Generative AI is transforming information technology functions across the Middle East. We look at the challenges and opportunities of GenAI.

The age of intelligent services

How AI is transforming the digital services industry

For decades, the digital services industry has scaled by adding people. Consulting and IT service firms built their business models on providing the right skills at the right place and price — expanding headcount to match demand. That model has reached its limits. Artificial intelligence (AI) is breaking the traditional link between manpower and value creation.

"AI is shifting the center of gravity in our industry — from scaling people to scaling know-how. The winners will be those who can turn data, models, and human judgment into a seamless system of value creation."

Across the industry, AI is beginning to act not just as a tool, but as a production factor. Generative and agentic AI can already design, execute, and continuously improve workflows once handled by large teams. This shift is rewriting the economics of consulting, software, and digital delivery. The firms that thrive in this new environment will not be those that deploy the most people, but those that embed the most intelligence.

AI marks the beginning of an *intelligence-scaled* era — one in which creativity, analysis, and execution are accelerated by machines capable of learning, reasoning, and adapting at scale.

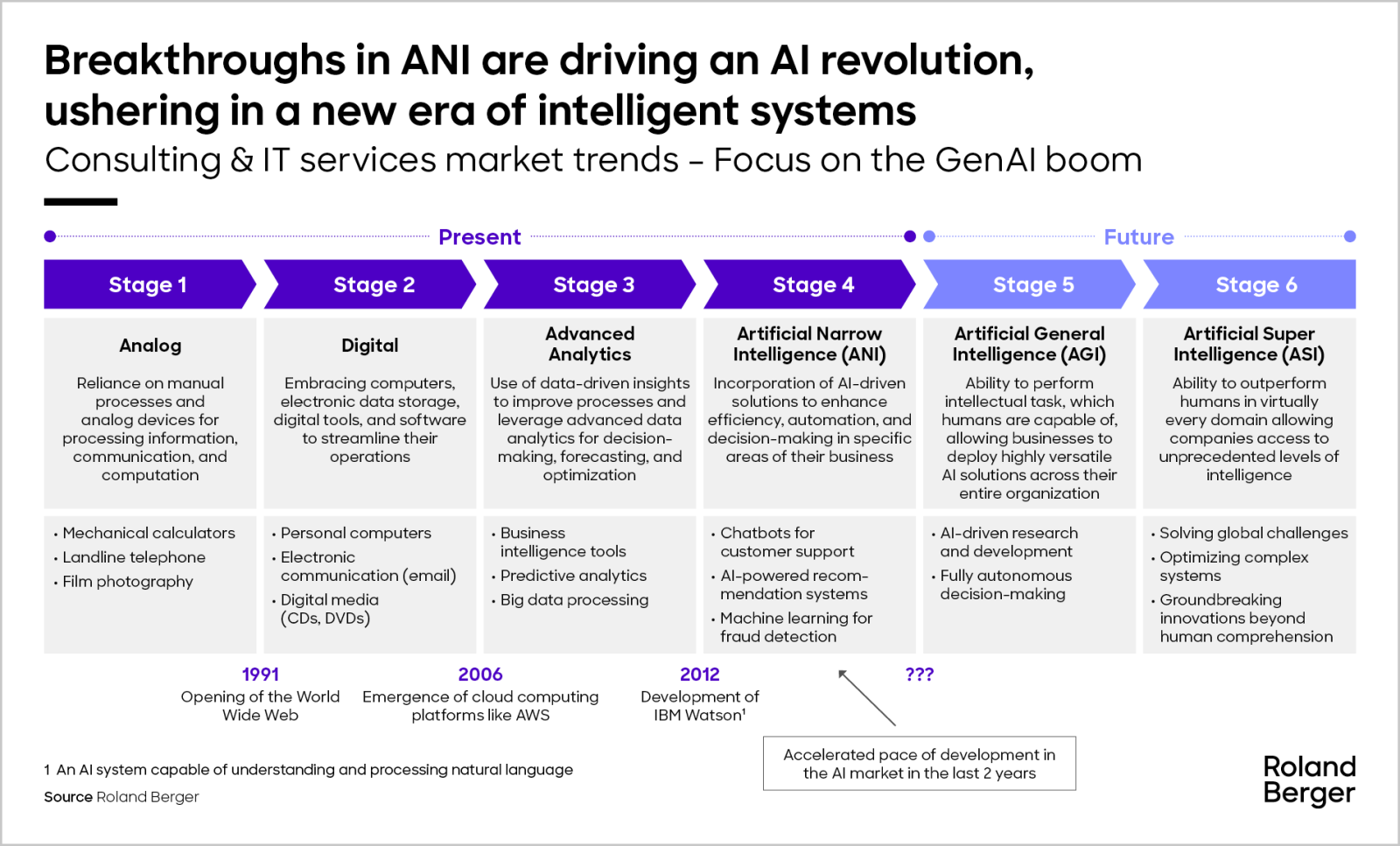

From automation to autonomy

The evolution from automation to autonomy has been fast and profound. From early digital tools to today’s emerging frontier of agentic systems, the industry has moved from assistance to orchestration.

In earlier phases, AI performed narrow, repetitive tasks: code suggestions, report generation, data extraction. Today’s agentic AI is self-directing. It can reason across datasets, take context into account, and execute multi-step decisions autonomously. Tomorrow, AGI may be able to make fully autonomous decisions, creating on its own new strategies to overcome new obstacles.

For service providers, this means rethinking their delivery architecture entirely. The future operating model will not be built on pyramids of people but on networks of intelligent systems — machines managing machines, supervised by experts focused on judgment, governance, and creativity. AI moves from the edge of operations to the center of the value chain.

A rapidly expanding market

The global consulting and IT services sector, valued at around €755 billion, continues to grow at a steady pace. But beneath that stability lies explosive momentum in one segment: AI-related services, expanding at over 20% percent annually.

