Learn how the AI revolution creates new winners and losers in the engineering products and services.

Satellite convergence

Why telco operators must prepare for the next infrastructure revolution

Direct-to-cell technology and vertical integration are transforming satellite connectivity from a niche solution into a fundamental competitive threat to traditional mobile operators.

"Satellite is no longer a niche layer of connectivity — it is becoming the third dimension of telecom infrastructure, alongside fixed and mobile. Operators who treat it as optional will find themselves structurally disadvantaged."

The telecommunications industry is at an inflection point. For decades, satellite communications occupied a narrow and expensive niche: emergency backup systems, remote maritime connectivity, and specialized government applications. That era has ended. Falling launch costs thanks to reusable rocket technology, and breakthroughs in direct-to-cell capabilities have fundamentally changed the economics and scope of satellite telecommunications. Satellite coverage is shifting from optional premium service to essential infrastructure, creating a third dimension of coverage alongside fixed and mobile networks for telecom operators.

The implications for legacy operators are significant. When SpaceX’s Falcon 9 reduced launch costs by roughly 80% compared with traditional systems — from about $9,000 per kilogram to as low as $1,200 — it did not just make space access cheaper. It unlocked an entirely new business model. Starlink has already deployed more than 9,400 satellites, with plans to expand to around 30,000. The constellation delivers consumer broadband speeds of 100–300 Mbps at prices that match or undercut terrestrial offers in many markets. More importantly, Starlink’s direct-to-cell service launched commercially in July 2025 with T-Mobile, enabling standard smartphones to connect directly to satellites without hardware modifications.

This convergence creates a new reality for traditional operators: the strategic playbook that drove mobile–fixed convergence over the past decade must now be repeated with satellite. Operators that dismissed satellite as peripheral to their core business are discovering that spectrum ownership, network control, and customer relationships — long-standing sources of telecom advantage — are exposed to disruption from vertically integrated satellite players operating with different cost structures and deployment models.

The structural advantage of vertical integration and long term visibility

"Vertical integration in satellite — from launch to spectrum to service delivery — creates a cost and speed advantage that traditional telecom models are not designed to match."

SpaceX’s position illustrates why satellite telecommunications differ from previous technology cycles. The company controls the entire value chain: satellite manufacturing, launch, network operations, ground infrastructure, and customer delivery. This vertical integration creates a self-reinforcing flywheel that is difficult for competitors to replicate.

The economics are decisive. Starlink’s internal launch demand from its own constellation ensures high utilization of Falcon 9 rockets. Flying more than 100 missions annually creates manufacturing scale effects that competitors launching 6–10 times per year cannot match. High launch cadence drives learning-curve benefits — more than 400 Falcon 9 launches have built deep operational expertise in recovery, refurbishment, and turnaround. SpaceX can price launches at around $28 million while sustaining margins, undercutting rivals that must recover full mission costs without internal demand.

The constellation follows the same logic. Starlink generated roughly $8 billion in revenue in 2024, split approximately 60% consumer, 30% government, and 10% enterprise. This revenue funds both satellite production and next-generation development. Cash flow from current satellites supports Starship development, targeting launch costs below $250 per kilogram — another major step down from current levels. External customers buy capacity, but Starlink controls deployment priorities, orbital architecture, and technology evolution without dependence on third-party manufacturers or launch schedules.

Traditional satellite operators lack this structural advantage. Companies such as Eutelsat, SES, and Viasat procure satellites from manufacturers like Thales Alenia Space or Airbus Defence & Space at costs of $60–150 million per MEO or GEO satellite. They buy launch services from ULA, Arianespace, or SpaceX at market rates, without internal volume discounts. This fragmented value chain introduces coordination costs, schedule risk, and structural economic disadvantages that operational efficiency alone cannot offset. On top of that they do not have the long term visibility that allows to plan with confidence in the short to medium term.

Without a clear consolidation of the value chain and long term commitment from European government, the European ecosystem will remain structurally disadvantaged.

Direct-to-cell: The technology that changes everything

"Direct-to-cell changes the rules of the game: when standard smartphones can connect directly to satellites, coverage is no longer limited by towers — it becomes a function of orbital architecture."

The breakthrough that shifts satellite from complementary to competitive is direct-to-cell connectivity. Starlink’s second-generation V2 Mini satellites include functionality that enables standard 4G and 5G smartphones to connect directly to space-based infrastructure using existing LTE bands. No specialized terminals and no hardware modifications are required. Devices can fall back to satellite when terrestrial coverage is unavailable.

