To cope with today's challenges, retailers must change eight paradigms in their supply chain strategy and apply the right digital technologies to each of them.

Massive potential for industry: Blockchain beyond the cryptocurrencies

By Jochen Ditsche and Martin Streichfuss

More than just hype: Blockchain technologies can bring greater efficiency in supply chain management

Co-authors

Prof. Dr.-Ing. Volker Stich

Managing Director, FIR

Themo Voswinckel

Project Manager, FIR

Jessica Rahn

Project Manager, FIR

Blockchain solutions are mostly known and successfully applied in the financial sector to date. But the undeniable benefits they bring hold potential far beyond finance, making them of interest for industrial applications as well. Supply chains in particular, with their complex structures, multiple participants, and wide variety of material, information and financial flows, can be made considerably more efficient with the use of blockchain technology.

The first thing most people think of in connection with blockchain is probably Bitcoin. The success of the cryptocurrency as a speculative object has made the technology and its advantages well known: With its decentralized and tamper-proof storage of data and documents, blockchain gives players the confidence to engage in business transactions and collaboration without having to know and trust each other. That's because the data is stored not centrally in a database but redundantly across a large number of the participants' servers and is immutable – it cannot be changed without others knowing about it.

The potential of blockchain was really hyped up from 2015 onwards, especially in the financial sector, where apps were developed, Bitcoin and other cryptocurrencies were touted as a way to break the stranglehold of the banks, and virtual IPOs were going to provide capital for startups. But promising projects were underway in other industries, too: IBM and Thyssen-Krupp developed an open platform for industrial 3D printing where companies can share blueprints – which are both copyrighted and protected from modification – with customers or service providers as a way of shifting production from the factory to the end user's premises. In another example, a solution was developed that allows seamless and tamper-proof documentation of the origin of foodstuffs.

However, as with most hype, after the initial highs blockchain plunged to a low for a time: The Bitcoin price, as a gauge of the hype, crashed in late 2017/early 2018 and the market for cryptocurrencies collapsed. Many of the financial apps that had so enthusiastically been developed turned out to be useless or failed to take off due to false expectations. Similarly, the industrial applications proved too expensive, too slow, too inflexible, offered too little apparent benefit and were consequently of too little interest to users. And that was despite the fact that investment in the technology had been enormous to start with, nearly USD 7 billion in 2018. But in the years that followed, spending on developing the technology for industrial applications declined sharply.

"Blockchain technologies are not just interesting for the financial sector. They also hold a great deal of potential for industry."

More realism this time: Making a new go of it after the lows

Nevertheless, the financial sector has already gotten over the disillusionment, and applications for blockchain technology have been experiencing a renewed and sustained boom for some time now. The price of Bitcoin can again be used to gauge the excitement level: Since hitting a low of around USD 3,000 at the end of 2018, Bitcoin's value has risen – first slowly and then more rapidly since the end of 2019 – to around USD 60,000 today. Of course, there's a lot of speculation in this, but there has also been a massive increase in the number and variety of applications developed for financial transactions. These include what's known as DeFi apps (DeFi=Decentralized Finance), mostly based on Ethereum, one of them being Compound, a protocol that handles credit transactions through smart contracts and a central platform; it basically involves cryptocurrencies being converted into Compound's own currency (the cToken) and traded.

By now undeniable, the success of these and other blockchain applications is based on the fact that they create a financial benefit, be it in the form of interest or windfall profits. Outside the financial sector, the focus is on a different benefit of the technology: the efficiency gain. This may be in public administration, for instance, where the digital coronavirus vaccine certificate is based on the IBM and Ubirch blockchain. But in industry there's also a renewed sense of optimism, which can be seen as a sign that here, too, the low of the disillusionment phase has passed and new, more realistic growth is on the horizon.

Supply chain management is an ideal use case

A particularly promising industrial use case for blockchain lies in supply chain management, an area with a background and a set of challenges eminently suited to the capabilities of the technology: Today's supply chains are often highly complex and involve a large number of players. Various production steps are outsourced to suppliers, who in turn use sub-suppliers; as a result, the involved parties sometimes do not know each other and mutual trust is no longer a given. In addition, there are data silos, problems with interfaces, and issues of data security and data sovereignty, which make it difficult to maintain an overview over the entire supply chain and all its players.

