![Global evolution of EAF and BOF crude steel production, 1990-2024 [bn Mt]](/content_assets/content_images/captions/24_2670_WEB_Steel-scrap-challenge_01_03_large_image.png)

![Evolution of EAF and BOF crude steel production in Europe, 1990-2024 [bn Mt]](/content_assets/content_images/captions/24_2670_WEB_Steel-scrap-challenge_03_03_large_image.png)

![Evolution of EAF and BOF crude steel production in US, 1990-2024 [bn Mt]](/content_assets/content_images/captions/24_2670_WEB_Steel-scrap-challenge_02_03_large_image.png)

![Evolution of EAF and BOF crude steel production in China, 1990-2024 [bn Mt]](/content_assets/content_images/captions/24_2670_WEB_Steel-scrap-challenge_04_03_large_image.png)

How steel players can harness AI to maximize outputs, improve efficiencies and increase competitiveness.

The growing battle for scrap steel in green steel production

Building resilience in your steel supply chain

As the steel industry races toward a more sustainable future, a critical challenge is emerging that may determine which companies thrive and which struggle in the decades ahead. While hydrogen technology and carbon capture dominate headlines, another critical issue demands immediate attention: securing access to high-quality steel scrap in an increasingly competitive market.

"Developing a comprehensive approach to scrap management is no longer optional – it's an imperative for long-term competitiveness."

The silent revolution: EAF's unstoppable rise

The shift toward greener technologies, such as Electric Arc Furnace (EAF) steelmaking, represents one of the industry's most profound transformations. In Europe alone, EAF production has grown from approximately 30% of total steel output in 1990 to around 45% in 2024. This transition isn't slowing – on the contrary, the majority of planned capacity additions in both Europe and North America are dedicated to EAF technology.

This revolution isn't happening by chance. Regulatory pressures (particularly carbon taxes in Europe), lower emissions, and economic advantages are driving steelmakers away from traditional blast furnace routes. Recent data reveals that in the EU-27, the growth rate of recycled steel consumption outpaced total steel production by a remarkable 10 percentage points – clear evidence of accelerating change.

