How banks can master the new competitive situation in the SME lending market and successfully adapt their business model

In the lending market, small and medium-sized enterprises (SMEs) represent a very attractive segment for banks and other lenders. But the business environment is changing dramatically: more and more SME customers are turning to alternative financing providers such as manufacturers, digital banking platforms or alternative (direct) lenders. They offer them better conditions, less complicated processes and more customized solutions. Traditional bank loans are becoming much less relevant. Banks and other incumbent lenders must act now to adapt their business model to the changed needs of SMEs, otherwise they're at risk of irretrievably losing an entire business segment.

More than 99 percent of companies in Germany count as small and medium-sized enterprises (SMEs). They generate 60 percent of all corporate revenues, making them the mainstay of the German economy. And they need access to lending. Accounting for a volume of EUR 279 billion, some 36 percent of all unsecured corporate loans in Germany go to SMEs – so they are undeniably a key customer group for banks and

financial service

providers.

But the classic bank loan is becoming less and less relevant for these companies: some are now actively avoiding banks' often slow, opaque and overly bureaucratic processes. Too many SMEs do not get individual offers that are tailored to their actual needs, and they also note a lack of understanding of new, digital business models among some banks. Over recent years, growing numbers of firms have already begun seeking alternative forms of financing, a trend that has accelerated significantly in the wake of the COVID-19 crisis and the massive influx of time-critical applications for loans and support that it triggered. As a consequence, 86% of SMEs are happy to consider alternatives to traditional bank loans, while 11% have already made use of this option – and the tendency is rising (see Fig. 1).

"The future of loan processing is live, seamless and transparent. Banks need to live this reality."

Keeping step with this trend, the range and number of new players in the market for lending is growing steadily. Today, companies can choose between loan offers from banks as well as manufacturers, digital banking platforms, alternative (direct) lenders and other players. Business models that are closely aligned with customer needs have the best chances of success. Providers with the ability to use the latest digital technology to perform smart data analytics to compute accurate credit scores and quickly make customers bespoke offers via digital platforms have an edge here.

Rising competition in the SME lending market weighs on margins

Our analysis indicates that the volume of SME loans transacted via platforms will have reached as much as EUR 250 billion by 2025. Competition is already ramping up massively, as can be seen from the declining margins on SME lending, which recently sank to just over 2 percent. For incumbent lenders, and the banks in particular, this means that their traditional business is in jeopardy unless they act now and adapt to the needs of SMEs. They must not miss the opportunity to support small companies as they grow over the longer term, which would allow them to increase their lending exposure over time. Clearly, the SME segment is far too important to give it up to new players without a fight.

"Banks have to adapt their business model to the changed needs of SMEs if they don't want to fall behind in this segment."

For many banks, the requirements of the future SME lending process will necessitate the wide-ranging digital transformation of their business model. In order to initiate this transformation, reposition themselves in the SME lending segment and align their business for the future, banks first need to put all of their processes under the microscope. Then they will be able to identify gaps in their current set-up compared to the competition and take steps to close them, for example by improving individual processes or bringing in proven external solutions.

