The coming together of the physical and digital worlds is giving a new boost to innovation in healthcare. How will that impact markets, players and patients?

MedTech@Hospital 2021

How Covid-19 and the Hospital Future Act reshuffled MedTech investments

Roland Berger’s annual study of German hospital MedTech trends reveals that MedTech companies should adjust their offering. This year’s annual Roland Berger MedTech@Hospital survey of 600 executives from the largest hospitals in Germany is proof that hospital priorities have changed this year. Two key factors are driving this change.

"MedTech companies must be aware of the growing focus on sustainability and reflect it in their messaging, operations, and corporate strategy."

First, the Hospital Future Act ("Krankenhauszukunftsgesetz" or KHZG) of 2020 grants over EUR 4 billion to qualifying German hospitals for investments in digitization, IT security, and emergency care. Consequently, German hospitals have shifted their focus to align with this public funding.

Second, the large and specific MedTech investments seen during COVID-19 (such as ventilation systems) are largely exhausted now. As such, hospitals are reprioritizing their spending to improve their digital technology and processes. Moving forward, here’s what the industry needs to know.

Key findings from this year’s study

While the full report provides greater detail, here are the top five observations from this year’s study:

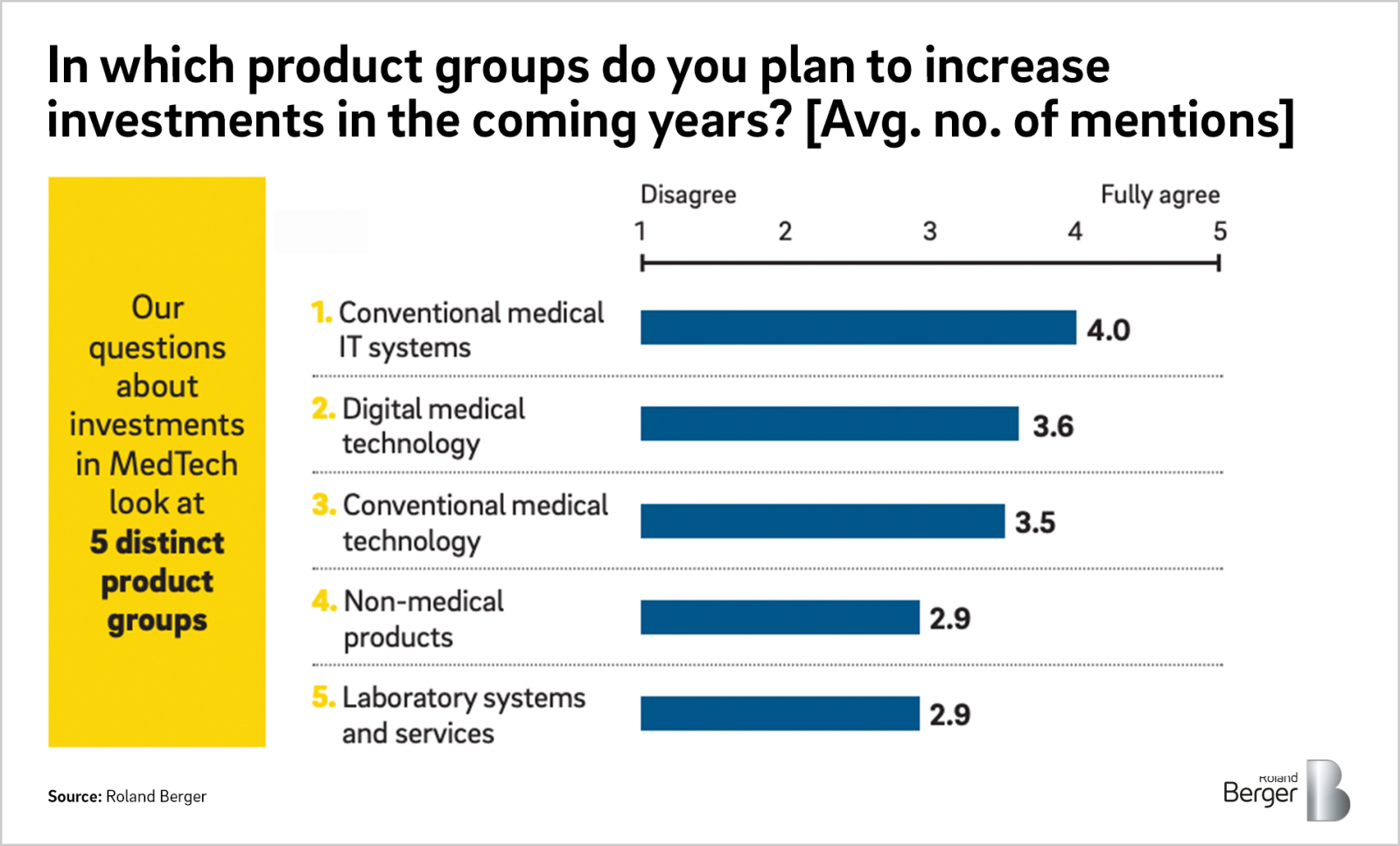

Conventional IT systems are the top investment priority for hospitals

- To improve their core capabilities, German hospitals are investing in digital and conventional IT systems and pausing new purchases of intensive care equipment, laboratory systems, and non-medical products such as beds, furnishing, and medical carts.

- Larger hospitals in particular plan to invest in digital medicine solutions, especially telematics and telemedicine.

- Although paying the full purchase price is still the most common method, the attractiveness of pay-per-use and of full service models is increasing significantly.

- Most hospitals, particularly small and private institutions, will continue to outsource their maintenance services to OEMs or third parties.

- Sustainability is a relevant purchasing factor for almost all respondents, but hospitals' willingness and ability to pay extra for it is not keeping pace.

"The crisis-driven growth in hospital capital spending is coming to an end. Hospitals are now focusing on meeting their pent-up demand for products such as digital patient portals."

In summary, the short-term increase in hospital investments driven by COVID-19 is coming to an end. Now hospitals are planning to spend on pent-up demand for products such as digital patient portals , decision support systems, and emergency care.