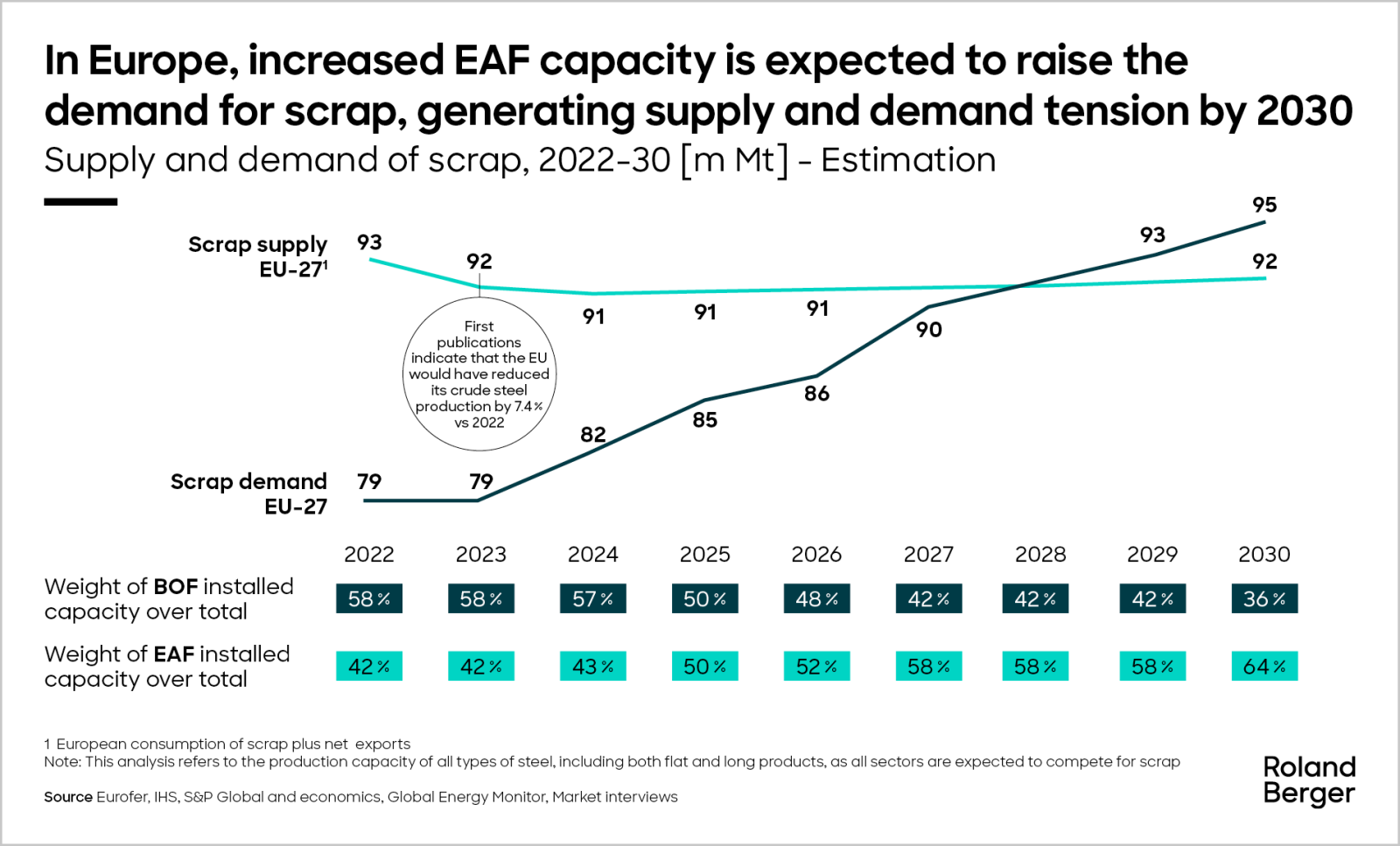

The approaching supply crisis: A mathematical certainty

As EAF production grows, so does the demand for its primary input: high-quality steel scrap . Yet the industry faces a sobering reality – scrap availability is growing more slowly than overall steel demand, creating a widening gap that represents both risk and opportunity.

This constraint is unavoidable due to fundamental market dynamics:

- Fixed supply sources: Scrap availability is determined by end-of-life steel products, not by market demand

- Long product lifecycles: The average lifespan of steel products is 40 years, creating a significant delay between production and recycling

- Diminishing returns: Collection rates are already high in developed markets, limiting potential supply increases

- Accelerating demand: Steel demand has been growing 0.4% faster annually than scrap availability since 1990

Industry projections indicate that by 2030, scrap demand in Europe will exceed supply – transforming the region from a net exporter to a net importer of approximately 3 million tons. This impending reality will reshape competitive dynamics across the industry.

"Successful implementation of a scrap management strategy requires a deep understanding of regional market dynamics, technological capabilities, and strategic options ranging from greenfield investments to acquisitions."

Quality: The hidden dimension of the challenge

Beyond raw tonnage, the quality dimension of scrap presents an equally critical challenge. Current sorting infrastructure and practices are inadequate to meet the needs of sophisticated EAF operations targeting high-end applications.

Steelmakers require highly sorted scrap with precisely controlled chemical compositions to produce advanced grades. The widespread practice of commingled collection results in downcycling, where the lowest alloy grades in mixed scrap define the potential applications of the recycled material. As a result, yield is highly dependent on scrap quality and scrap traders and steelmakers are heavily investing in scrap sorting capabilities. This is also necessitated by the fact that Direct Reduced Iron (DRI) based steelmaking performs worse than steel produced with a higher scrap ratio in terms of OPEX per ton. This quality gap represents another dimension where strategic foresight will separate industry leaders from followers.

First-movers are already securing their position

Forward-thinking steel companies recognize these trends and are taking decisive action. We've witnessed a wave of strategic acquisitions as steelmakers vertically integrate into scrap management:

- In North America: Cleveland Cliffs acquired Ferrous Processing and Trading for $775 million; Steel Dynamics secured Mexican processor Roca Acero; BlueScope doubled its processing capacity

- In Europe: ArcelorMittal acquired Scottish recycler John Lawrie Metals, German facilities from ALBA, Dutch recycler Riwald, and Polish processor Zlomex; Salzgitter purchased recycler Must Metalle Container Recycling

These acquisitions reflect a strategic recognition that future competitive advantage will increasingly depend on securing reliable access to high-quality scrap at predictable costs.

From risk to resilience: Creating a strategic advantage

For steel executives navigating this rapidly evolving landscape, developing a comprehensive approach to scrap management is no longer optional – it's an imperative for long-term competitiveness.

The companies that will lead tomorrow's steel industry are developing strategies today across three dimensions:

- Supply chain security: Establishing diverse, reliable sources of scrap through ownership, long-term contracts, or strategic partnerships

- Quality optimization: Investing in advanced sorting and processing capabilities to secure higher-quality input materials

- Cost predictability: Developing financial strategies to mitigate increasing price volatility in scrap markets

Successful implementation requires a deep understanding of regional market dynamics, technological capabilities, and strategic options ranging from greenfield investments to acquisitions.

The time for action is now

The transition to EAF technology and the resulting competition for scrap resources represents both risk and opportunity for steel producers worldwide. Companies that proactively secure their scrap supply chains now will gain significant advantages in cost structure, product capabilities, and sustainability credentials.

The window for action is open, but it won't remain so indefinitely. As more companies recognize this strategic imperative, acquisition targets will become scarcer and more expensive.

For steel industry leaders, the question isn't whether to develop a comprehensive scrap strategy – it's how quickly they can implement one that will secure their position in the industry's green future.

Roland Berger's Materials & Process Industries practice works with leading steel companies worldwide to develop comprehensive strategies for securing scrap supply, evaluating acquisition targets, and optimizing supply chain resilience. Our team combines deep industry expertise with strategic vision to help clients transform challenges into competitive advantages.

Digvijay Gupta also contributed to this article.

Sign up for our newsletter

Further readings