A better future for the piggy bank

Conversion of savings to investments

"Converting part of the rising Belgian savings deposits into investments comes with a triple win, but realizing it remains a key challenge for banks"

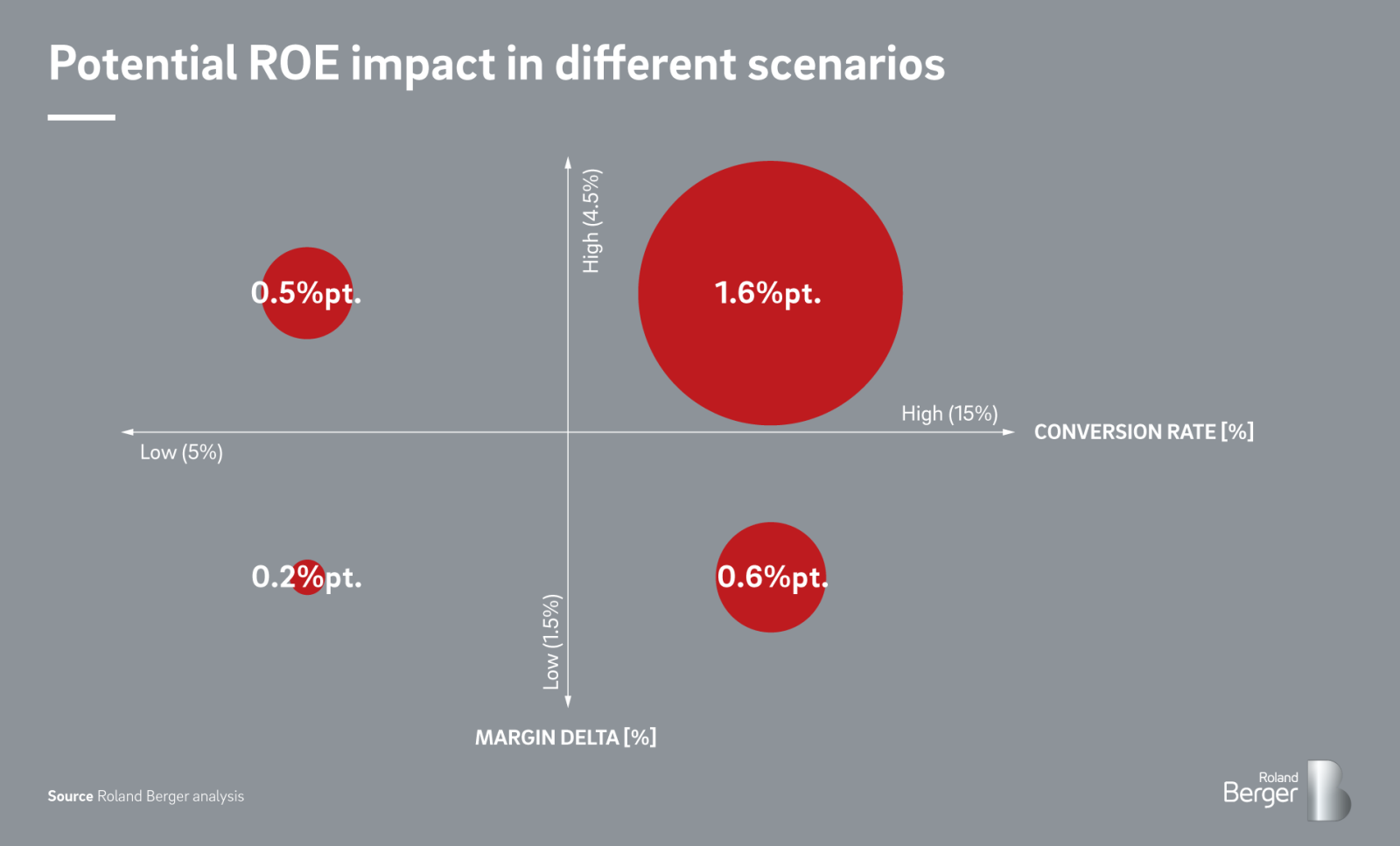

After a gradual decline in recent years, the share of income Belgian households save has been rapidly increasing in recent months and is expected to reach this year c. 20% in the wake of the Covid-19 crisis. An important share of the money saved ends up on traditional savings accounts despite the negative real return they offer to the bank customers. This is clearly a missed opportunity for both banks (as savings deposits are also for them lossmaking) and for the society (as the money on savings accounts could also play a role in e.g. the relaunch strategy). To successfully convert loss-making savings into revenue-generating financial investments, banks can help customers to clear a set of hurdles along the way that are currently preventing them to consider, discover or purchase financial investment products. Although there are clearly no quick fixes, we identified the levers banks and policymakers can use to help the Belgian households to make the switch. By successfully applying these levers, the conversion of savings to investments could increase revenues for Belgian banks by up to EUR 2 billion per year and ROE up to 1.6 percentage points.

