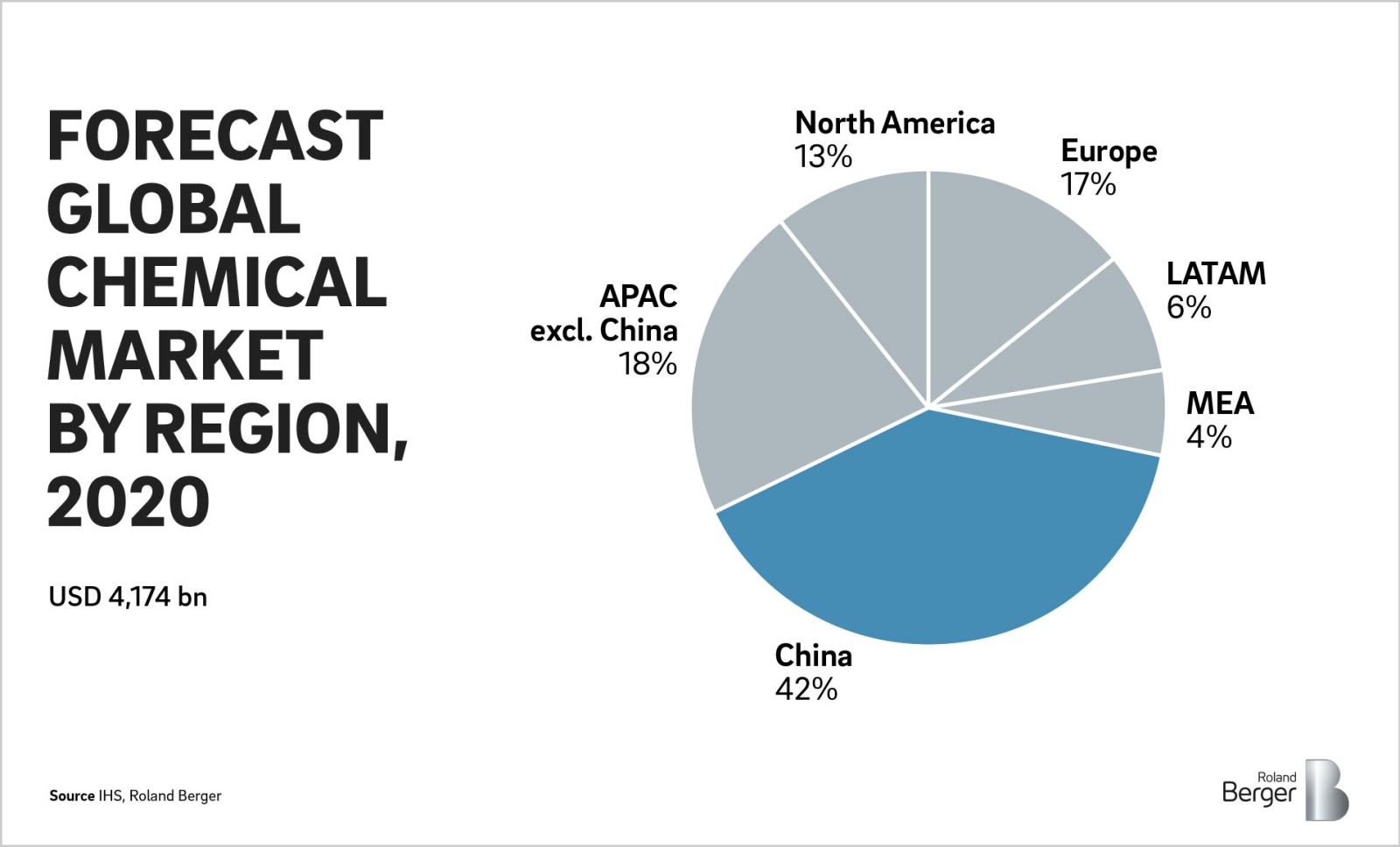

China is in the midst of a great transition. No longer willing to be classed as a major polluter, it is undertaking one of the most comprehensive sustainability action plans in history – and the chemical industry will be fundamental to turning this vision into reality. For its part, the chemical industry in China is entering a period of consolidation and selective growth. In line with the planned environmental upgrade, both domestic and foreign companies will have to meet new environmental standards and deal with higher production costs. As domestic players consolidate, foreign players will face fiercer competition.