How MedTech companies can respond

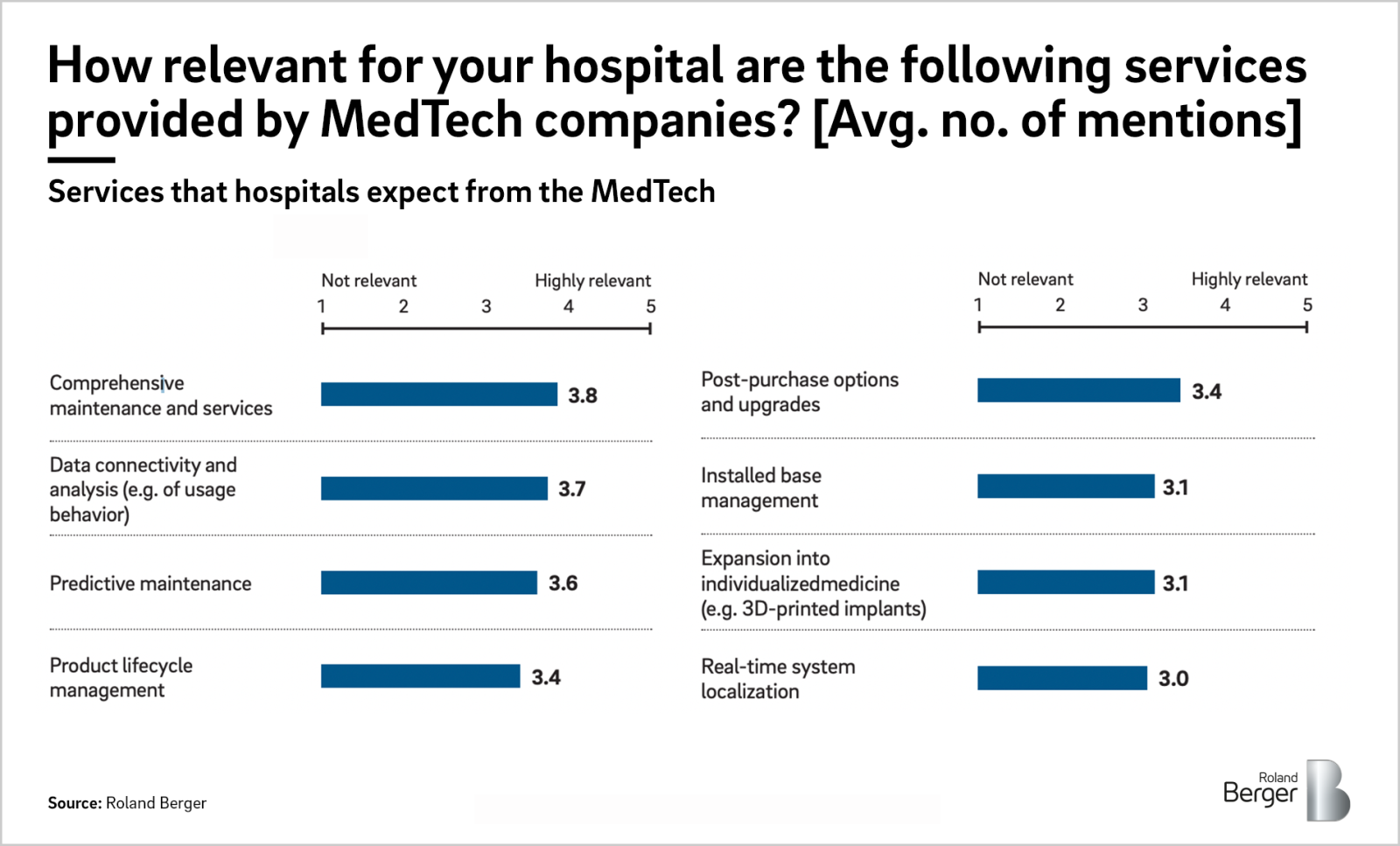

When deciding how to invest in their futures, our survey revealed that hospitals are especially interested in keeping down their operating costs. To that end, hospitals are increasingly keen to delegate maintenance and services to MedTech companies and other third parties, especially in the areas of predictive maintenance, data connectivity, and usage analysis to improve workflows.

Given this desire for cost-efficiency and the financial stress on many hospitals, we see in our survey that MedTech companies should offer more flexible financing, leasing, and usage-based models to hospitals moving forward. Additionally, with 90% of hospital executives saying sustainability is a factor in their purchasing decision, MedTech companies must be aware of the growing focus on sustainability and reflect it in their messaging, operations, and corporate strategy.

Outsourced comprehensive maintenance is a top demand

Driven by the ongoing COVID-19 pandemic and new legislation such as the KHZG, MedTech companies must adapt their focus. With this in mind, we offer the following recommendations to MedTech firms operating in Germany and beyond:

- Understand your customers and their challenges. What worked before and during COVID no longer applies. Today, MedTech leaders must consider the updated appetite for hospital investment. On this basis they can then define a distinct offering that is in line with customer needs, such as offering more affordable devices and predictive maintenance to help hospitals keep costs down.

- Offer flexibility. Today, hospitals of all types and sizes are looking for flexibility in response to their limited financial resources. MedTech players should offer flexible financing models and options for reducing hospitals' operating costs. Players should also strive to establish long-term partnerships with hospitals , allowing them to focus on helping patients while relinquishing their technical equipment to outside expertise.

- Think ahead on sustainability. MedTech companies must mirror the concerns of hospitals and make sustainability a priority now. Getting ahead of the competition on sustainability should include assessing their current sustainability footprint, defining a strategy for improving that footprint, and sharing these goals in external communications.

Thank you for reading. To learn more, please read the full survey or contact us.

Request the full publication here

Register now to download the study to learn more about how Covid-19 and public funding are shaping hospitals´ investments in medical technology. Get also regular insights into Health & Consumer topics.

Further readings