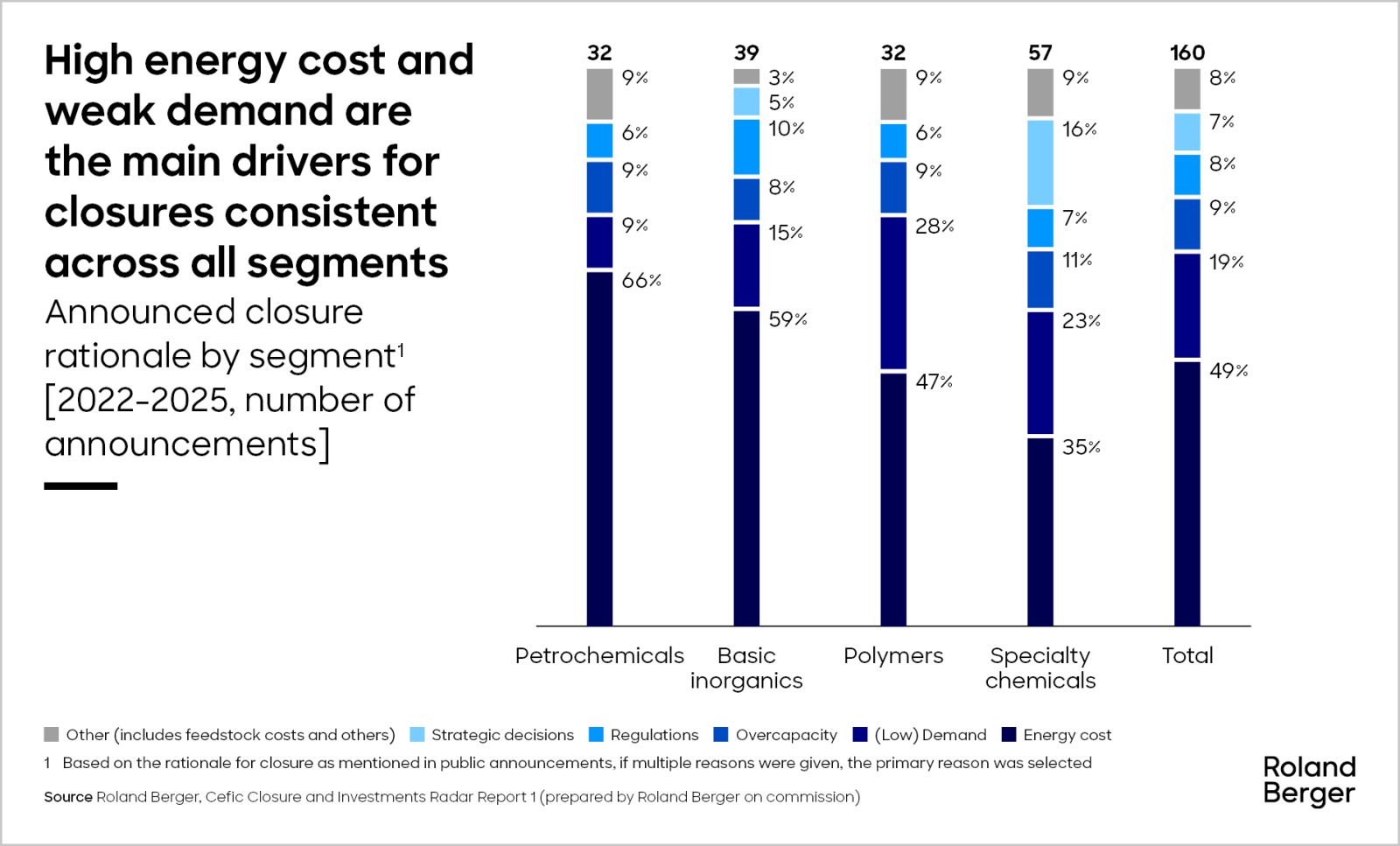

Upstream petrochemicals accounts for nearly 50% of the announced closures in capacity followed by basic inorganics and polymers. The closures are geographically widespread but most acute in Germany and the Netherlands, which together account for nearly half of the total.

Closures are increasingly framed as irreversible, driven by lack of energy cost competitiveness, weak demand, and overcapacity. These closures put approximately 20,000 direct and 89,000 indirect jobs at risk, threatening the stability of integrated chemical clusters across Europe, which might be leading to a cascading and accelerating effect.

"We're witnessing an acceleration in both the number and capacity of closures with companies citing uncompetitive energy costs and weak demand as the main reasons. Chemical players have little choice but to transform their business in Europe."

