Practical advice on navigating challenges and exploiting growth opportunities in material handling and warehouse automation.

Material handling and warehouse automation outlook

By Ralph Mair and Sebastian Koper

Recovery, reinvention, and the road to 2030

After a turbulent period marked by post-pandemic overcapacity and economic uncertainty, the global material handling and warehouse automation industry stands at a critical inflection point. Investment cycles are shifting, technology adoption is accelerating, and the competitive landscape is continually evolving. For senior decision-makers, the challenge is clear: how to position their organizations to benefit from the sector’s anticipated recovery and long-term transformation, while navigating persistent risks and evolving customer expectations.

Market recovery and the new growth equation

The warehouse automation market’s trajectory over the past five years has been anything but linear. Following a surge in investment during the COVID-19 pandemic—driven by e-commerce expansion and supply chain disruptions — the industry faced a pronounced slowdown from 2022 to 2024. Overcapacity, inflation, and macroeconomic uncertainty led many customers to delay or cancel projects, particularly in consumer-driven sectors like retail and food & beverage.

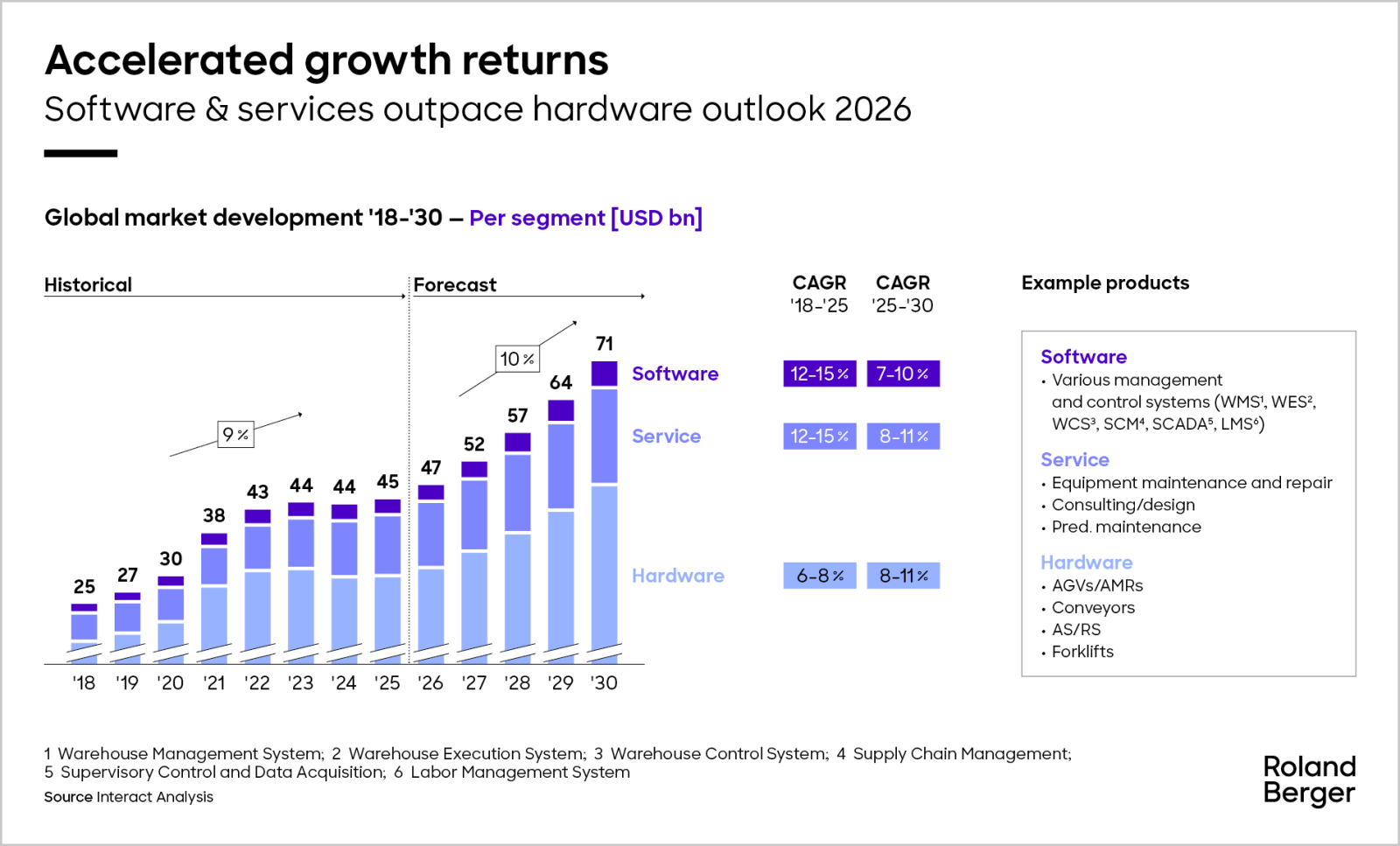

However, the outlook for 2026 and beyond is fundamentally more optimistic. The market is poised for a strong recovery, with a projected compound annual growth rate (CAGR) of 7–10% through 2030. The US, in particular, is expected to return to double-digit growth, fueled by greenfield warehouse projects, manufacturing reshoring, and renewed e-commerce momentum. Retail and logistics are set to drive approximately 75% of total market growth in the US between 2024 and 2030.

