A challenging outlook for industrial automation in 2025, but after a short breather, we believe robust growth will be back in the pipeline and expect improvement through 2030.

Industrial automation update 2026

By Alex Xu, Ralph Mair, Eymeric Boyer and Sebastian Koper

The year of the upswing? Or another one with muted development?

Previous report

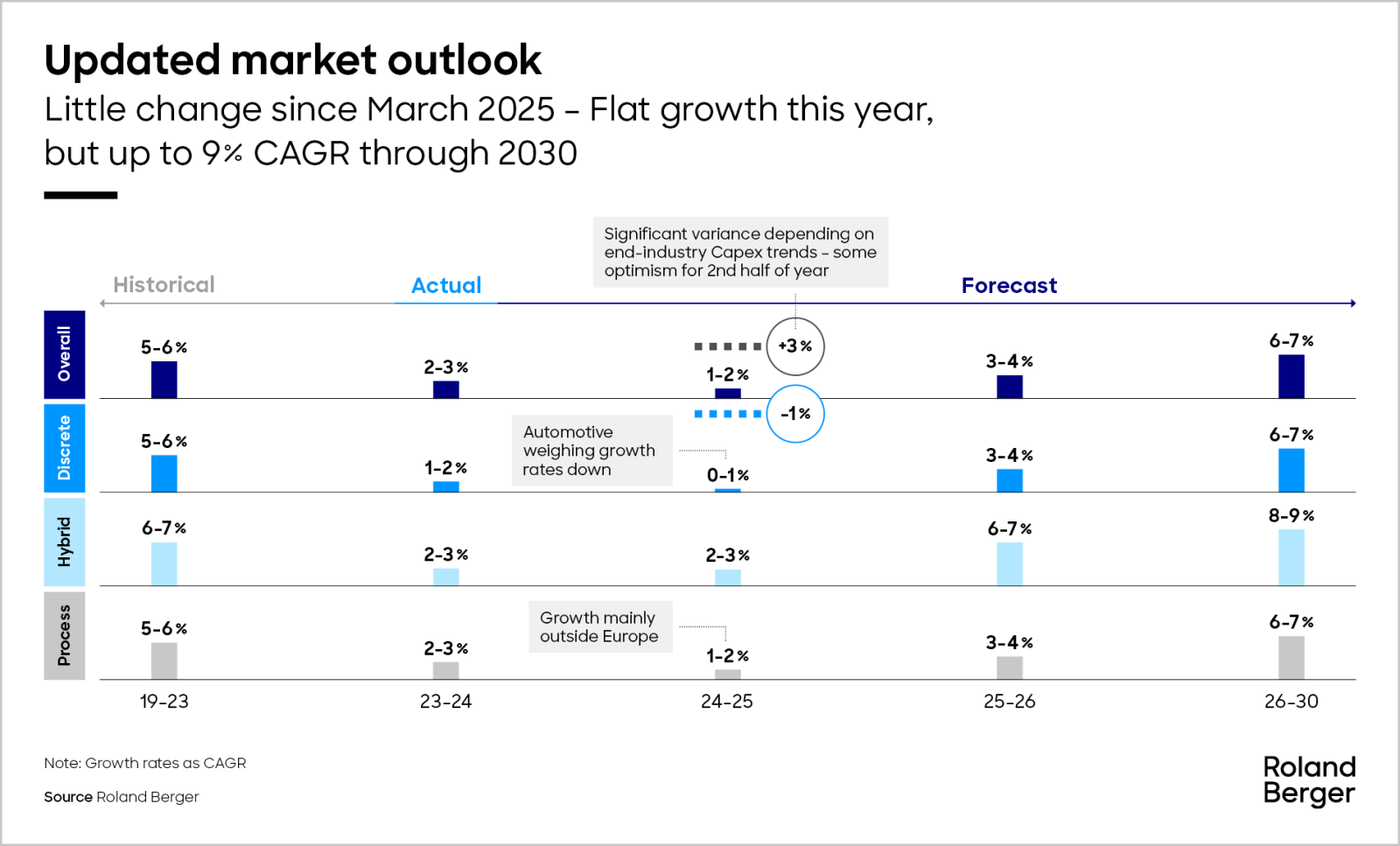

Our last report in March 2025 covered all aspects of the industrial automation market, from components to services and digital offerings. It outlined projections of a slight blip that would soften momentum in the industry 2025 before a return to more vigorous growth in the years ahead, discussing how organizations can best prepare to participate in the coming growth phase.