This growth is driven by both sides of the market equation. Clients are demanding measurable outcomes — efficiency, quality, and innovation delivered faster and cheaper. Providers, meanwhile, face cost pressure, talent scarcity , and the need to defend margins. AI offers the leverage they need: more output, less dependency on human scale.

At the same time, competitive boundaries are dissolving. Hyperscalers, software publishers, and AI-native consultancies are moving into each other’s domains. Traditional service firms now compete with technology platforms that integrate strategy, implementation, and operations into one intelligent stack.

For decision-makers, this is no longer a question of adopting AI tools; it is about redefining the firm’s strategic position in a radically changing market.

The dual impact of AI

AI is transforming both the offer and the engine of digital services.

On the client side, demand is shifting toward AI-enabled solutions that deliver clear, quantifiable results. From predictive analytics to autonomous process management, clients expect technology to deliver outcomes — not reports. On the delivery side, firms are deploying AI internally to increase speed, reduce cost, and improve consistency.

By 2027, nine out of ten digital service providers will use generative AI in software development. The productivity gains are already visible: 30 to 50 percent improvement in coding, testing, and documentation performance.

This “dual transformation” — AI in both the client offering and the delivery backbone — is redefining competitiveness. Service firms that use AI to deliver smarter products and run smarter operations will widen the performance gap dramatically in the years ahead. Those who treat it as a back-office tool will fall behind.

"We are moving from service delivery built on pyramids of talent to operating models orchestrated by AI. This transition isn’t incremental — it’s a structural reinvention of how consulting and digital services create impact."

Six forces reshaping the industry

The transformation is being accelerated by six structural forces that no provider can ignore.

First, AI commoditization is pushing firms to differentiate through application design, proprietary data, and integration capability rather than technology access.

Second, platform convergence is underway. Hyperscalers and AI-native consultancies are entering the same value space, combining infrastructure, data, and strategy.

Third, sustainability constraints — in energy consumption and chip availability — are forcing a shift toward more efficient and environmentally responsible “green AI.”