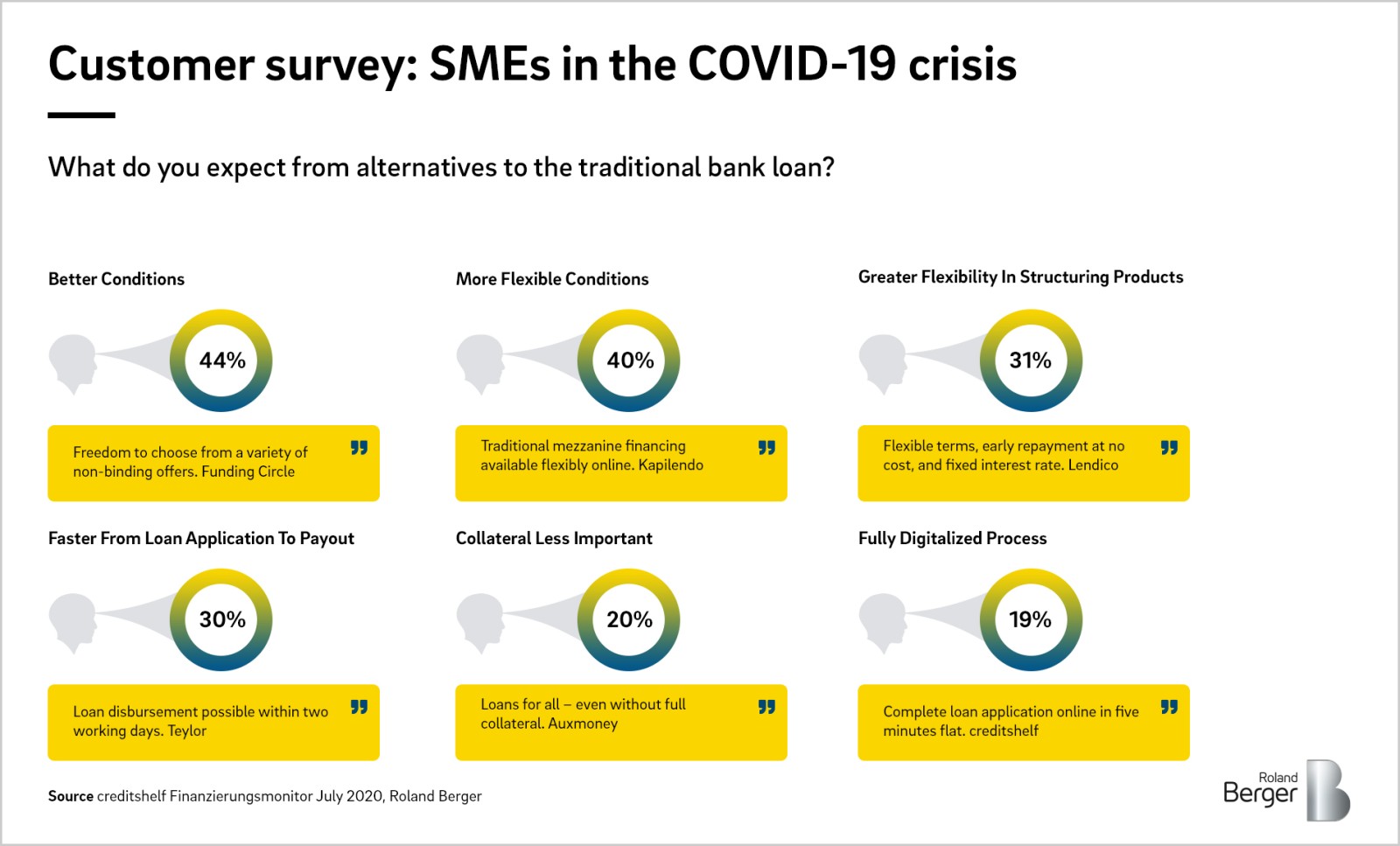

The key to success in the SME lending market is to focus stringently on customer needs. This means, above all, offering flexible terms and conditions as well as product features, having fast processes and ensuring transparency over the requirements for being offered a loan. All of this should be combined with high levels of service, striving to offer customers added value (see Fig. 2).