Investment imbalance: A shrinking footprint

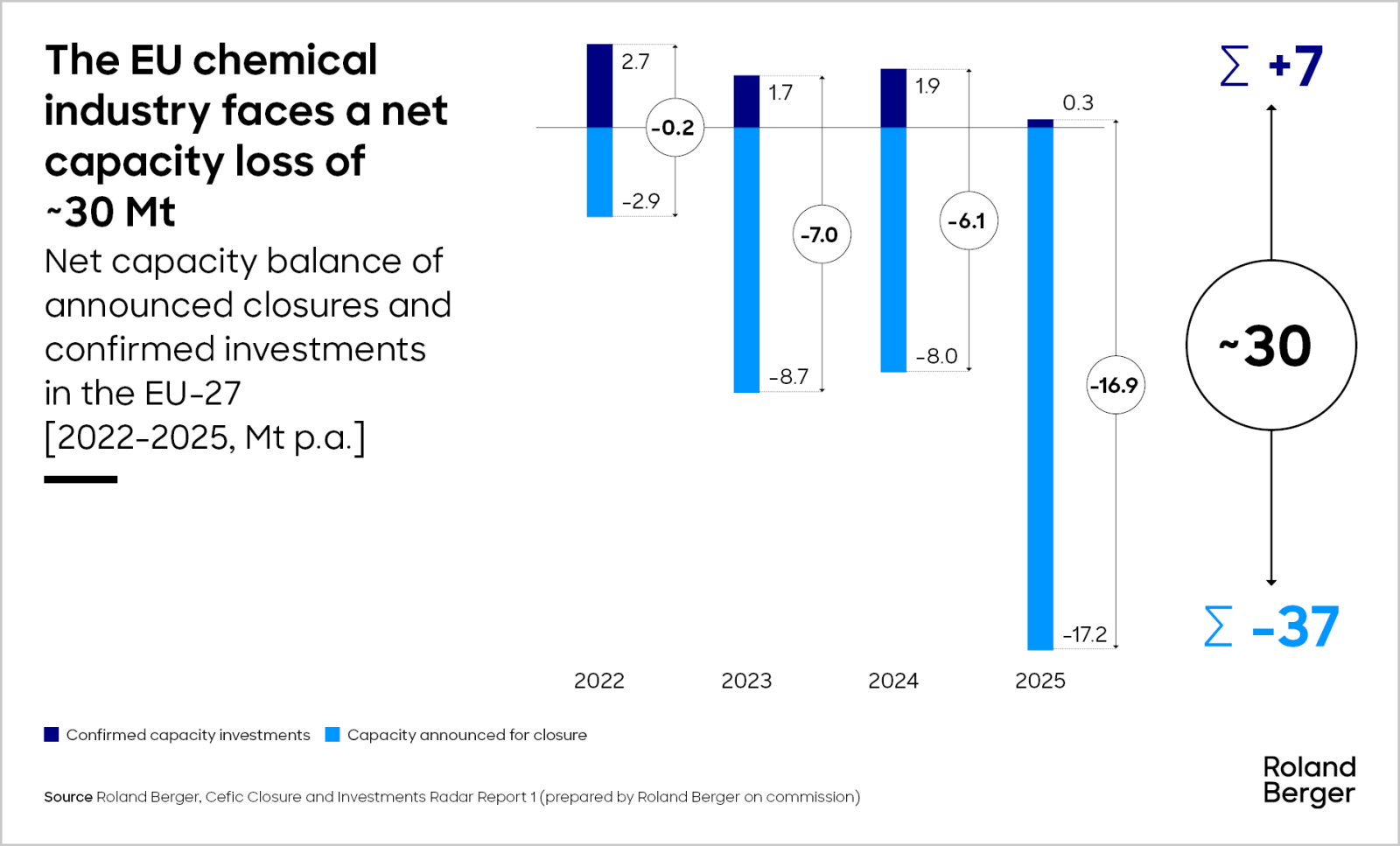

In stark contrast, confirmed investments in new chemical capacity have dramatically dropped by 90% from 2022 to 2025 totalling just 7 million tons over the period, i.e. only 2% of total production capacity.

New investments are by far insufficient to offset the scale of closures, especially in petrochemicals, where new capacity additions are dwarfed by shutdowns. Remaining capital deployment is increasingly concentrated around a limited number of themes including circularity, emissions reduction, and battery materials, which emerges as a silver lining for specialty chemicals.

A decisive moment: Strategic choices ahead

This creates a decisive moment for chemical companies, clusters, and policymakers alike. The industry now faces a structural and potentially irreversible contraction, with a net capacity loss of over 30 million tons.

This raises hard questions about which assets to defend, which to transform, and which to exit, and how to do so while preserving strategic capabilities, employment, and long-term resilience. This is where targeted transformation and performance improvement become critical.

Required actions: From strategy to execution

In an environment of shrinking capacity and constrained capital, chemical companies must make deliberate choices about where to act, by reinventing their strategic positioning, refocusing their operating model and by strengthening near-term economics through performance improvement. Depending on starting point and ambition, this can entail different actions. It may involve value chain repositioning and portfolio and asset optimization, selecting the best participation model defining the radical business rules, and improving performance by defining a new target operating model or by supply chain optimalization, implementing procurement excellence, fixed-cost reduction and plant performance uplift.

Companies that focus on the right levers for their situation can stabilize performance in the short term while building a more resilient and competitive footprint over time. The window for incremental optimization is closing; what lies ahead is a period of active, strategic reconfiguration that demands disciplined choices and execution at speed.

At the same time, strategic decision‑making must explicitly account for the high degree of uncertainty shaping the industry’s outlook. Geopolitics, trade policy, energy markets, regulation, demand recovery, and the pace of the green transition all remain uncertain requiring a scenario‑based approach to assess the robustness of the strategic and footprint choices.

Within these scenarios, value‑chain resilience must be evaluated from two complementary perspectives. A feedstock‑forward analysis provides transparency on future cost curves, regional competitiveness, and structural resilience. In addition, a market‑back analysis starts from customer demand, identifying underlying growth drivers, shifts in end‑markets, and changing customer requirements across regions and applications.

By combining feedstock‑forward and market‑back perspectives, companies can test strategic options against both supply‑side and demand‑side realities, derive clear implications for their portfolio and footprint, and assess how resilient these choices remain under different scenarios. This integrated approach enables more confident decisions on where to invest, where to transform, and where to exit, turning uncertainty from a constraint into a structured input for strategic reconfiguration.

Request the full PDF here

Register now to access the full study. Furthermore, you get regular news and updates directly in your inbox.

Further readings