This is precisely where blockchain comes in. With its high data security standards and its reliability alongside real-time data availability, the technology provides the basis for single line of sight across all supply chain activities. The tracking and tracing it enables allows players along the entire supply chain to share the necessary information in a way that's tamper-proof, including evidence and certificates to prove, say, cultivation methods, compliance with health and safety and environmental regulations, or the origin of raw materials. These data and documents cannot be added in subsequently, nor can they be falsified or replicated, because every action taken is seamlessly and traceably documented and stored in the blockchain.

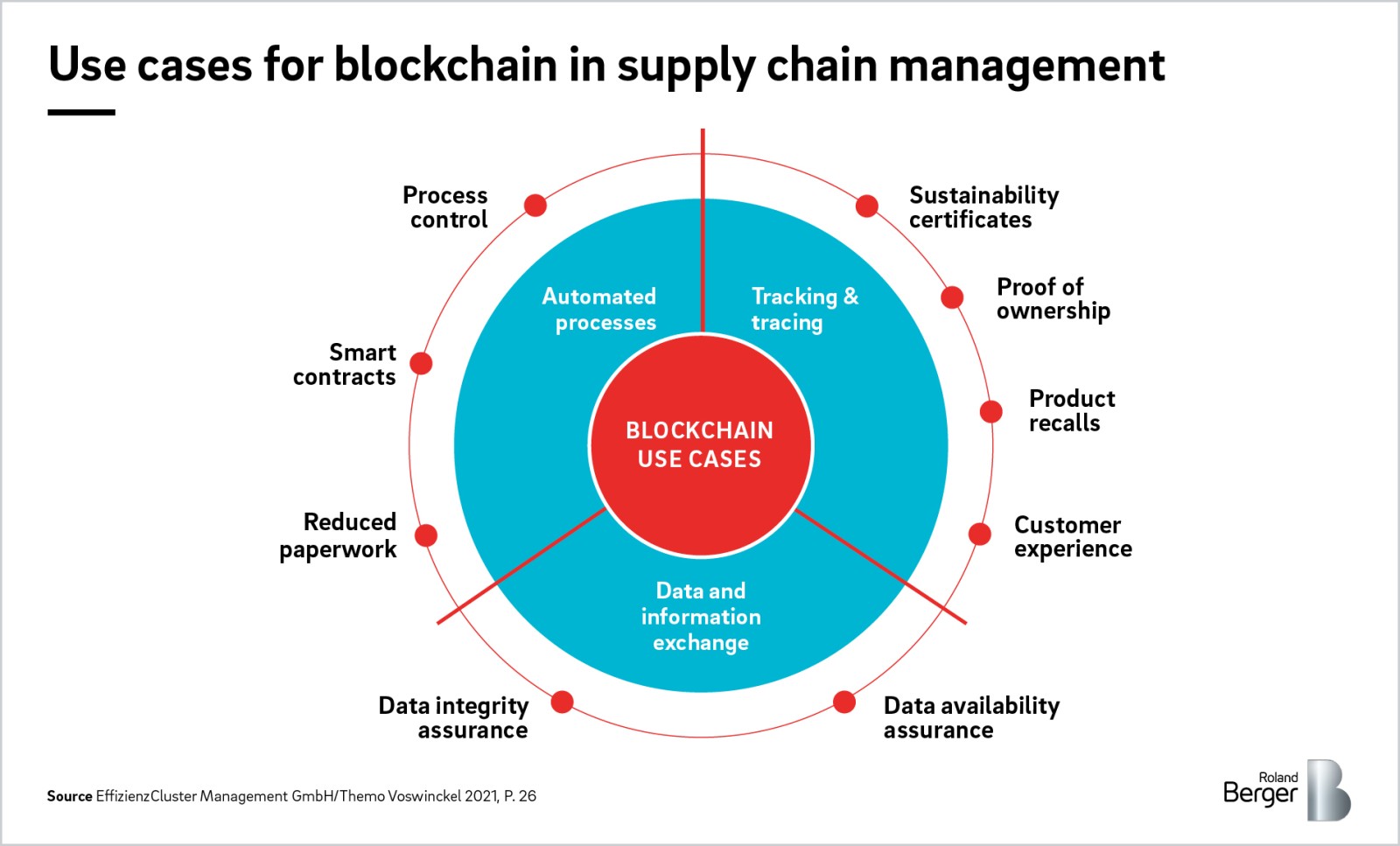

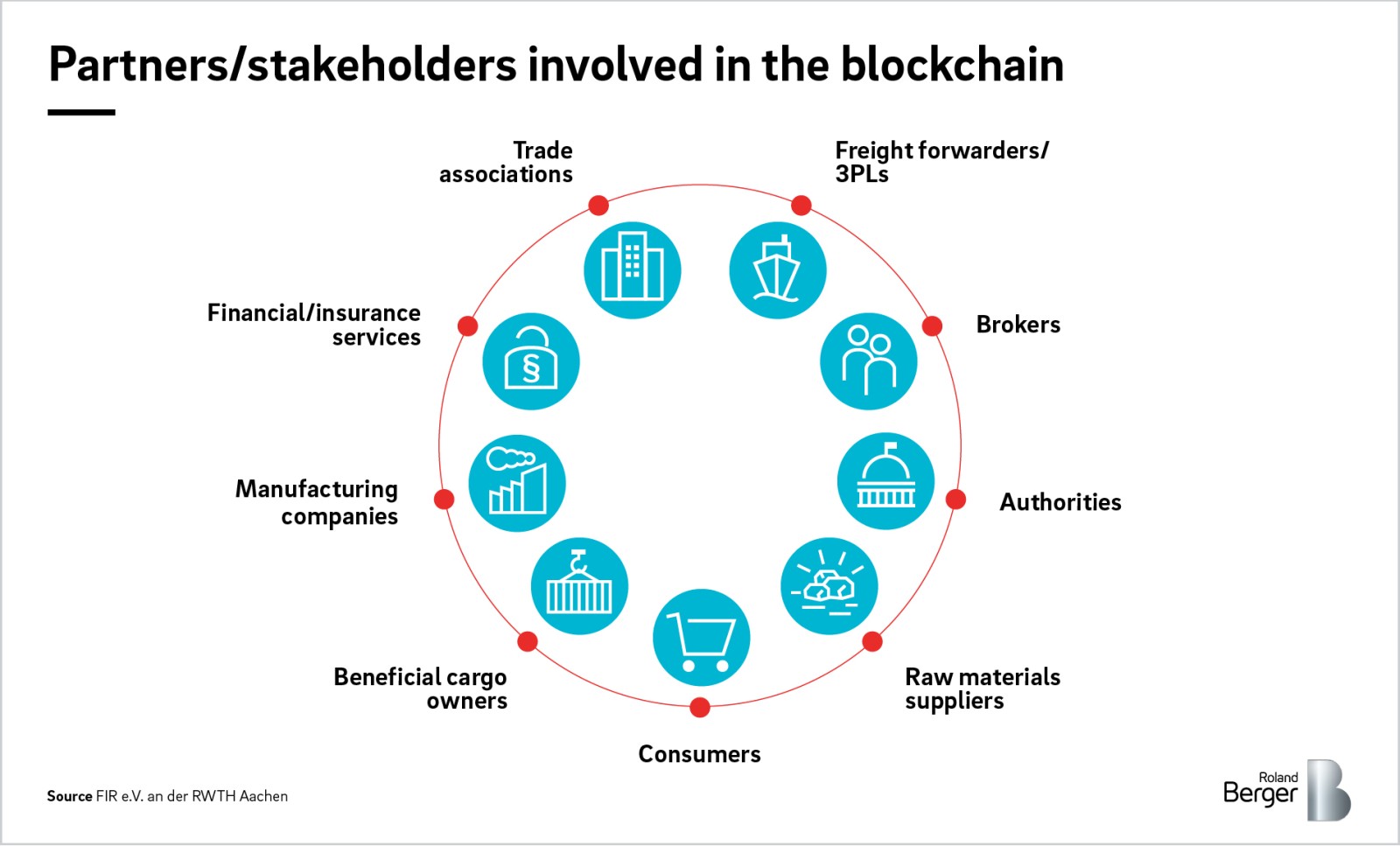

Besides tracking & tracing, there are two other major use cases for blockchain in supply chain management (see Fig. 1): The first of these would be to automate processes, such as electronic invoicing between participants based on an e-invoice. The second would be to exchange data between participants. Here, blockchain serves as a shared database whose content represents the Single Source of Truth. Participants are granted individual access permissions depending on their role in the supply chain, and alerting and information release mechanisms are in place, with the result that all permissioned parties, all the way up to the authorities or consumers themselves, are able to access the information that's relevant to them. A case in point is Tradelens, a cooperative project between Maersk and IBM, which makes the movement of freight containers within global trade transparent and traceable in real time. On the Tradelens platform, port and terminal operators, shipping companies, customs authorities, freight forwarders, logistics companies and other players can exchange data securely and thus make their collaboration more efficient (see Fig. 2).

New potential for businesses