"Software and AI are rewriting the rules of warehouse value creation. The winners will be those who master integration, not just installation."

Competitive landscape: Consolidation and specialization

As the market recovers, the competitive landscape is both fragmenting and consolidating. Full-liners and specialized OEMs are balancing growth and profitability, while solution providers face margin pressure from cost inflation and commoditization.

Software providers—ranging from large players like SAP and Oracle to niche specialists such as BlueYonder and Manhattan Associates—are capturing high-margin opportunities. Orchestration and intelligence are becoming central to value creation.

M&A activity is reshaping the field. Players are building out hardware and software capabilities or doubling down on technology-agnostic integration. The ability to form and manage effective partnerships across hardware, software, and services will be a key determinant of long-term success.

Regional dynamics and end-market divergence

Americas: Resilience and reacceleration

The Americas remain the largest and most resilient market for warehouse automation. After a period of stagnation due to overcapacity and macro uncertainty, the region is expected to see renewed growth as vacancy rates decline and new investments are announced.

Retail and parcel segments are set to regain momentum, supported by Amazon’s regionalization strategy and the rebound in e-commerce volumes.

EMEA and APAC: Stabilization and catch-Up

Transitioning to other regions, EMEA faces short-term headwinds from inflation and geopolitical risks but is projected to stabilize and rebound post-2026.

APAC, particularly China, has seen a pause in warehouse construction, delaying recovery. However, the region is expected to deliver the fastest long-term growth as modernization and automation catch up with global peers.

End-market nuances

Retail and food & beverage together account for roughly 65% of the global market, with strong concentration in the Americas and EMEA. Manufacturing and life sciences are steadier, with manufacturing expected to rebound strongly post-2026.

Parcel automation, after a period of capex cuts, is projected to pick up at a double-digit CAGR from 2026 onward.