The technical approach reflects a sophisticated spectrum and regulatory strategy. Starlink’s initial direct-to-cell deployment uses PCS G-block spectrum (1910–1915 / 1990–1995 MHz) leased from T-Mobile in the United States. Regulators have also approved additional frequencies around 1.9 GHz under specific leasing arrangements. This partnership model supports rapid rollout while Starlink pursues longer-term spectrum control through its planned $17 billion acquisition of EchoStar spectrum assets, including 40 MHz of AWS-4 S-band and 10 MHz of H-block PCS spectrum with nationwide US coverage.

The strategic direction is clear: Starlink is moving from a dependent partner toward a potential standalone mobile operator. Today’s model relies on MNO partnerships for terrestrial spectrum access. Spectrum ownership would make such partnerships optional, improving leverage, economics, and strategic flexibility. Over time, this supports a hybrid satellite–terrestrial network that could scale to around 15,000 dedicated direct-to-cell satellites delivering full 5G-class capacity.

In Europe, the structure differs but the pressure is similar. The region has more than 180 facilities-based mobile operators across markets that typically support three to four MNOs each. This fragmentation creates partnership opportunities for satellite providers, especially with smaller operators willing to lease spectrum. Starlink increased EU lobbying activity in 2025, engaging with the European Commission on satellite spectrum allocation, direct-to-cell approvals, the EU Space Act, and the spectrum implications of the EchoStar acquisition.