But the environmental reform presents opportunities as well as challenges. As environmentally-friendly solutions increasingly become a matter of priority in China, the provision of greener, more

sustainable chemical applications

presents a new window of opportunity for astute Western players to develop and secure their share in the world's largest chemical market by far.

"We need not only economic growth but also a good ecological environment, and we prefer a good ecological environment to economic growth. In fact, a good ecological environment is itself a valuable asset.

"

Xi Jinping

President

People's Republic of China

A new environmental approach in China

China's leaders – headed by President Xi Jinping – consider environmental protection a major driver of economic transformation and sustainable development for the country. The 13th Five-Year Plan, which covers the period 2016-2020, promotes a more sustainable economy, with strong commitments to environmental management and protection, clean energy, emissions control, ecological protection and security. Moreover, with the introduction of the amended Environmental Protection Law on January 1, 2015, China fundamentally restructured its approach to environmental regulatory enforcement.

The regulatory environment in China is complex. Since 2013 the country has enacted numerous environmental regulations, and it continues to draw up new measures and further strengthen enforcement. In 2017 the country consolidated its previous government agencies into three ministries responsible for environmental policy decisions and enforcement: the Ministry of Ecology and Environment, responsible for controlling pollution and mitigating climate change; the Ministry of Natural Resources, in charge of natural resource management, urban planning and rural planning; and the Ministry of Emergency Management, which designs policies and mechanisms for managing emergencies.

Regulations affecting

the chemical industry

cover the entire industry value chain. In the area of energy, for example, China has promised to reduce national consumption by 15 percent by 2020 compared to the 2015 level. To achieve this reduction, it is using market-based mechanisms such as a national carbon trading scheme. China also aims to reduce national coal consumption, including for the production of chemicals. Its goal is to achieve total consumption of 4.1 billion tons of coal by 2020, down from peak consumption of 4.2 billion tons in 2013.

The changes in the regulations also affect production and maintenance, formulated products, warehousing and storage, and transportation. China has increased its scrutiny of chemical companies, upping the number of on-site inspections it carries out. It has also limited the number of approvals for new plants and the number of permits for transporting and storing hazardous materials. The government has made efforts to close down small factories, for example, only allowing same or reduced capacity relocation of caustic soda factories from mid-2016. China intends to relocate chemical plants manufacturing dangerous chemicals out of densely-populated city areas to industrial parks. All chemical manufacturers in Shandong province for example, especially those who produce hazardous chemicals or are newly registered, must be relocated into qualified chemical industry parks by the end of 2018. Furthermore, Beijing has improved its chemicals management system with a revised version of "China REACH" (the New Chemical Substance Notification), affecting all production activities and also the import and export of new chemicals.

In the area of waste and emissions, the Chinese government has introduced new, restrictive standards for carbon emissions, polluting chemical exhaust fumes and industrial waste from the production of chemicals. The aim is to reduce major air emissions by 2020 compared to 2015 levels. China also now requires major emitters to install automated monitoring equipment and publish their emissions figures. In April 2015, the State Council issued its Water Pollution Prevention and Control Action Plan, which sets a series of ambitious targets for 2030. They include achieving excellent water quality in seven major watersheds, eliminating "black and odorous" water, and achieving an overall water quality of Level 3 or better for 95 percent of point sources in urban areas. Key themes of the plan are industrial effluent management, wastewater treatment, water reuse and enhanced monitoring. Finally, an Environmental Protection Tax Law – the first of its kind in China – came into force on January 1, 2018, tightening up the enforcement of environmental regulations.

Trends, impacts and opportunities

What are the key trends in the chemical industry and how can Western companies use them to their own advantage? We examine four key areas below.

China is shifting its focus from commodity chemicals to specialty chemicals.

Impact: China used to be first and foremost an exporter of upstream commodity chemicals. Now, specialty and fine chemicals represent an increasing share of economic growth. Specialty chemicals are forecast to grow at eight to nine percent a year through 2020. These are important ingredients in the country's efforts to upgrade its industrial value chains.

