Building the next generation of financial services

Financial technology is reshaping financial services across the Gulf Cooperation Council (GCC) – and AI is the catalyst. What was once a largely cash-driven landscape is evolving into an intelligent, data-first ecosystem where fintechs, banks and telecom operators redefine how consumers engage with financial services. Roughly USD 260 billion of incremental GDP is at stake for the region by 2030, and financial services are poised to capture a sizable share as AI becomes integral to every fintech vertical.

Several forces are driving this convergence. GCC consumers are already digital natives: Mobile wallet penetration surpassed 60 percent in the United Arab Emirates (UAE) in 2024,2 for instance, and smartphone usage is on track to reach 97 percent by 2025.3 Regulators in GCC countries have established AI sandboxes, electronic Know Your Customer (e-KYC) frameworks and open-banking regimes that lower barriers to innovation while safeguarding systemic stability. Meanwhile, abundant venture capital and sovereign cloud capacity allow Fintech startups and incumbents alike to scale AI solutions.

Practical applications are moving from pilot to production. AI-driven fraud detection has reduced false-positive rates by up to 90 percent,4 automated credit models now deliver real-time loan decisions and conversational chatbots resolve as much as 80 percent of customer queries without human intervention.5 The business impact is significant: Customer acquisition costs can fall by three-quarters, compliance workloads by two-thirds and time-to-market for new products by nearly half. Together, these advances mark a structural transition from digital banking to AI-enabled Fintech.

"AI converts financial complexity into instant clarity."

Financial technology – or fintech – refers to applications that enhance, support or replace the functions of traditional financial and banking services providers. The industry is predicted to reach USD 882 billion by 2030. The GCC region has emerged as a forerunner over the past decade. As of 2024, the UAE hosted 329 active fintech companies, while Saudi Arabia had 224 as of Q2 2024. Half the GCC population used a digital wallet in 2024, and more than 40,000 companies have adopted "buy now, pay later" (BNPL) solutions.

The acceleration of fintech adoption in the GCC reflects three main drivers: a pro-fintech regulatory stance, a youthful and tech-savvy demographic, and unmet needs in traditional banking.

Fintechs in the region are expanding into more specialized offerings through embedded fintech, allowing non-financial businesses to integrate payments, lending and insurance directly into their platforms. The embedded fintech market in the region is projected to reach USD 2 billion by 2030.