Fourth, a cognitive leap in AI reasoning is imminent. Within two years, smaller, domain-specific models will autonomously manage complex multi-step tasks, from generating architectures to orchestrating project delivery.

Fifth, talent transformation is accelerating. As routine tasks are automated, demand is shifting toward hybrid skill sets that combine business design, technology fluency, and ethical judgment.

Finally, data sovereignty is becoming the new strategic moat. As public datasets reach their limits, ownership and control of proprietary domain data are emerging as the most defensible advantage in the market.

Together, these forces are collapsing traditional industry boundaries. The next generation of service firms will not sell hours, licenses, or even methodologies — they will sell systems of intelligence that scale autonomously.

Reinventing operations and talent

Inside service organizations, AI is transforming how work is planned, executed, and managed. Code assistants accelerate development cycles; AI copilots document and test automatically; retrieval-augmented generation improves quality assurance. Across the software and consulting lifecycle, firms report 20–40 percent reductions in manual workload and significant quality improvements.

Yet the greater transformation lies in how organizations are structured. Hierarchies are flattening. Decision-making is being delegated to intelligent systems that can manage complex workflows in real time. The “pyramid” model of consulting and IT delivery is being replaced by agile, AI-orchestrated networks of human and machine expertise.

Human talent remains critical — but its focus shifts toward what AI cannot yet replicate: creative problem solving, relationship management, and ethical judgment. The workforce of the future will be smaller, more interdisciplinary, and more strategically deployed.

How leading players are responding

Industry leaders are already investing heavily in this transition. CGI’s ai360 program has expanded AI-based client projects by 140 percent in a year. Accenture has pledged USD 3 billion to AI transformation and expects half its revenue to come from AI-related work by 2028. Capgemini’s partnership with Microsoft to build the Quercus GenAI platform illustrates how consultancies and hyperscalers are merging expertise to accelerate industrial-scale AI deployment.

These moves mark the start of a new competitive era. AI investment is no longer optional — it is the foundation of future relevance. Firms that move early can shape industry standards; those that hesitate will find their legacy models increasingly unprofitable.

From agents to enterprise impace - early days of AI scaling

Across the digital services landscape, the trajectory of AI adoption shows strong momentum — yet a clear gap remains between experimentation and enterprise-level impact. Several patterns have become consistent over the past years:

1. AI adoption is now ubiquitous, but scaling remains the exception.

Most organizations have introduced AI into at least one business function, and many have achieved promising results in isolated domains. Yet broad, cross-functional scaling is still rare. AI often sits at the edges of operations rather than reshaping the enterprise core.

2. AI agents are gaining traction, though deployments are still narrow.

Agentic systems are being tested widely — in IT operations, support functions, analytics workflows, and software delivery. However, these deployments typically remain limited to single use cases. The transition from localized pilots to integrated, multi-process agentic architectures has only begun.

3. Value creation is strong at the use-case level, but enterprise impact is modest.

Where AI is applied with focus, organizations achieve meaningful gains: accelerated execution, cost-efficient delivery, and higher quality outputs. Yet many still struggle to convert these gains into material improvements in enterprise performance, signaling a need for more systemic integration.

4. Leading performers approach AI as a redesign challenge, not a tooling exercise.

A defining characteristic of early leaders is their willingness to re-architect workflows, clarify ownership, and embed AI into decision-making processes. Technology alone does not differentiate them; operating-model transformation does.

5. Organizational and process readiness are more decisive than technical capability.

The primary barriers to scaling are rarely model access or algorithmic constraints. Instead, challenges typically lie in fragmented data foundations, legacy workflows, unclear governance, and insufficient workforce readiness for human-AI teaming.

6. Domain-specific data ecosystems are emerging as the strongest source of advantage.

Differentiation increasingly depends on curating, protecting, and activating proprietary, industry-relevant datasets. Firms that control high-quality domain data are better positioned to deliver contextualized solutions — the step in the value chain least exposed to commoditization.