How to develop a future-proof business model

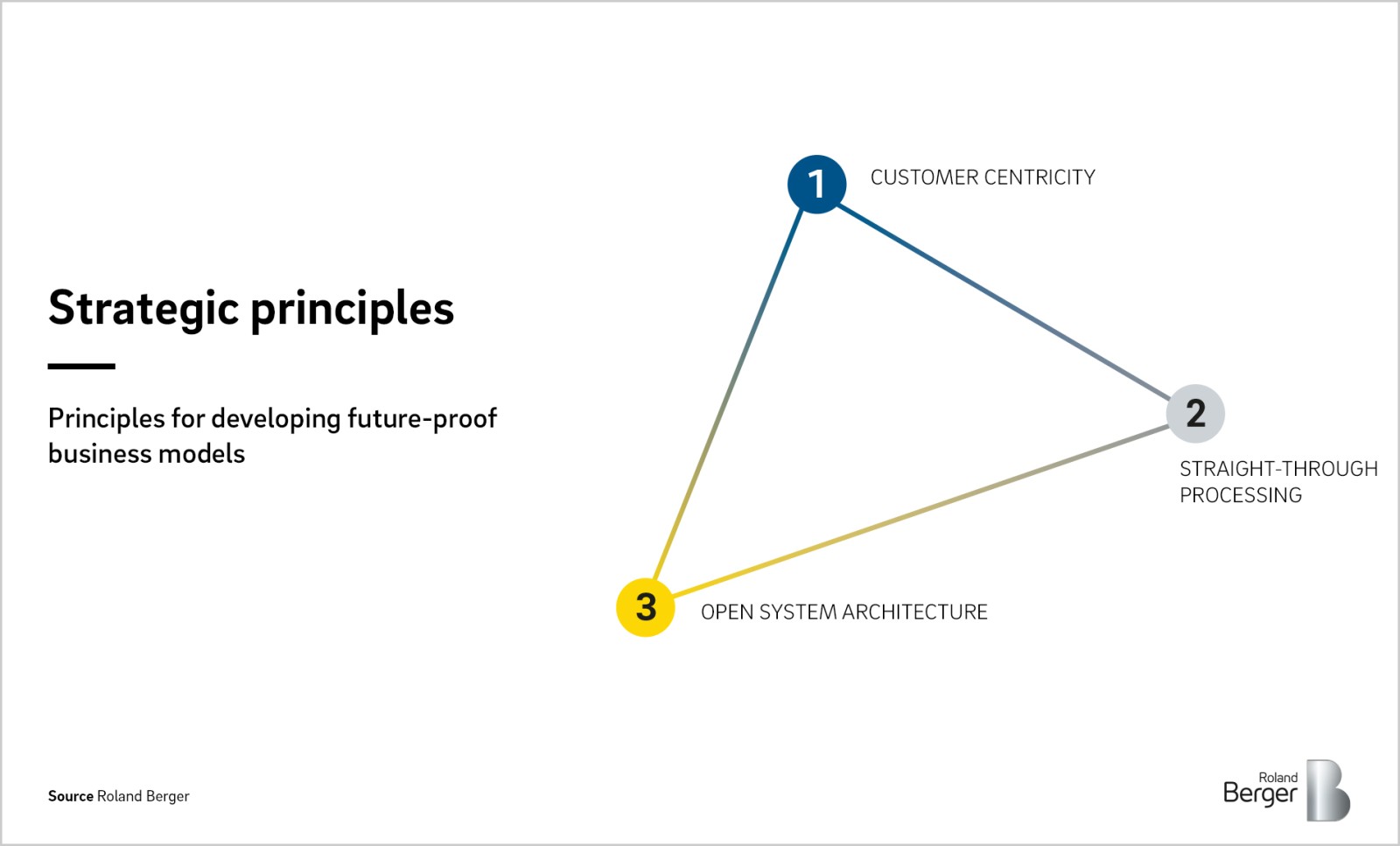

The SME lending process is in need of radical digitalization and simplification. The key levers that can be applied here are automation of workflows and data processing, standardization of modular products, clear specialization with roles created specifically to support SMEs, and steering and controlling geared to the new challenges. Banks should follow three strategic principles (see Fig. 3):

Customer centricity: Customers need to know that their individual requirements are understood from the moment they first make contact. This requires a standardized data repository and an optimized customer front end.

Straight-through processing: Efficient and transparent processes are fundamental to being able to process applications quickly – systems need to be harmonized, technologies standardized across the board and manual activity reduced.

Open system architecture: The required product range or the necessary process quality is often impossible to realize efficiently with internal solutions. Banks should therefore say goodbye to monolithic operating models and build an open system architecture.

These strategic principles can be implemented in two stages that lead towards the evolution of the bank business model: first through extensive digitalization and automation of the lending process, and then by building a fully integrated offering that goes beyond traditional banking services. We'll help you put the necessary prerequisites (including Open Banking) in place so that you can offer your SME customers an innovative lending experience.