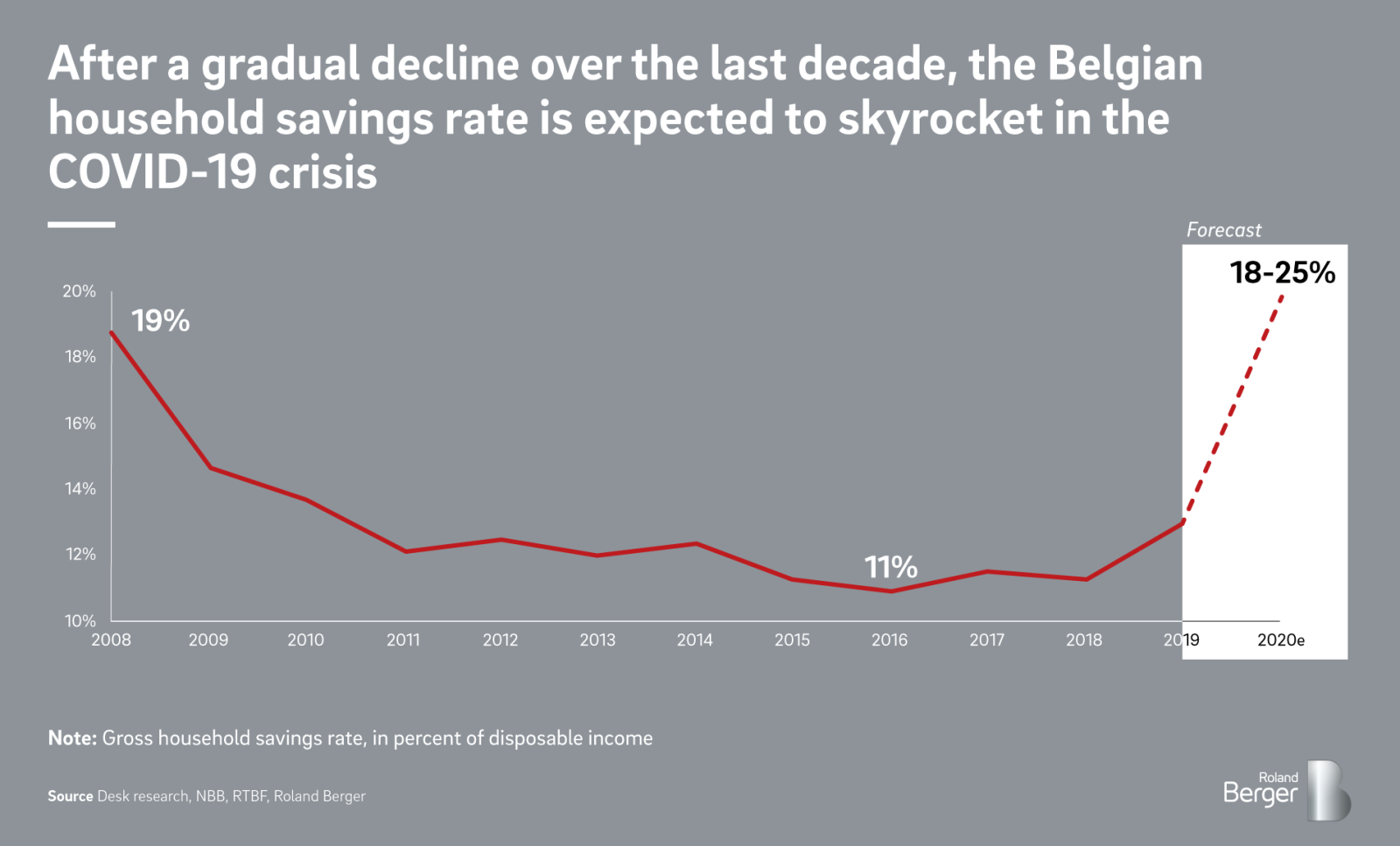

Since the financial crisis, the Belgian household savings rate (savings rate corresponds to the ratio of household income saved to household net disposable income in a given time period) gradually declined from almost 19% at the start of 2009 to less than 12% by early 2019.