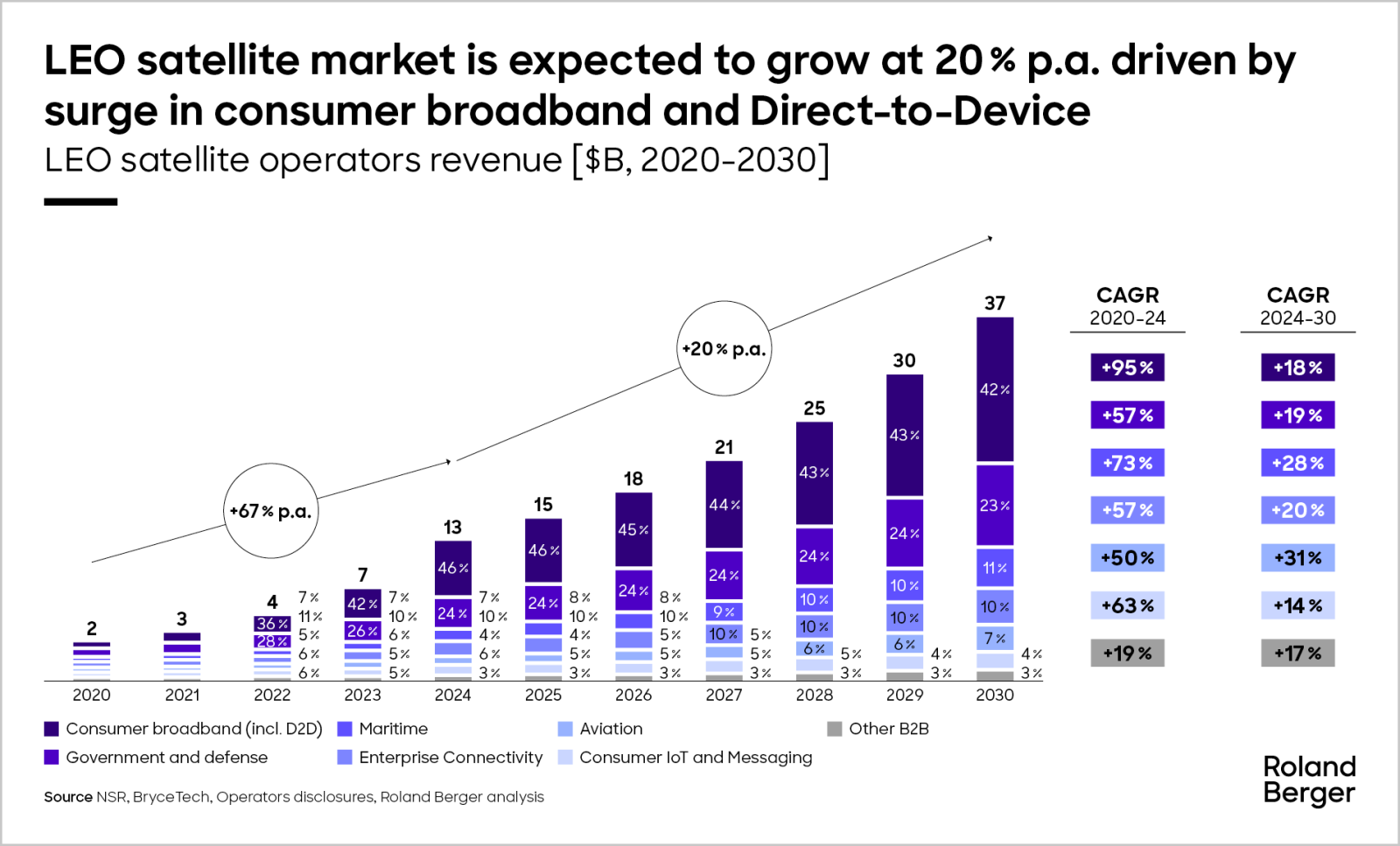

Market economics: From niche to mainstream

The financial trajectory of LEO satellite services highlights the scale of the coming shift. The LEO satellite operator market is projected to grow at around 20% annually, reaching roughly $53 billion by 2030. Consumer broadband remains the main growth engine, while direct-to-device services are emerging as the next major revenue stream.

Current pricing already challenges terrestrial benchmarks. In the United States, Starlink residential service costs about $120 per month for 100–300 Mbps, compared with typical terrestrial broadband prices of $60–80 for similar speeds. The premium is noticeable but acceptable in underserved areas. In Europe, Starlink pricing of roughly €50–70 per month competes directly with rural broadband offers. Some operators now resell Starlink-based fixed wireless access, acknowledging that satellite can be more cost-effective than fiber in low-density regions.

Enterprise and government segments show even stronger economics. Maritime connectivity can generate $30,000–300,000 per vessel annually because LEO satellites provide mission-critical coverage where alternatives are limited. Aviation shows similar dynamics, with airlines paying premium rates for in-flight connectivity that matches passenger expectations shaped by terrestrial networks.

Government and defense contracts provide stability that supports commercial expansion. Starlink’s Starshield program secured an $1.8 billion contract with the US National Reconnaissance Office, plus roughly $537 million in Pentagon-related support for Ukraine connectivity. These multi-year commitments provide predictable, high-margin revenue streams.

Strategic implications for legacy operators

Satellite convergence forces difficult strategic choices for telecom operators. Satellite coverage is becoming mandatory, but most operators lack a clear path to competitive delivery on their own.

Partnership models currently dominate operator responses. Vodafone formed a joint venture with AST SpaceMobile and signed agreements with Amazon’s Project Kuiper for backhaul and fixed wireless access. Orange partnered with Starlink for messaging and geolocation services and with Eutelsat OneWeb for global backhaul. Deutsche Telekom announced direct-to-cell pilot agreements with Starlink. These partnerships extend coverage without large capital commitments, but they also shift strategic control to satellite-native providers that own the infrastructure and often the service roadmap.

The path forward

Operators need a coherent satellite strategy that treats the technology as core infrastructure rather than a niche extension.

First, accept satellite as the third dimension of convergence. Fixed–mobile convergence took decades to mature. Satellite convergence will follow a similar path at a faster pace. Operators without satellite integration will face disadvantages in enterprise, maritime, aviation, and rural markets where coverage gaps matter.

Second, treat spectrum as a rising-value strategic asset. Regulatory “use it or lose it” pressure can encourage divestment of underutilized bands. That impulse should be resisted where frequencies are compatible with direct-to-cell services. These bands will become more valuable as satellite providers seek access and hybrid architectures expand.

Third, pursue partnerships from a position of strategy, not reaction. Many current agreements appear defensive. Strong partnerships should guarantee long-term capacity access, preserve customer ownership, and maintain optionality. Simple resale arrangements provide short-term coverage gains but create long-term dependency.

Satellite convergence is no longer theoretical. Large LEO constellations operate at scale. Direct-to-cell connectivity works with standard smartphones. Launch costs have fallen by 80–90% and continue to decline. The question for telecom operators is no longer whether satellite will matter, but how quickly they can adapt their business models, investment priorities, and partnership strategies to compete in a network landscape that increasingly extends into space.

Sign up for our newsletter

Further readings

Milan Office, Southern Europe