Explore key trends and winning strategies in the global natural gas market. Download our latest study for actionable insights.

Unlocking value potential for renewable energy developers

How project developers under pressure can achieve measurable results

The economics of renewable energy development have changed. Permitted pipelines are growing, auction prices are falling, and investors are expecting higher returns. Developers that want to remain competitive need to adjust across strategy, operations, and finance.

"The fundamentals of the energy transition are intact. But in today's market environment, developers need to clean-up their portfolios and embrace new business models such as multi-technology projects and new offtake structures."

For much of the past decade, the development model was relatively straightforward: secure permits, win tenders, build projects, and repeat. That model worked well in a period of supportive auction prices, low interest rates, and clear policy support for ambitious build-out targets. But the market has moved on.

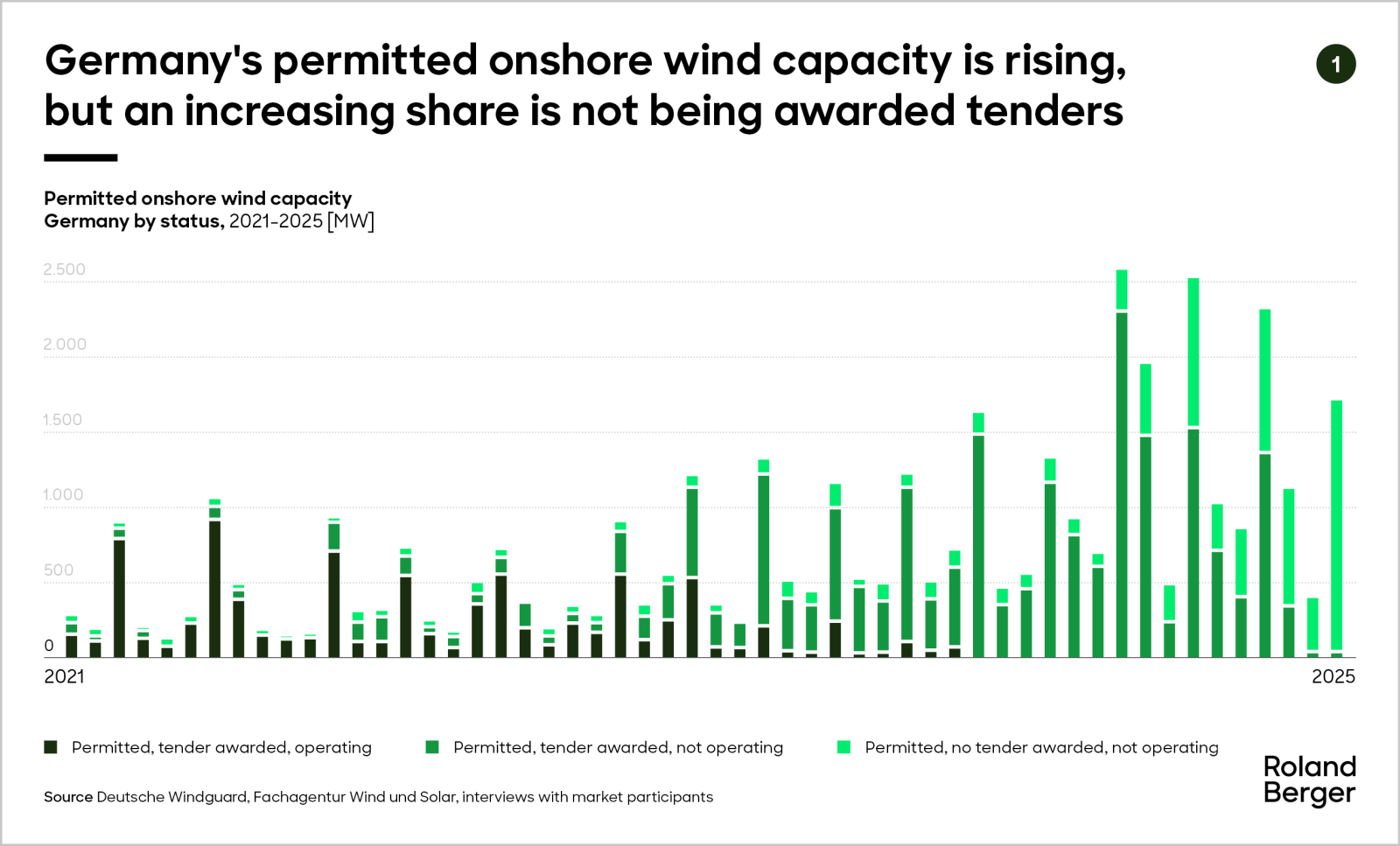

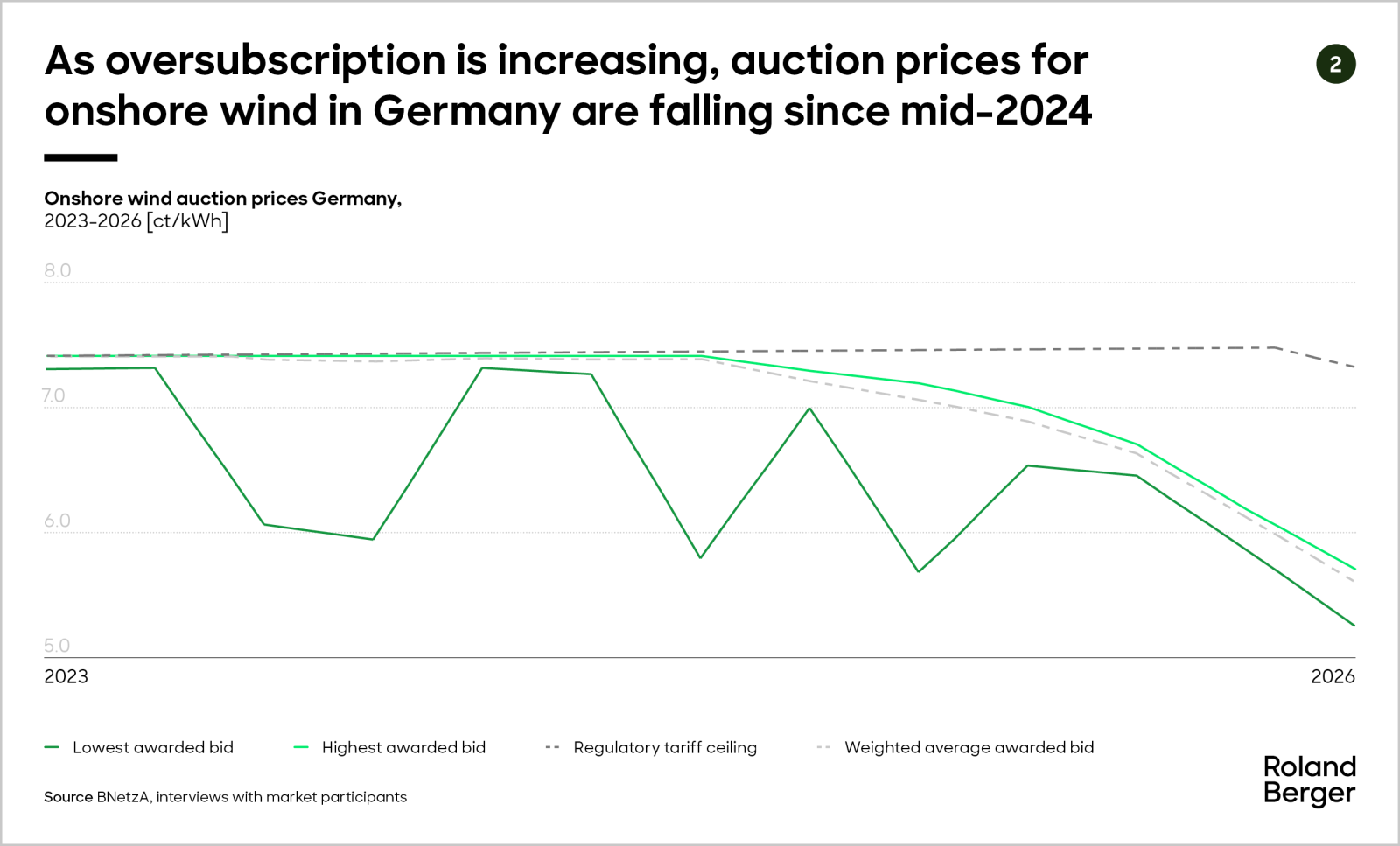

In core European markets like Germany, the volume of permitted onshore wind capacity has been growing steadily, resulting in heavily oversubscribed auctions where a glut of permitted projects competes for the limited capacity that can be awarded. As a result, auction prices have been declining since mid-2024. On the financing side, the reset in risk-free rates has pushed equity return expectations higher, with ten-year government bond yields sitting well above the historic lows seen in the early 2020s.