After a period of gradual decline, the Belgian household savings rate is soaring and expected to reach approximately 20% in 2020 in the wake of the Covid-19 crisis

While there is no single, clear explanation for this decrease, several fundamental factors can be linked to it, including persistently high consumer confidence, an increased ratio of labor income/total income and an increase in loans linked to low interest rates.

However, in the wake of the Covid-19 crisis, the savings rate has been soaring since the announcement of the lockdown, during which Belgian households piled up 40% more savings than the same period last year, according to De Tijd (02/07/20) "Tegoeden op spaarboekjes stijgen het meest in tien jaar". As a result, the savings rate is now expected to outgrow the rates of 2009, and we expect it to reach 18-25% in 2020. The main reasons behind this are:

- Precautionary savings: households create financial buffers to protect themselves against an uncertain future (including higher risk of unemployment and higher future taxes linked to increased sovereign debt levels).

- Restricted lifestyle: national Covid-19 measures have largely restricted daily life and leisure activities (especially during the lockdown period) and hence, the possibility to spend money.

Over the last few months, we see that in many cases the money saved still ends up on a classic savings account.

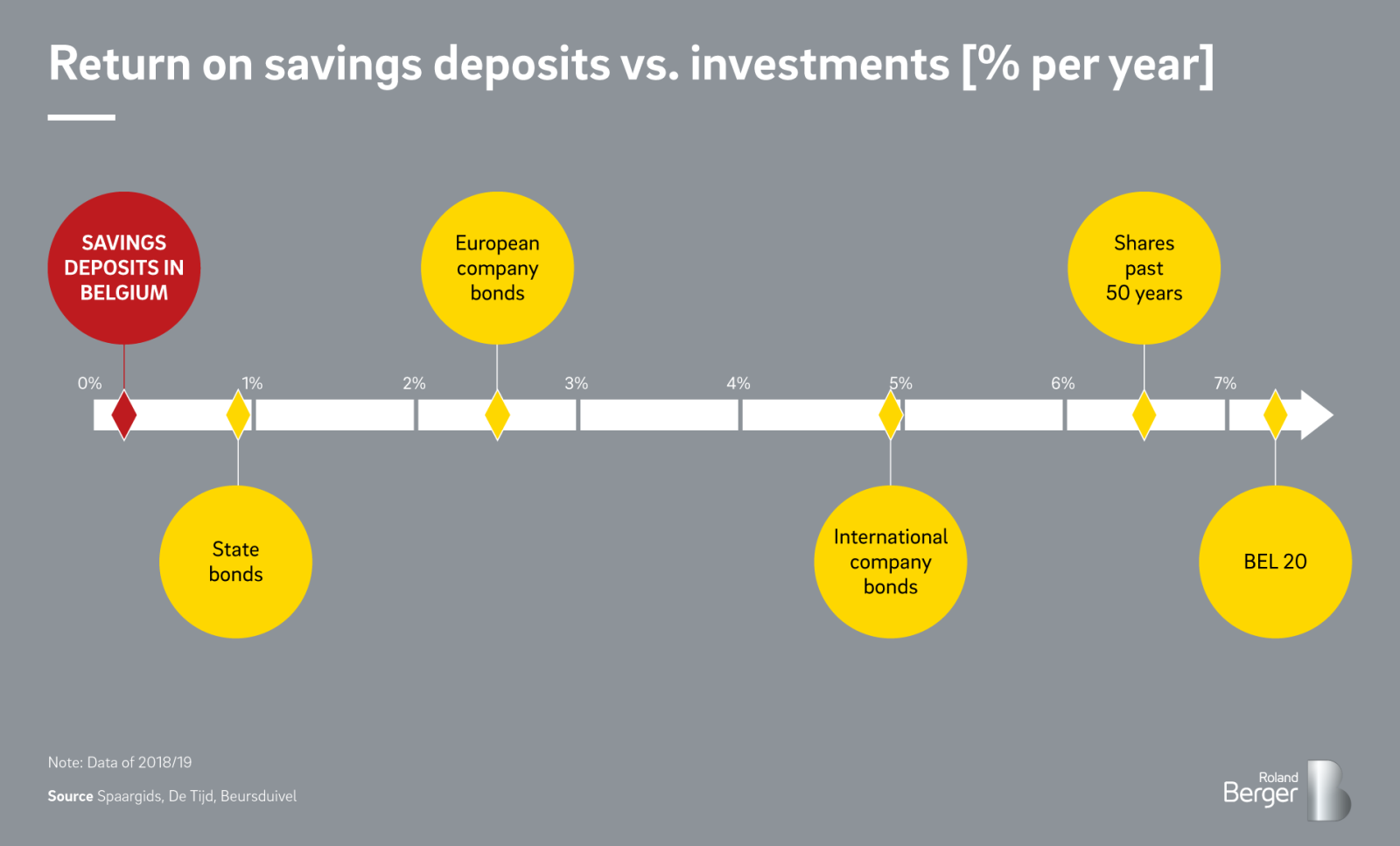

However, the shift to savings deposits is not an economically attractive one for the clients. From 2014 to 2019, the Belgian inflation rate increased from about 0.5% to 1.4%, while interest rates on savings deposits decreased and currently range from 0.11% (the legal minimum) to 0.6%. This implies that money in savings accounts is eroding in real terms, hence negatively affecting the purchasing power of Belgian households. Very clearly, a well-diversified portfolio of investment products demonstrated superior positive performance over the same period negatively affecting the purchasing power of Belgian households. Very clearly, a well-diversified portfolio of investment products demonstrated superior positive performance over the same period.

A classic alternative to an investment in financial assets remains for many Belgian households an investment in real estate. Even though it is less liquid, real estate investments entail a number of fiscal advantages and are sometimes considered less risky. Still, in many cases risks and costs remain non-transparent (which is less the case for an investment in financial assets, esp. since the arrival of MiFID).

The increase in savings deposits puts bank profitability under pressure as they turn from a "revenue model" to a "loss model"

Banks' traditional business model has long relied on the net interest margin (NIM), a measure of the difference between the interest income generated and the interest paid out to depositors. As interest rates have plummeted in Europe over the past decade, the banks' NIM has been under pressure.