7. Digital service firms and software providers are advancing fastest — each from a different starting point.

IT services organizations have moved quickly due to early establishment of AI labs and strong incentives to improve operational efficiency. Software developers, by contrast, are unlocking scale by leveraging extensive proprietary datasets embedded in their products. Together, they are setting the pace for AI industrialization in the services economy.

Strategic recommendations

For leaders in consulting and digital services, the message is clear: adaptation must be structural, not superficial.

Four imperatives stand out.

First, redefine the business model.

Transition from capacity-based billing to value- and outcome-based pricing. As AI compresses delivery timelines and reduces manual input, traditional hourly billing will face margin compression. Develop new commercial frameworks that price intelligence and outcomes rather than effort, establishing clear metrics for AI-enabled value creation—from speed-to-market improvements to quality enhancements. Leading firms are pioneering hybrid models combining subscription-based platform access with success-based fees tied to specific business outcomes, capturing the full economic upside of intelligence-scaled operations rather than capping revenue at labor capacity.

Second, build proprietary data ecosystems.

Curate, protect, and leverage domain-specific data as the foundation for differentiation. As generic AI models become commoditized, the real competitive moat lies in owning exclusive, industry-specific datasets. Firms must evolve from "buyers" of off-the-shelf AI tools to "builders" of their own intelligence layers. Organizations with formal data governance demonstrate 35% higher ROI on data investments and achieve 4x faster speed-to-insights compared to those without.

When AI is combined with proprietary datasets and process redesign, organizations achieve cost reductions of up to 25%. This requires systematic investment in data infrastructure and treating proprietary data as a core strategic asset rather than an engagement byproduct.

Contextualization remains the least threatened step of the services value chain because it demands intimate industry understanding that only domain-specific data can provide. Firms with curated client-specific repositories can deploy AI agents that diagnose, predict, and recommend with precision generic models cannot match. In an era where generic intelligence is abundant but contextualized intelligence remains scarce, ownership of high-quality, industry-relevant data will determine who controls the next wave of AI-enabled services.

Third, redesign the operating model.

Automate systematically to fundamentally reconfigure workflows around AI-human collaboration. Treat intelligent systems as integral workforce components with clear accountability frameworks and governance mechanisms. Organizations report 20-40% reductions in manual workload as AI copilots handle documentation, testing, and quality assurance while human experts focus on architecture and judgment. This requires re-architecting end-to-end processes rather than simply deploying AI tools—clarifying ownership between human and machine capabilities and embedding AI into decision-making workflows. Create hybrid delivery models that orchestrate seamless collaboration, amplifying strategic judgment while automating execution at scale.

Fourth, rethink talent and culture.

Invest in AI literacy across all roles while restructuring workforce composition toward hybrid skill sets combining business design, technology fluency, and ethical judgment. Build continuous learning programs blending technical training with domain expertise, ensuring professionals can translate business context into AI-executable strategies. Foster a culture of experimentation and cross-functional collaboration, creating psychological safety for testing AI-enabled approaches. Focus human talent on creative problem solving, relationship management, and AI governance—the irreducible capabilities that define leadership in the intelligence-scaled era—as routine work diminishes and value shifts to orchestrating autonomous systems.

Looking ahead

The digital services industry stands at a defining inflection point. AI is not another technology wave — it is the foundation of a new industrial logic. It will amplify human creativity, accelerate delivery, and upend the relationship between scale and value.

The firms that succeed will not be those with the largest teams or the longest client lists, but those that learn to turn intelligence itself into an asset class. The age of intelligent services has begun — and in it, leadership will belong to those who can transform fastest, think boldly, and make machines an integral part of their strategic DNA.

"In an era where AI models are becoming commoditized, proprietary data ecosystems are the new competitive moat. The firms that will thrive aren't those deploying the most AI – they're those curating domain-specific datasets that encode deep industry knowledge."

Sign up for our newsletter

Further readings