Define the approach to succeed in the Spanish foodservice market

How players in the foodservice segment are tailoring their strategies for success?

The foodservice market has long been a strategic arena for FMCG manufacturers. This strategic importance has intensified over the past two years, particularly for manufacturers primarily focused on the retail sector. Nonetheless, establishing significance in this market is no simple task, demanding a tailored strategy to emerge victorious.

The foodservice market comprises a diverse array of clients and necessitates various go-to-market strategies. Employing all available tactics isn't the sole path to leadership. Given the market's complexity, success demands defining a tailored business model for each client profile and adapting to collaborate with various intermediaries (distributors, generalists, specialists, C&C, etc.). A fresh, specific approach is imperative; merely tweaking existing retail strategies won't suffice for success in the foodservice market.

The Spanish foodservice market is highly relevant, representing c. 9% over total household expenditure per year

End-consumers allocate a portion of their disposable income to satisfy various needs, both basic and non-basic. A portion of their expenditure is specifically earmarked for leisure and out-of-household activities, with foodservice being a primary choice. Despite the impact of COVID-19, the industry's significance has remained relatively stable at around 10% of total expenditure, and it recovered to pre-COVID levels by 2022.

In comparison to other European countries, Spain demonstrates a notably high dedication to foodservice. For instance, the foodservice segments in Italy and the UK represent approximately 8% of total expenditure, while in Belgium and Germany, they amount to around 4%. Moreover, the Spanish foodservice sector has shown resilience during recession periods. Spanish consumers may defer purchases of furniture or bedding, but they prioritize maintaining their indulgences in foodservice for pleasure.

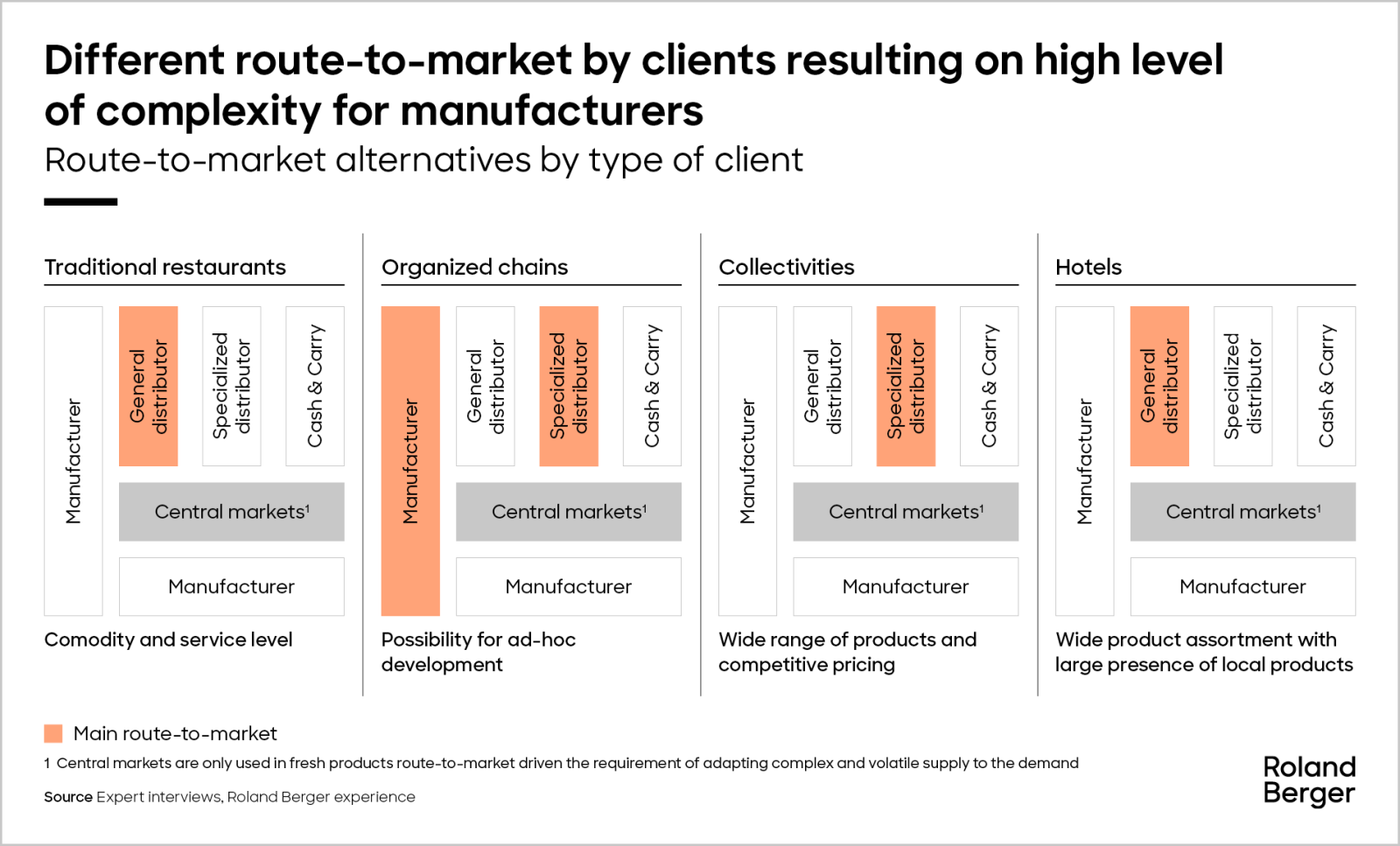

Spanish foodservice market is very complex driven by the wide variety of actors among the value chain.

The foodservice market encompasses a broad spectrum of clients, ranging from traditional restaurants (typically representing around 60-70% of the Spanish market) to hotels and collectivities, including organized chains (the fastest-growing segment in the industry).

These diverse segments differ in their offerings and value propositions to clients; referred supply models and purchasing criteria.

This variety of clients has led to a diverse range of FMCG business models. Becoming the exclusive provider for the entire segment is challenging. However, there are companies that have successfully implemented strategies to cater to the different segments.

"Diversify to Horeca is key to continue growing in the CG&R industry. Copying the retail strategy is not enough, foodservice demands a tailored approach."

But… what are the common characteristics of these players that have succeed in the market?

Successful players typically integrate a wide array of elements, with success often contingent on the specific subindustry. For example, providing fresh meat or fish differs significantly from offering a range of packaged products. There is no single formula for success in the market.

A good starting point is to focus on understanding where manufacturers intend to compete. It's crucial to gain a comprehensive understanding of the market opportunity, encompassing not only market size and prospects but also competitor analysis and the feasibility of entering the segment.

Once the opportunity has been assessed, defining a specific target picture becomes essential. This involves determining the precise role these companies need to fulfill, including which products they will manufacture, their pricing strategies, and their corporate image and branding. This target picture may vary significantly from that of modern distribution targets.

And when the market and target picture is defined, it is the time to prepare the company to provide the service level

Service level is essential, yet it is very challenging for companies to ensure its provision. Many companies falter in this area because the specific requirements often diverge significantly from what they are accustomed to in the modern distribution landscape.

Successful companies typically undertake thorough preparations before entering a market, considering a comprehensive list of requirements necessary to meet market demands. This process involves:

- Determining optimal locations for distribution centers.

- Identifying flexibility requirements within the production process and incorporating them into business case development.

- Mapping sustainable transport alternatives to ensure future sustainability.

- Accounting for all variable costs.

- Establishing a tailored incentive system to foster the professional development of the sales force.

- Defining specific requirements for the sales force, including specialized personnel for each segment.