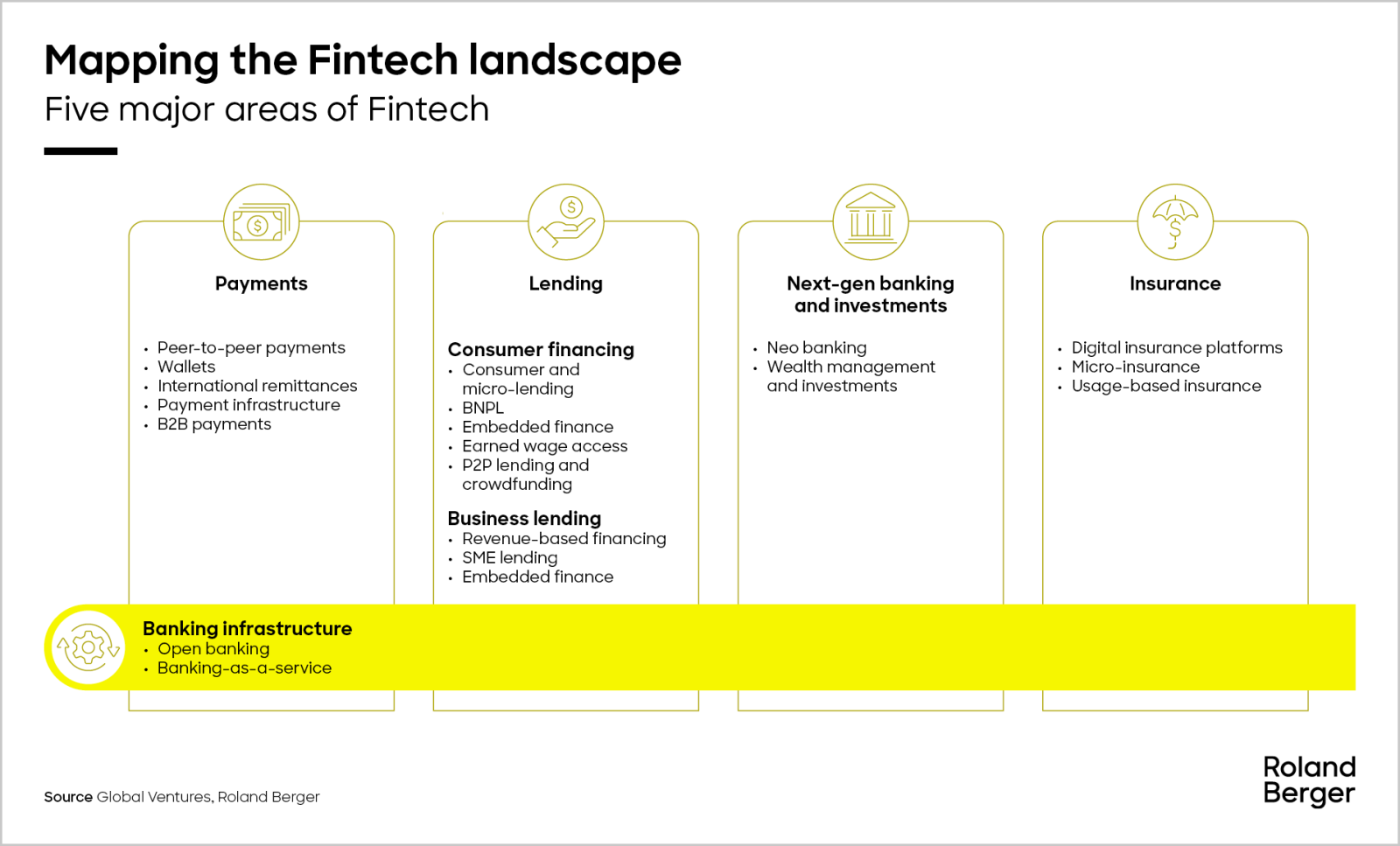

Mapping the fintech landscape.

