Study

Venture Capital: fuelling innovation and economic growth

![{[downloads[language].preview]}](https://www.rolandberger.com/publications/publication_image/Roland_Berger_Treibstoff_Venture_Capital_Cover_EN_download_preview.jpg)

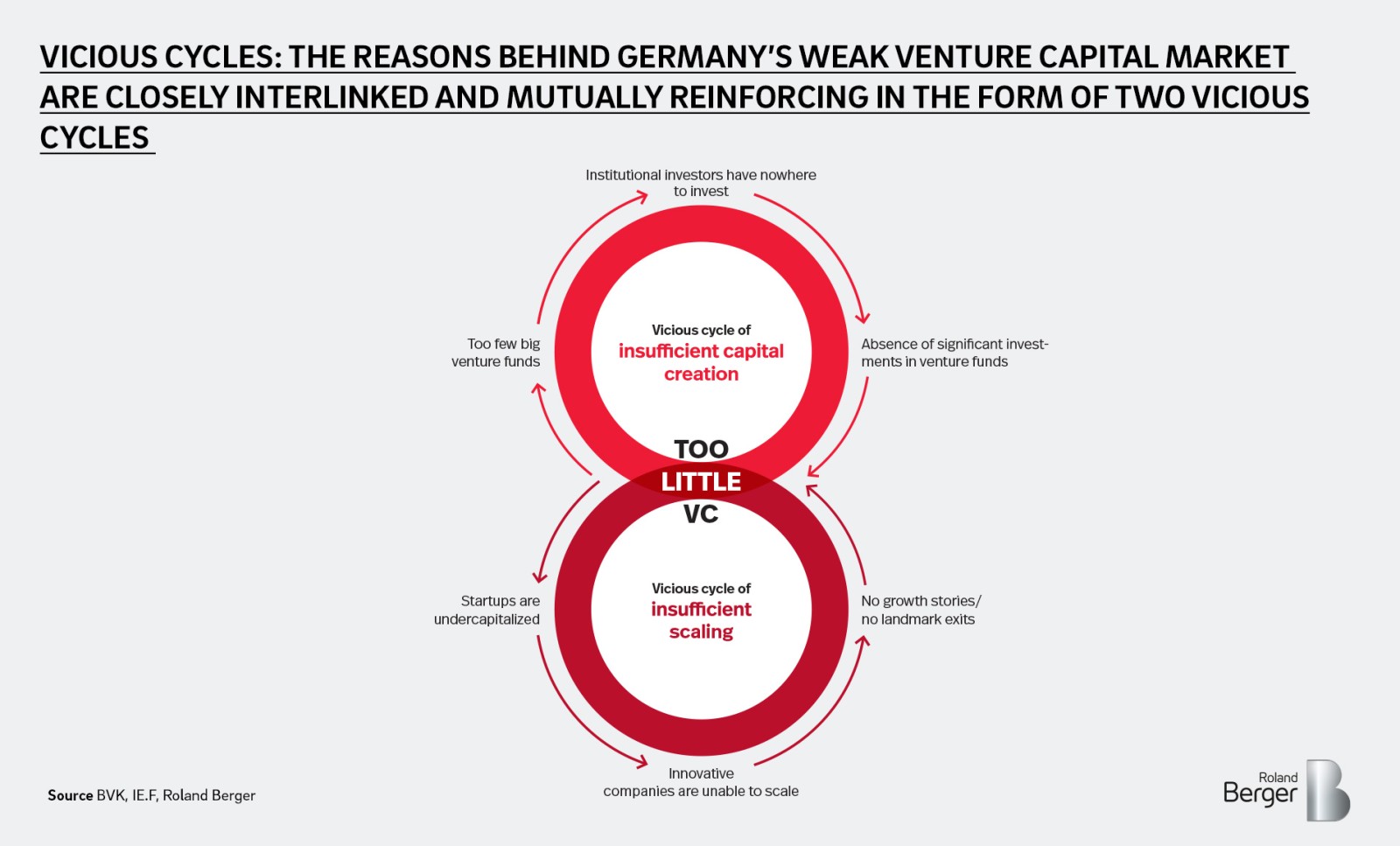

A lack of venture capital diminishes the German economy's power to innovate and hinders the growth of new companies. We outline six actions that Germany can take to mobilize more venture capital.

Published June 2018. Available in