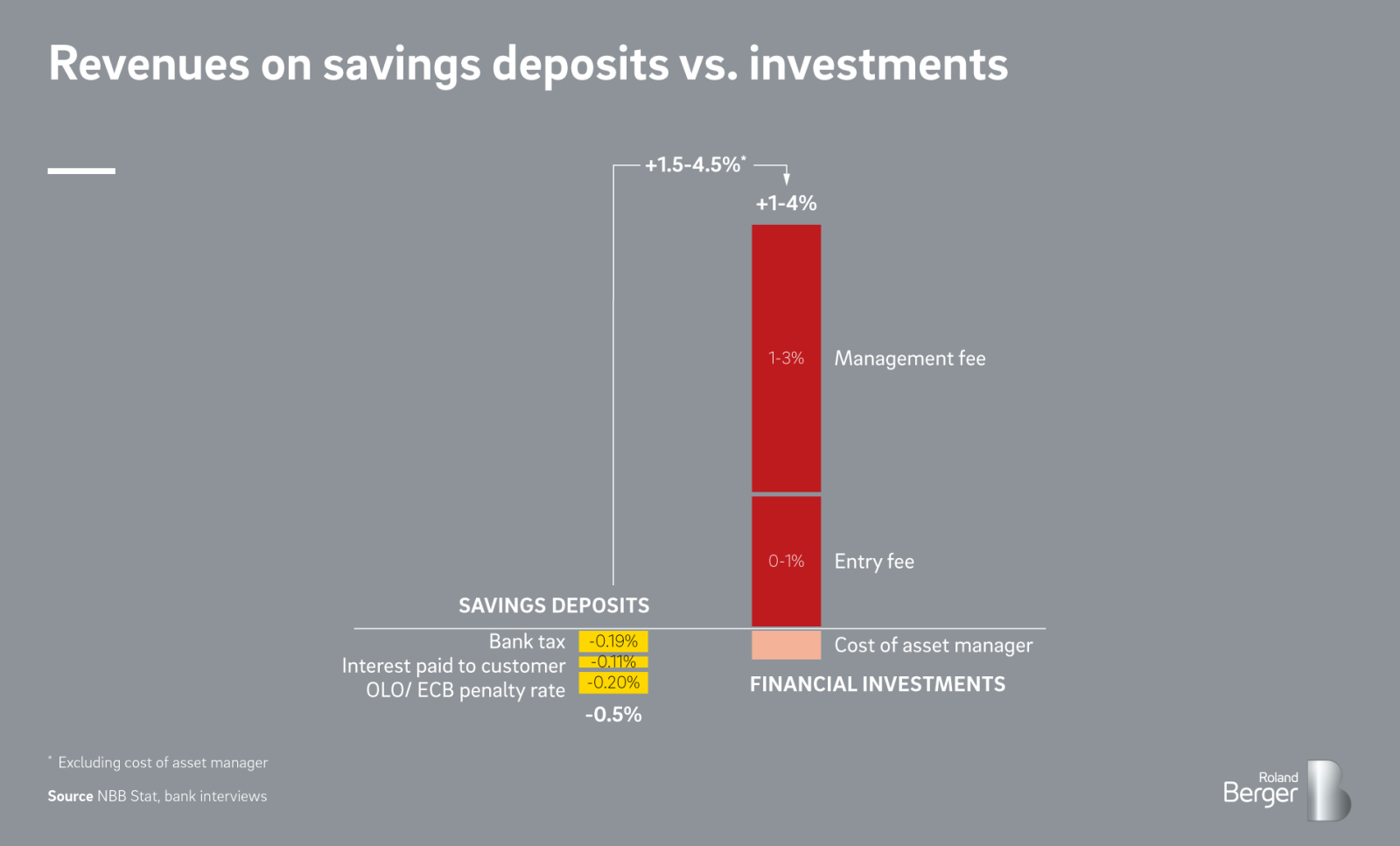

Belgian banks are no exception and see their profitability shrinking as a result. We estimate that fresh money flowing into savings deposits currently has a cost of c. -0.5% to Belgian banks (we disregard the reinvestment of deposits into loans as this gives rise to extra risk and costs such as personnel, processes, etc.).

_large_image.png)

In contrast to the negative profitability of savings deposits, retail customers' financial investments still offer interesting returns for banks. As the income on these products is particularly driven by commissions (management fees, entry fees, etc.), a bank's income on investments is not affected by falling interest rates. Furthermore, we saw that the profitability of investments was not fundamentally impacted by the obligation to credit kickbacks to customers' accounts. It is therefore not only important for the purchasing power of clients (provided that this concerns a well-diversified portfolio, cf. supra), but also in the interest of banks to convert part of the savings deposits on Belgian bank accounts into investments.