AI as a strategic lever for growth

3.1. Developments in AI – globally and in the GCC

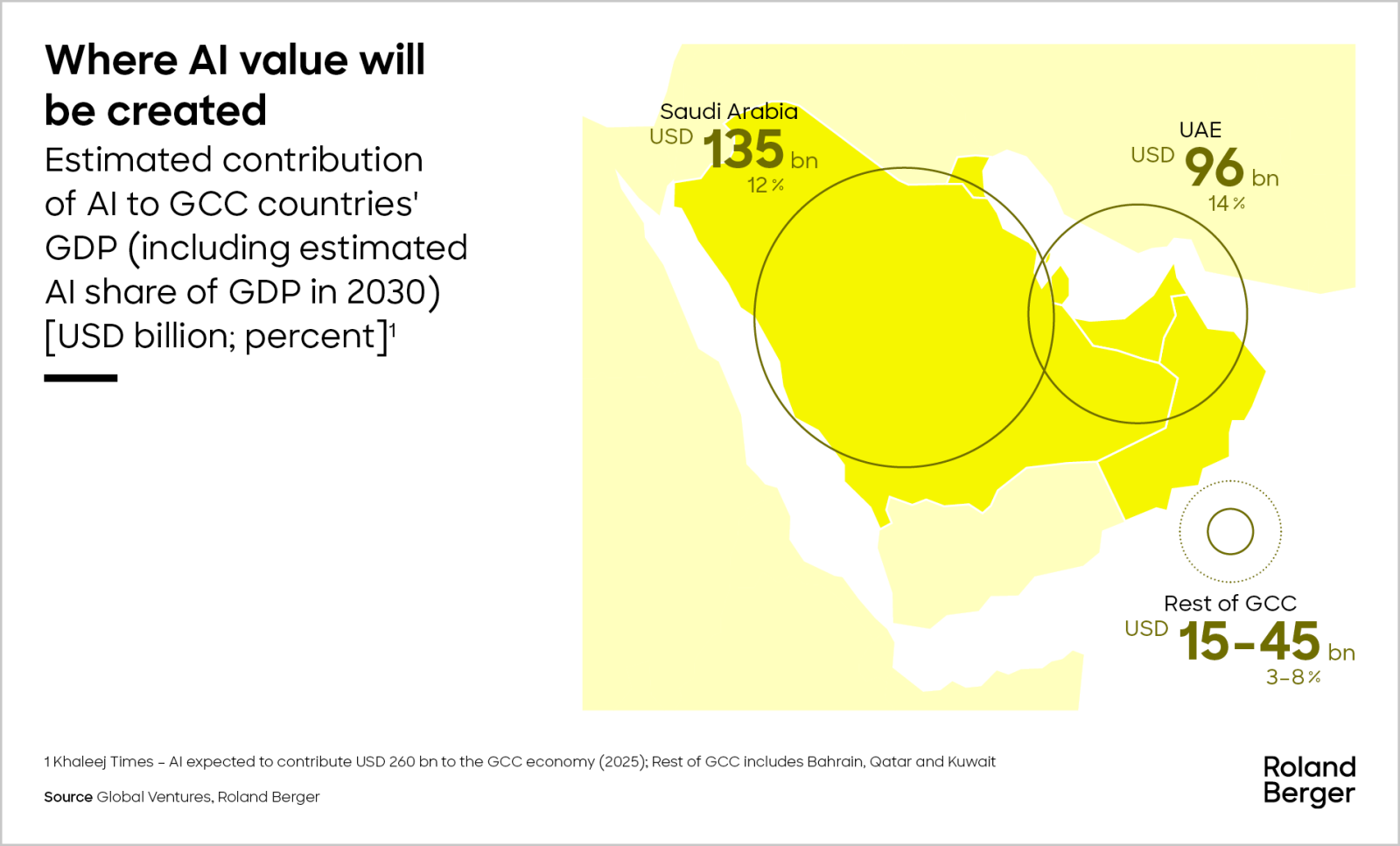

The global surge in AI has accelerated across industries and functions, driven by breakthroughs in large-language models. Today, roughly 80 percent of organizations deploy AI in at least one business area. Economist Impact projects that AI could generate up to USD 260 billion in economic contribution to GCC GDP by 2030, with banking estimated to contribute almost 14 percent to the GCC’s GDP by 2030. Governments are actively nurturing this ecosystem: the UAE appointed the world’s first "Minister of Artificial Intelligence" and integrated AI into school curricula; Qatar and Saudi Arabia have launched multi-billion-dollar AI incentive packages.

3.2. Horizontal and vertical applications

AI solutions in fintech can be categorized as horizontal (broadly applicable, e.g., fraud detection, chatbots) and vertical (sector-specific, e.g., credit scoring, underwriting, robo-advisory). Vertical AI is rapidly outpacing horizontal, delivering sharper value and compliance advantages.

3.3. Direct benefits

AI is driving broad operational improvements, especially in process optimization. It reduces manual effort, accelerates decision-making and improves turnaround times. In marketing and sales, AI can lower customer acquisition cost by up to 75%. Underwriting costs can be reduced up to 90%. Compliance functions benefit, particularly in KYC processes, with cost savings of 60–80%. On the revenue side, AI enhances speed and scalability, reducing time-to-market for new products by up to 40%. In customer service, AI platforms handle routine inquiries, accelerate resolution times and provide 24/7 support, delivering up to 150% ROI without increasing staffing needs.

Where AI value will be created.

Making AI work: An implementation pathway

Step 1 – Strategic prioritization: Map potential AI initiatives by business impact and implementation complexity to target high-value, quick-win use cases.

Step 2 – Build or buy: Decide between custom AI-native development or integrating third-party tools based on speed, control, and cost.

Step 3 – Governance & talent integration: Embed AI into core workflows with cross-functional oversight, starting with a narrow MVP to validate and refine.

The road ahead: A regional opportunity for AI-first fintech

AI is now a defining force in fintech. Regulators must build AI-specific sandboxes and co-design compliance frameworks. Financial incumbents should invest in core AI domains and partner with AI-native fintechs. Investors should prioritize teams with deep AI execution experience and robust governance. Founders must design AI-native solutions tailored to regional needs and regulatory expectations.

For more insights, case studies, and practical guidance, download the full report.

Download the full PDF

Study

The AI-fintech transformation in the GCC

Discover how AI is transforming the fintech landscape across the GCC, driving operational efficiency, innovation, and growth. Explore regulatory advances, real-world case studies, and actionable strategies for banks, startups, and investors in the region.

![{[downloads[language].preview]}](https://www.rolandberger.com/publications/publication_image/Roland_Berger_25-2386_AIFintechTransformation_Cover_download_preview.png)