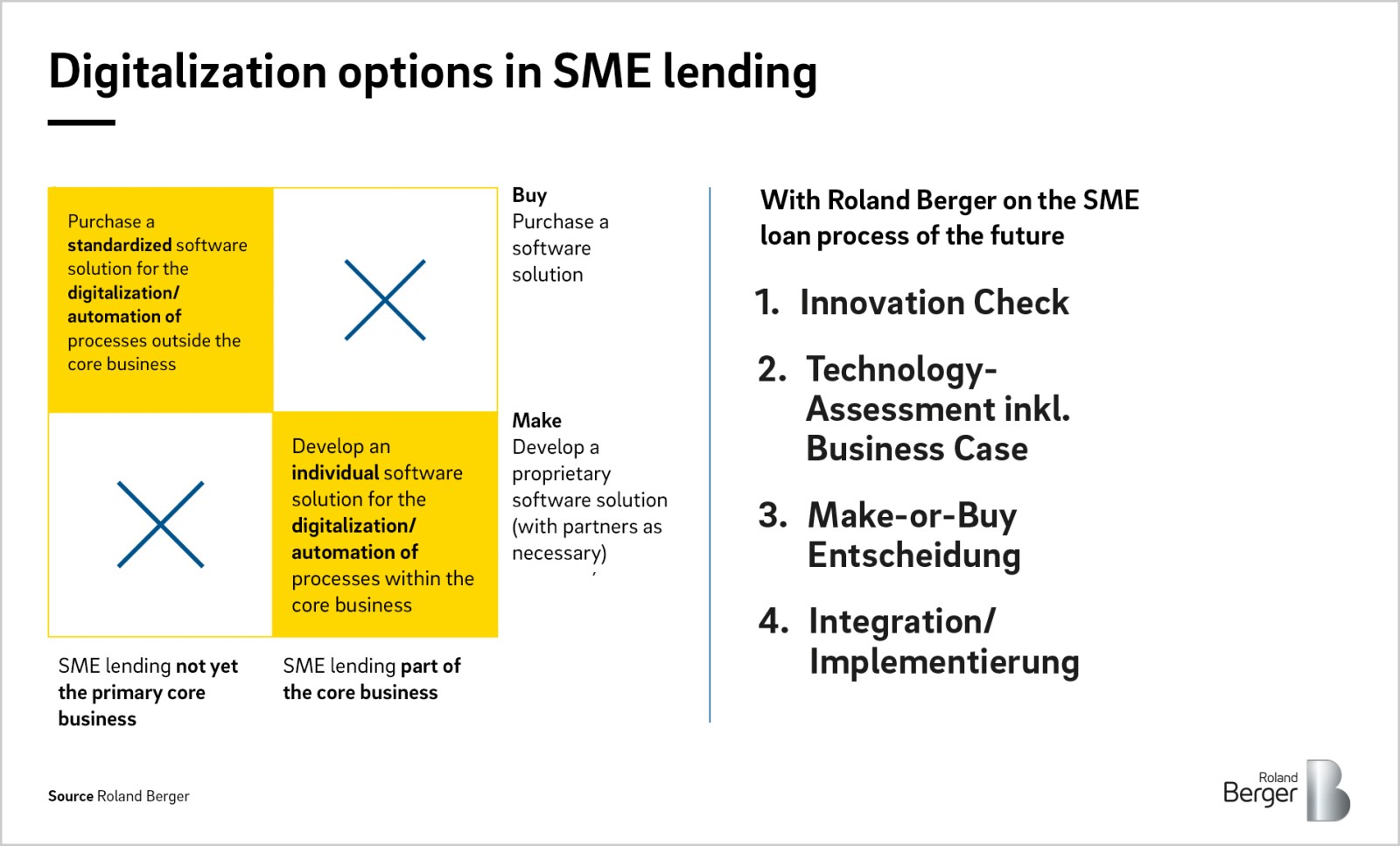

Roland Berger has supported German and international clients in numerous projects as they seek to manage the transformation, to reposition themselves in this segment and to align their business for the future. We will be happy to advise you today on the requirements of tomorrow's SME lending process. After conducting a situation audit, we'll define a holistic business case with a focus on your long-term strategy. From this, we'll derive a customized recommendation for you on whether to develop technical solutions yourself or to bring exclusive partners on board (see Fig. 4). Because one thing is for sure: if you merely implement standard solutions, you will end up irrelevant – what you need is bespoke solutions and an emphasis on your bank's specific USPs. When it comes to developing and implementing these solutions, we'll be by your side, steering all service providers to ensure turnkey delivery.

For a detailed analysis of the SME lending market and its importance for banks and lenders, as well as recommendations and steps to develop a future-proof business model, please take a look at our study on the future of SME lending.

Study

SME lending in transition: opportunities to develop future-oriented business mod

The market for SME lending is changing rapidly: Alternative financing providers are becoming increasingly attractive to companies, and the traditional bank loan is losing importance. Banks and other traditional lenders must adapt their business model to customer needs and learn from the most successful financing platforms.

![{[downloads[language].preview]}](https://www.rolandberger.com/publications/publication_image/700_roland_berger_the_future_of_sme_lending_cover_en_download_preview.png)