Mobile automation and the rise of AI

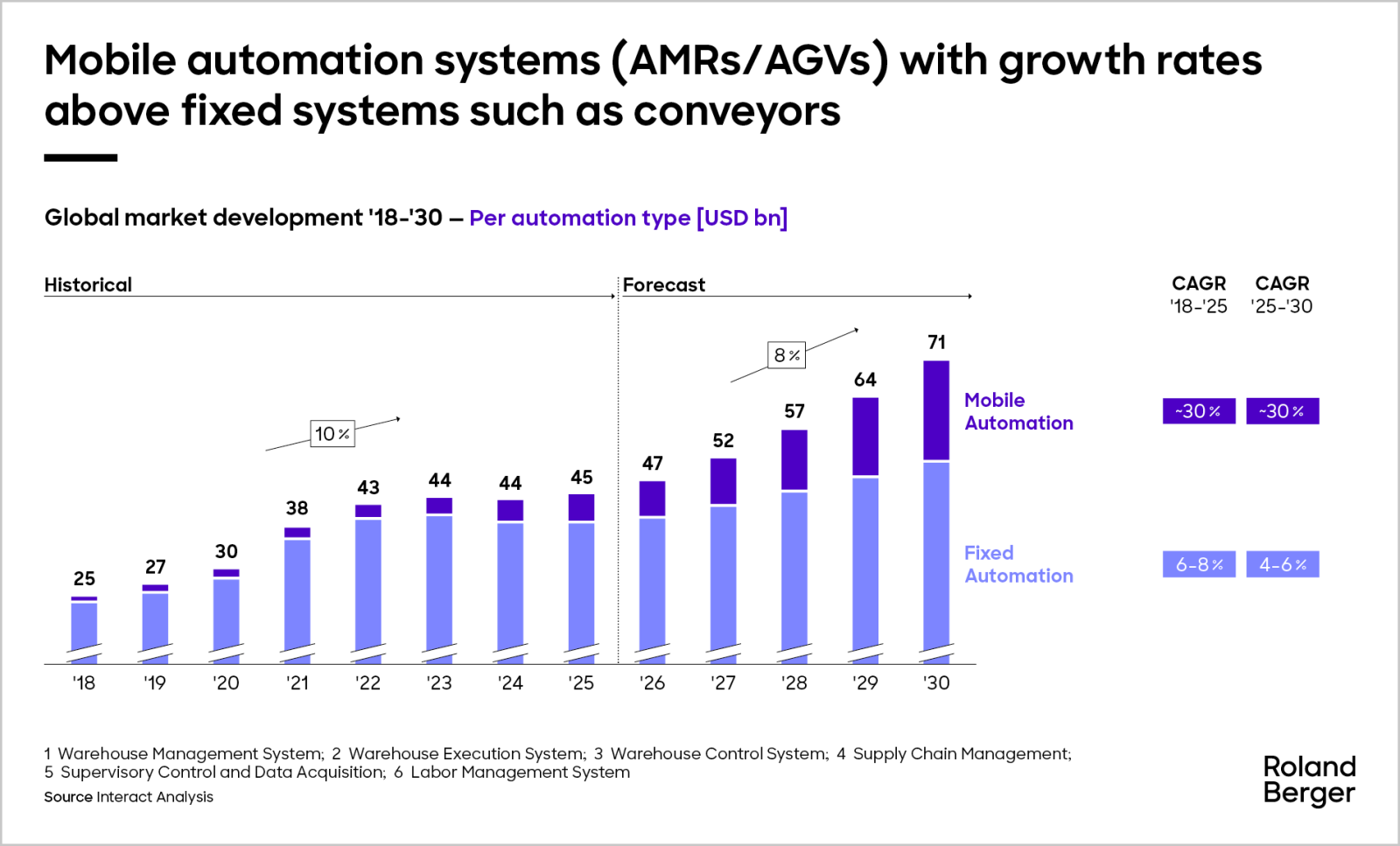

Perhaps the most dynamic segment is mobile automation, including Autonomous Mobile Robots (AMRs) and Automated Guided Vehicles (AGVs). These technologies are forecast to grow at a CAGR of approximately 30% between 2025 and 2030—far outpacing fixed automation solutions like conveyors and sorters.

The advantages are clear: mobile systems offer faster deployment, greater flexibility, and easier scalability. This enables operators to adapt to fluctuating demand and SKU complexity.

At the same time, artificial intelligence is moving from hype to practical application within mobile automation. AI-enabled navigation, fleet management, and real-time orchestration are becoming differentiators for AMR and AGV solutions. While many use cases are still in the early stages of adoption, the direction is unmistakable: future competitive advantage in mobile automation will hinge on the ability to leverage data and automation for continuous optimization.

Strategic implications: decisions for leaders

"The next five years will separate the agile from the obsolete — automation is no longer optional, it’s the backbone of competitive supply chains."

Rethinking investment timing and risk

The timing of investment is a central strategic question. While the consensus points to a market recovery beginning in 2026, downside risks remain—particularly if tariffs, inflation, or geopolitical tensions persist.

Some scenarios suggest that a prolonged period of uncertainty could delay the rebound until 2028, with a subsequent catch-up in investment. Leaders must balance the risk of acting too early (and facing continued volatility) against the risk of missing the next wave of growth.

Navigating the value chain and partner ecosystem

The warehouse automation value chain is becoming more complex and interconnected. System integrators—especially those with deep end-market experience—are increasingly critical for customers lacking in-house expertise.

However, the market is also seeing the rise of technology-agnostic integrators, specialized OEMs, and pure-play software providers. M&A activity remains high, as players seek to expand their capabilities and secure their position in the evolving ecosystem.

For decision-makers, the choice of partners and suppliers is more consequential than ever. Reliability, integration expertise, and the ability to deliver end-to-end solutions are key purchasing criteria. Switching barriers are highest for lifecycle services, making initial integration decisions particularly sticky.

Responding to labor and consumer pressures

Labor shortages and rising wage costs are persistent drivers of automation adoption. Warehousing and logistics roles are increasingly difficult to fill, with high turnover and growing regulatory pressures.

Automation is not just a cost-saving measure—it is becoming essential for maintaining operational continuity and meeting service-level expectations.

Consumer behavior is also reshaping the industry. The demand for faster delivery, broader product selection, and real-time information is pushing operators to invest in high-throughput, flexible fulfillment systems. E-commerce growth, after a brief post-pandemic plateau, is once again accelerating, particularly in retail and parcel segments.

Technology, integration, and the future of competition

As the material handling and warehouse automation industry enters its next phase, the winners will be those who anticipate and adapt to structural shifts rather than simply riding the recovery. The convergence of e-commerce growth, labor dynamics, and technology innovation is creating both opportunities and risks.

Leaders must make deliberate choices about where to invest, whom to partner with, and how to future-proof their operations. The imperative is clear: build flexibility into capital allocation and stay close to both end-market trends and the evolving partner ecosystem.

The next five years will reward those who can navigate complexity, manage uncertainty, and capture the upside of a sector in transformation.

Sign up for our newsletter

Further Readings