Closing the loop: Collection, sorting, and consumer behavior

Downstream, consumer willingness to embrace circular packaging is evident across the region. However, to turn intent into action, governments and mass-market retailers must introduce systems and nudges that enable behavioral change. Where incentives such as cashback or loyalty rewards are meaningful, engagement rises. Uptake also grows when recycling is convenient, carries a sense of value, and taps into the 'cool factor'.

Awareness is essential, but it is not enough. Educational initiatives involving public campaigns and school curricula reaching thousands of students, have succeeded in raising knowledge and willingness to recycle, but also exposed an uncomfortable truth: without the necessary waste management infrastructure, individual willingness rarely translates into long-lasting behavioral change.

The cost of inaction - and the way forward

According to the Gulf Petrochemicals and Chemicals Association (GPCA), the plastics recycling market in the GCC could generate approximately 50,000 jobs and USD 6 billion annually across the value chain – covering collection fees, materials recovery facility (MRF) revenues, recyclate sales and local conversion margins – if recycling rates increase from 10% to 40%. This figure reflects only the plastics segment, which accounts for roughly 15-20% of all packaging materials, indicating that the broader circular packaging market holds even greater potential for economic growth and sustainability in the region.

The GCC has already shown that bold measures can deliver rapid results. Abu Dhabi's single-use plastic bag ban in 2022 is proof: within two years, 364 million bags were eliminated, saving 2,400 tonnes of plastic and cutting greenhouse gas emissions equivalent to 130,000 cars off the road. Similar bans on Styrofoam achieved a 97% compliance rate among retailers.

These examples underscore the power of decisive regulation.

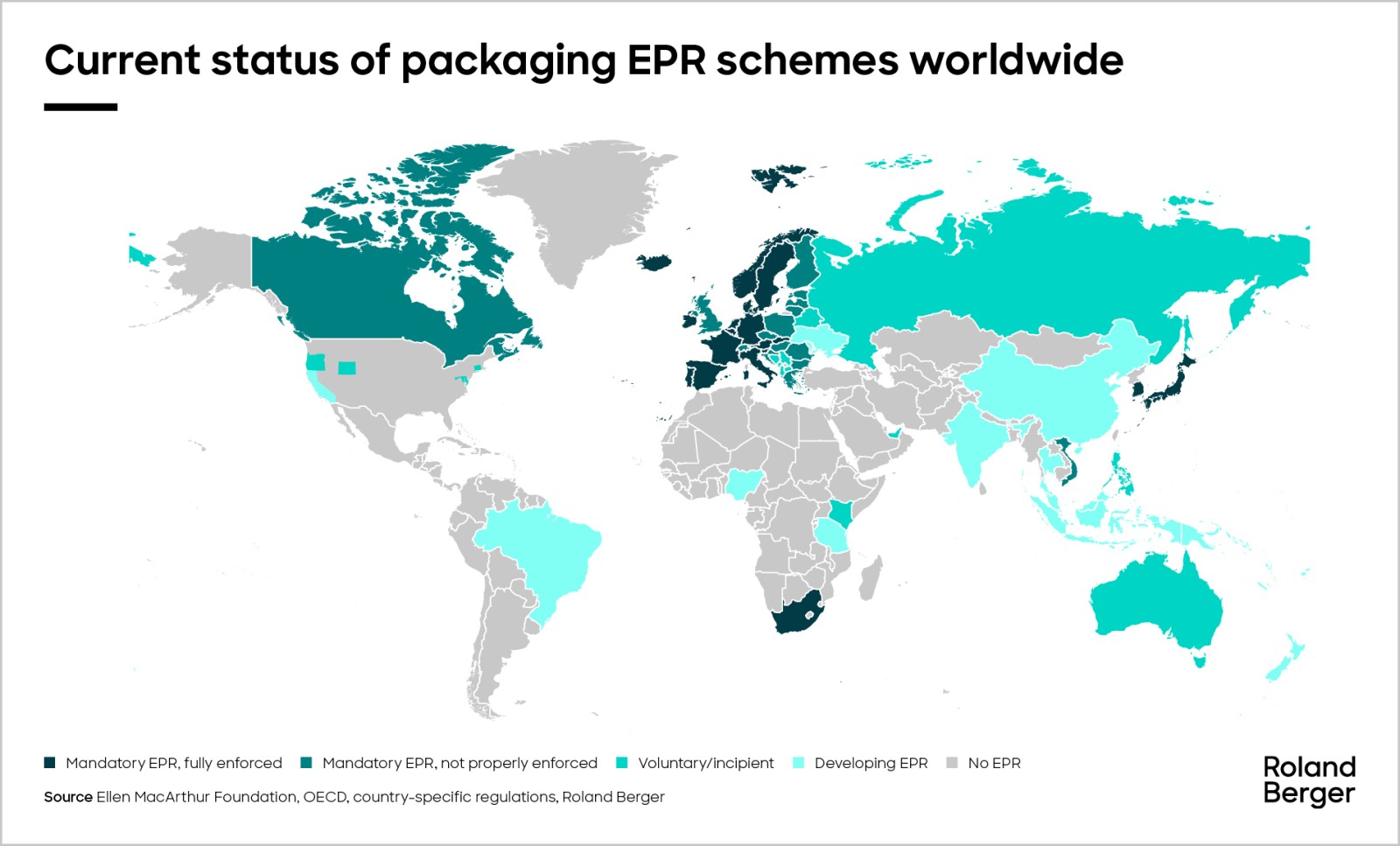

Creating economic pull is essential to scale circular packaging. EPR schemes with clear cost-sharing mechanisms and eco-modulated fees — where better-designed packs pay less — must be paired with recycled-content requirements for high-impact packaging formats, starting with PET bottles and HDPE containers. These measures will anchor demand for recycled materials and justify investments and upgrades to infrastructure.

Ambition must be matched by operational capacity. Investment is needed in integrated waste management and treatment systems that connect collection, sorting and reprocessing, with upgrades rolled out in step with regulatory milestones. Reducing contamination and improving capture rates through a well-enforced multi-bin system will ensure that more packaging waste is recycled locally, rather than exported.

Transparent data and regular reporting must be linked to real performance, not just promises, ensuring that policies remain adjusted to the evolving technology and market realities. Performance-based contracts with standardized reporting metrics on collection, contamination and recovery rates should become the norm. Dubai Municipality's digital waste tracking system offers a useful model, providing real-time data on collection and recovery to guide enforcement and investment decisions.

Download the full report for exclusive insights into the GCC circular packaging market, including the latest trends, regulations, and opportunities. See how leading brands are driving innovation and discover actionable strategies for advancing circularity across the region.

![{[downloads[language].preview]}](https://www.rolandberger.com/publications/publication_image/Roland_Berger_25_2483_CircularPackaging_Cover_download_preview.jpg)