Blockchain's potential is therefore considerable even outside the financial sector, and it is only a matter of time before a new push to use it arrives in industry, too. Companies would be well advised to start thinking about whether they have the structures and processes in place to enable them to use blockchain technology, and indeed how they can best prepare for it. Two issues are key: first, determining the right governance and second, clarifying the technology-related challenges .

Governance

The basic idea behind blockchain is to create a fully democratized infrastructure in which all stakeholders share the decisions on what it should contain and how it should evolve. Turning this into a reality is challenging and it only makes sense to do it when certain preconditions are in place. The ideal use case is a structure with multiple stakeholders who do not trust each other but who share a wish to have an impartial entity that can ensure the fair and cost-effective processing of otherwise costly transactions. This is the case with supply chains. Blockchain solutions therefore lend themselves to supply chain management, including issues of certification and payment. Other solutions are better used for structures where there is a high degree of mutual trust, for example within companies or when just a few companies are involved.

In terms of governance, a number of fundamental questions need to be addressed first and foremost: Which of the involved parties should implement the blockchain solution? Who will ensure the impartiality of the technology? Should there be designated parties who have more power and rights than the others? Or should majority structures decide, with all the extra effort that this entails?

Given that the parties involved from the beginning to the end of a supply chain do not have trust in each other – which is, of course, a prerequisite for the meaningful application of blockchain solutions – these and similar issues can be challenging. One solution would be to set up a consortium that makes its decisions democratically.

Technological challenges

As a collective term, a blockchain can take many different forms. There may be differences in the degree of data distribution, the consensus mechanism or the scope of data storage. Depending on how these and other criteria are defined, they can have far-reaching consequences on things like the practicality of the solution or the associated costs. It's vital to think through and clarify the following issues:

- Scalability: The number of nodes determines the efficiency of the blockchain. The more nodes, the greater the computing effort.

Depending on the consensus method that's been chosen, considerable time delays and costs can arise under certain circumstances before a transaction is eventually recorded. The decision to opt for a private or a public blockchain is also a significant one. Both have their limitations, which need to be weighed up in the context of the intended use case. - Volume of data: The amount of data that can be stored in a blockchain itself is limited. If it were not, the blockchain's resource consumption would go through the roof due to the same data being stored in different places. One solution here is to store only document signatures on the blockchain, including access permissions and the actual storage location. This provides a secure reference to each document, but the document itself is stored separately, either centrally in the cloud or decentrally at the company concerned.

- GDPR compliance: Data privacy is indispensable for the success of blockchain solutions and must therefore be incorporated from the very start. The key question is whether it's possible to trace information back to individual users and their identities. From the very moment the structure is set up, it's essential to ensure that personal data is not stored in the blockchain, because the immutability of data means it will not be possible to delete it later.

Bottom line

There's life in the old dog yet: In the financial sector, blockchain is already experiencing a new and sustained boom. But the technology also holds a great deal of potential for industry. Blockchains can connect material, information and financial flows as well as numerous different players, which means that they can map, automatically monitor and control complex chains and networks in a transparent manner. Supply chain management is one area in which that equates to considerable potential for efficiency gains.

Further readings