Opportunities: International companies are strongly placed to meet China's growing appetite for specialty chemicals, supplying the chemicals that China lacks. Products poised for rapid growth include electronic materials, fine chemicals, food chemicals, specialty plastics and water-treatment chemicals.

Chinese chemical companies are beginning to lose their cost advantage due to rising wages and higher environmental standards.

Impact: New – or newly enforced – environmental protection measures mean that Chinese chemical enterprises are losing their cost advantage and running at low production rates. Companies that have upgraded their technology stand to benefit here. At the same time, higher safety standards mean larger initial investments and increased operation and maintenance costs.

Opportunities: Western companies that already take environmental protection seriously will enjoy greater cost advantages due to a reduction in their tax burden. Chemical companies doing business in or with China can leverage their knowledge and high standards as enforcement of the legislation becomes stricter.

Chinese chemical plants are closing down, reducing overcapacity.

Impact: Higher energy and freight costs, combined with newly enforced environmental regulations, have resulted in a significant drop in Chinese production and exports. Small factories have been and will continue to be closed down. At the same time, new production capacities with new standards will be built. Overall, regulation has a positive effect, as cost-intensive production is replaced by cost-effective, state-of-the-art processes. As oversupply falls, Chinese producers can also enjoy better pricing.

Opportunities: Western companies can provide knowhow and expertise to Chinese companies as they replace their cost-intensive production with state-of-the-art processes.

Impact: The Chinese chemical industry is currently highly fragmented, particularly in the area of specialty chemicals. Tighter environmental regulation is forcing a reduction in overall capacity and an improvement in the level of technology used. This will result in fewer chemical players in the market, as the weakest and smallest players will not be able to afford the necessary production upgrades. Overall, stronger environmental regulation will benefit bigger, technologically more advanced players.

Opportunities: This is good news for Western players in China: These companies tend to be bigger and have better technology, particularly with regard to emissions control.

Leveraging China's new sustainability agenda

To maximize the opportunities generated by China's new agenda and exploit them as effectively as possible, Western chemical companies need to take action. They must emphasize their own high environmental standards and their knowhow regarding energy efficiency: After all, they are already familiar with what is becoming the "new normal" for China, namely environmentally-aware production, clean technology, higher wages and consolidated markets. By positioning themselves correctly, they stand to benefit substantially from China's new focus.

However, the window of opportunity for action is narrowing. Chinese players are already catching up with Western standards, and unless they take action fast, Western companies will quickly become less attractive for China. We recommend a number of carefully targeted actions.

Align yourself with China's needs Western companies can provide access to the chemicals or technology that China lacks, especially in the area of more advanced chemicals. The Chinese government is actively backing sectors such as electric vehicles, new energy technologies, transportation-related industries, agriculture and industry standards. Western players should offer quality processes here that are not easily replicable by Chinese companies. In many of these areas, Western players are superior in terms of product quality, performance and customer service. Furthermore, local manufacturing enables Western companies to tap into China's resources of raw materials such as phosphate rock, fluorspar and rare earths.

Manage stakeholders proactively It is vital for companies from the West to work with all the relevant stakeholders in China, from the government to suppliers, vendors and local communities. This is particularly important for securing new plant projects. Indeed, many multinationals have a dedicated, corporate-level government affairs team based in a single location in China that works on understanding stakeholders' concerns and addressing them ahead of time.

Manage your reputation Western companies should try to minimize the popular perception of them as contributors to environmental degradation, positioning themselves instead as promoters of the sustainability agenda. They will need to actively communicate the benefits created by their activities within China and their exports from China – for example, they can consider issuing a report on their economic, environmental and social performance. They can also create value propositions for university graduates and industry experts, tailored to the demands of an ambitious workforce.

Develop a local channel and go-to-market strategy Companies should tailor their distribution approach to the region in question. This will partly involve developing a suitable network of distribution partners in order to get closer to customers.

Pursue M&A and partnerships Finally, mergers and acquisitions (M&A) and joint ventures are effective ways for Western players to increase their market access in China. Players should set up a dedicated business development team in China. Now is an opportune moment for M&A, as traditionally high market valuations have fallen to more moderate levels. Over the last decade, a group of dynamic midsized Chinese specialty-chemical players has emerged that are attractive acquisition targets.

_person_144.png?v=1687234)