The result is a much tighter business environment for developers. Players are navigating margin compression on projects, alongside rising return expectations. Market valuations have come down, and the green premium that pure-play renewables once enjoyed has narrowed. None of this signals the end of the energy transition. Installed capacity targets remain ambitious and policy support continues. But the business of developing renewable energy projects requires sharper strategy and more disciplined execution than it did a few years ago.

Six strategic levers to unlock value

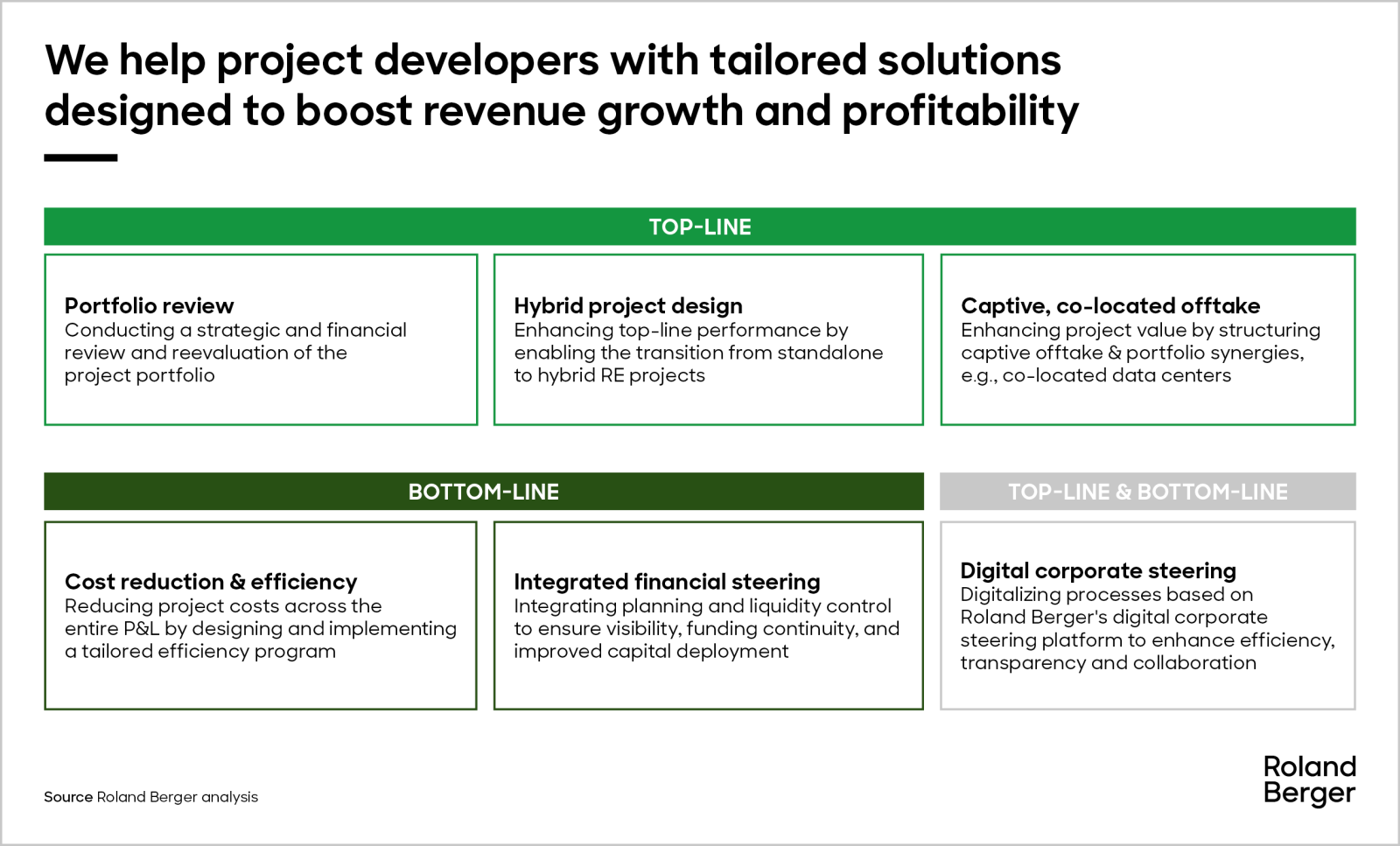

Across our work with renewable energy developers globally, we see six areas where focused action can make a measurable difference. Some are about protecting and growing the top line. Others address the cost base and operating model. Together, they form a coherent response to the new market realities.