"2026 marks the first year with renewed growth momentum in industrial automation, setting the stage for a potential CAGR of up to 9% through 2030."

This new, shorter update picks up subtle changes in companies’ projections in the last few months and adjusts the industry outlook accordingly. But essentially, little has changed. 2025 was a year of more muted development, for many companies, the order intake remained below revenues. However, the long-term outlook now looks a little stronger, with 2026 being the first year with some growth momentum. Similarly, the International Federation of Robotics (IFR) estimates the 2025 installed number of new industrial robots increase slightly compared after 2 flat years with even stronger growth in 2026. Looking beyond 2026, potential catch up investments could drive CAGR growth of up to around 9% through 2030. We believe the realistic growth corridor is around 6-7% with some variance by region and end-industries.

"Future manufacturing will increasingly rely on standardized hardware and software-driven value, expanding automation’s reach even to smaller batch production."

Although the mood prevalent in Q2 was dampened to some degree by geopolitical and fiscal uncertainties, Q3 brightened their sentiment modestly as no further major (tariff) shocks materialized in the interim period. Most players still tracked close to their initial 2025 guidance.

Leading IA players are gradually rebounding from the 2022-24 slowdown, and early signs of recovery are not just anticipated but now visible. Discrete industries and selected process industries will remain subdued, but both medical & pharmaceuticals and FMCG should remain relatively strong.

We position some optimism on technological developments creating incentives for new investments. Future manufacturing will likely rely on a more standardized set of hardware elements with more of the value add coming from software – this will most likely have a positive impact on Return on Investment and increase the penetration of Industrial Automation solutions also for manufacturing sizes with smaller batch sizes. Refer also to the recent publication from The Economist on the “ChatGPT moment in manufacturing”. Additionally, a hot topic has been, especially in Europe, the topic of Automation in Defense production – yet this is not materially moving the needle on overall market growth yet.

In the US, manufacturing activity remains more or less steady. Manufacturing investments are edging down from their Q2 2024 peak but remain elevated, as reshoring and nearshoring initiatives – driven by changing tariffs and the pursuit of supply chain stability – offset the tail-off of IJA- and CHIPS-incentive–driven spending. New orders for capital goods remain volatile but continue to trend above 2024 levels on average. Meanwhile, orders for material handling equipment, though still down on the highs seen in 2022 through 2024, are holding relatively stable.

Transaction activity showed signs of life in 2024 but still lags behind historical averages. Europe and North America continue to dominate as target and buyer regions. Aside from the Asia-Pacific region, a general preference for intraregional deals remains intact.

Variance in end-markets and regions

In different segments, destocking went further in 2025 than many players initially expected. Accordingly, hopes that the second half of the year would be better failed to fully materialize.

While selling to automotive companies has been and still is tough, most end-industries are generally doing well – food & beverages and farming being prime examples. After the challenges of this year, 2026 should see a slight improvement followed by noticeably stronger growth through the remainder of the decade. Regionally, China is largely rebounding, we are taking an especially close look at the South East Asia economies who are gaining momentum on their journey of manufacturing automation. Europe looks set to remain somewhat more challenging, whereas North America appears to be in better shape going forward.

With 2025 behind us, we expect companies coming in on revenue around their guidance, we would expect a somewhat cautious optimistic outlook from them for 2026.with potentially a slightly cautious take on China in the short term. Given that China is currently the engine of growth in the world’s automation industry, this latter stance could potentially lead to a somewhat more balanced (i.e. less China-heavy) spread of growth globally.

Future Roland Berger market updates

Taking the March 2025 report as our baseline, Roland Berger plans to align future updates with the timing of key players’ quarterly updates. This cyclical adjustment will enable us to track market sentiment more closely and give readers faster access to data on emerging shifts, trends and expectations.

Sign up for our newsletter

Further readings