1) Portfolio review:

Any strategic response starts with the portfolio itself. A large development pipeline looks impressive on paper, but it's only valuable if the underlying economics hold up under today's conditions. Many pipeline valuations still carry assumptions on margins, capture prices, and realization probabilities that were set in a different environment. Many also carry concentration risk across technology, geography, or development stage.

Developers who are managing this well conduct rigorous, strategy-led re-evaluations of every project's risk-adjusted economics. They set explicit financial guardrails, enforce them through structured stage-gate processes, and stress-test regularly against realistic downside scenarios.

2) Hybrid project design:

With portfolio clarity established, the next question is how individual projects can be structured to perform better commercially. Here, the shift from standalone to hybrid is one of the most significant developments in the sector.

Co-located solar PV and battery storage projects are growing rapidly and are expected to represent the majority of new solar deployments by the end of the decade. Hybrid configurations allow developers to shift energy to higher-price periods, reduce curtailment exposure, and access ancillary service revenues. In a market of declining capture prices, that flexibility meaningfully improves project economics. But it requires updated financial models, revised procurement strategies, and organisational readiness.

3) Captive, co-located offtake:

Beyond project design, developers can further strengthen revenues by rethinking who buys the energy and how it gets there. Captive, co-located offtake is gaining traction as a way to improve both revenue and project bankability.

When a renewable project supplies a co-located consumer directly, the offtaker avoids grid and balancing fees that can represent roughly a third of total electricity cost. That saving allows developers to negotiate PPA pricing above auction price levels. Data centres, with their surging power demand driven by AI and digitalisation, are a natural fit. Structuring these arrangements well requires careful commercial work, but the value potential for both sides is significant.

"The developer industry has entered survival-of-the-fittest mode. In this environment, the winners will be those who combine rigorous cost discipline with operational excellence. Standardized processes, leaner structures, and smarter procurement are no longer nice-to-haves."

4) Cost reduction and efficiency:

While the first three levers focus on the top line, the cost side deserves equal attention. Growth periods tend to mask inefficiencies, and many developers have accumulated overhead, while neglecting PMI in the case of M&A during their expansion years. When it comes to core processes, standardization in project development and optimized procurement for equipment and key services are often lacking.

Given these shortcomings, the improvement potential is often larger than expected. In wind turbine procurement, for instance, optimized project configurations, volume commitments, and longer-term framework agreements with OEMs can yield price reductions of 8–14% of CAPEX. Similar opportunities exist across construction, O&M, and overhead functions. Capturing them requires structured baselining, clear measure ownership, and disciplined tracking.

5) Integrated financial steering:

Operational and commercial improvements only deliver their full impact if the financial steering model can keep up. In many fast-growing RE businesses, that’s not yet the case. Planning is fragmented, liquidity management is reactive, and an EBITDA-centric lens overlooking cash and financial KPIs can mask whether the business is truly positioned to finance its next stage of growth.

An integrated model connecting P&L, balance sheet, and cash flow in a single framework, combined with structured short- and long-term liquidity planning, provides the visibility needed to manage cash proactively, prioritise investment, and engage credibly with capital providers.

6) Digital corporate steering:

Finally, much of what has been described above becomes easier to execute and sustain with the right digital infrastructure. Yet, many developers operate with IT landscapes that have evolved organically, with systems that don't integrate well and project data scattered across spreadsheets.

The most effective approach is pragmatic: pinpoint the most critical process bottlenecks and address them with targeted solutions first, e.g., stage-gated project platforms, automated reporting, AI-assisted permitting, or centralized portfolio dashboards. A "merit order" logic, solving the highest-impact problems first, ensures that digital investment delivers returns quickly rather than becoming an end in itself.

From growth to value creation

The renewable energy sector remains structurally attractive, but the rules of the game have changed. Growth alone is no longer enough. The developers best positioned for the next phase are those making deliberate choices today about portfolio composition, revenue structures, cost discipline, and operational capability.

Those who act decisively will be best positioned to thrive in the next phase of the energy transition.

Want to explore what this could look like for your organization? Get in touch with our energy experts today!

Sign up for our newsletter

Sign up for our newsletter and get regular insights on newest publications related to Energy & Utilities.

Further readings

_person_320.png?v=1687234)