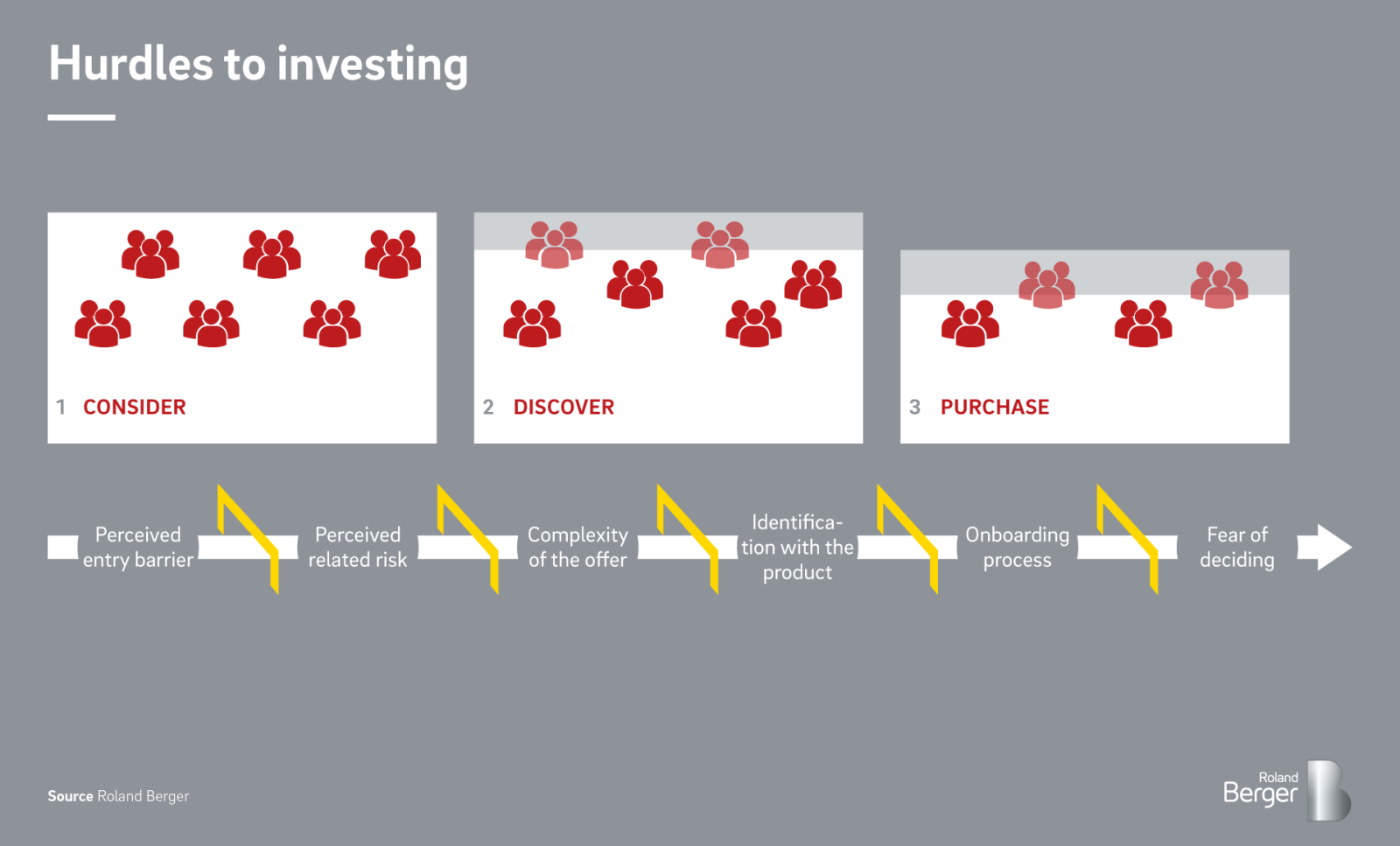

To successfully convert savings to investments, banks must help customers clear a set of hurdles along the way

Hurdles

As investments can offer higher financial returns than savings accounts for both banks and investors, it seems there must be some hurdles holding Belgians back from investing their money. To understand where these hurdles to investing come from, a deeper look at the client's thinking process is required. The journey between having the initial idea of investing and making the actual investment seems to involve three important stages. Within these stages, several hurdles can hold clients back from investing and their different nature reveals already that there is no quick fix to overcome these hurdles.

Consider ("Investing is not for me")

A first important hurdle keeping numerous clients away from investing are the perceived entry barriers. Many people still believe that they do not have enough funds to invest or that investing does not fit their knowledge or risk profile. Moreover, it seems that a large share of the Belgian population perceives investments as very risky. This perception has been spreading in recent times, as markets have become very volatile in the current crisis. Even though there are several risks inherent to investing, the perceived risks often do not match reality and can be managed.

Discover ("I do not know what to invest in")

Once a client believes investing could be of interest, many still do not know what investment products exist and where to start with their research. This is partially due to the complexity of bank offerings. When a potential investor has been able to identify the options available, they will research the pros and cons of the different options to decide which one fits them best. This has proven to be a painful process for many Belgian bank clients. In addition, recent research has shown that the financial literacy of Belgians is below the European average, which keeps a large number of potential investors from actually putting their money to work. But even when clients have gained an understanding of a specific product, many still struggle to identify with the product offer. Investment products often have obscure names and rarely succeed in genuinely attracting customers.

Purchase ("I do not know how to invest")

The final stage consists in converting clients that are convinced a certain investment product is of interest into actual purchasers of the product. Even at this stage, some clients are still lost in the process. The complex and cumbersome process of onboarding clients is one of the reasons for this. Given the way some banks deal with the many regulatory (e.g. MiFID II, KYC) and contractual obligations, the onboarding of investors can be a very time-consuming process. In addition, some investors drop out in the end because of the fear of deciding: Not making a decision is ultimately easier than having to decide, and second thoughts often only pop up at the moment the actual decision needs to be made.

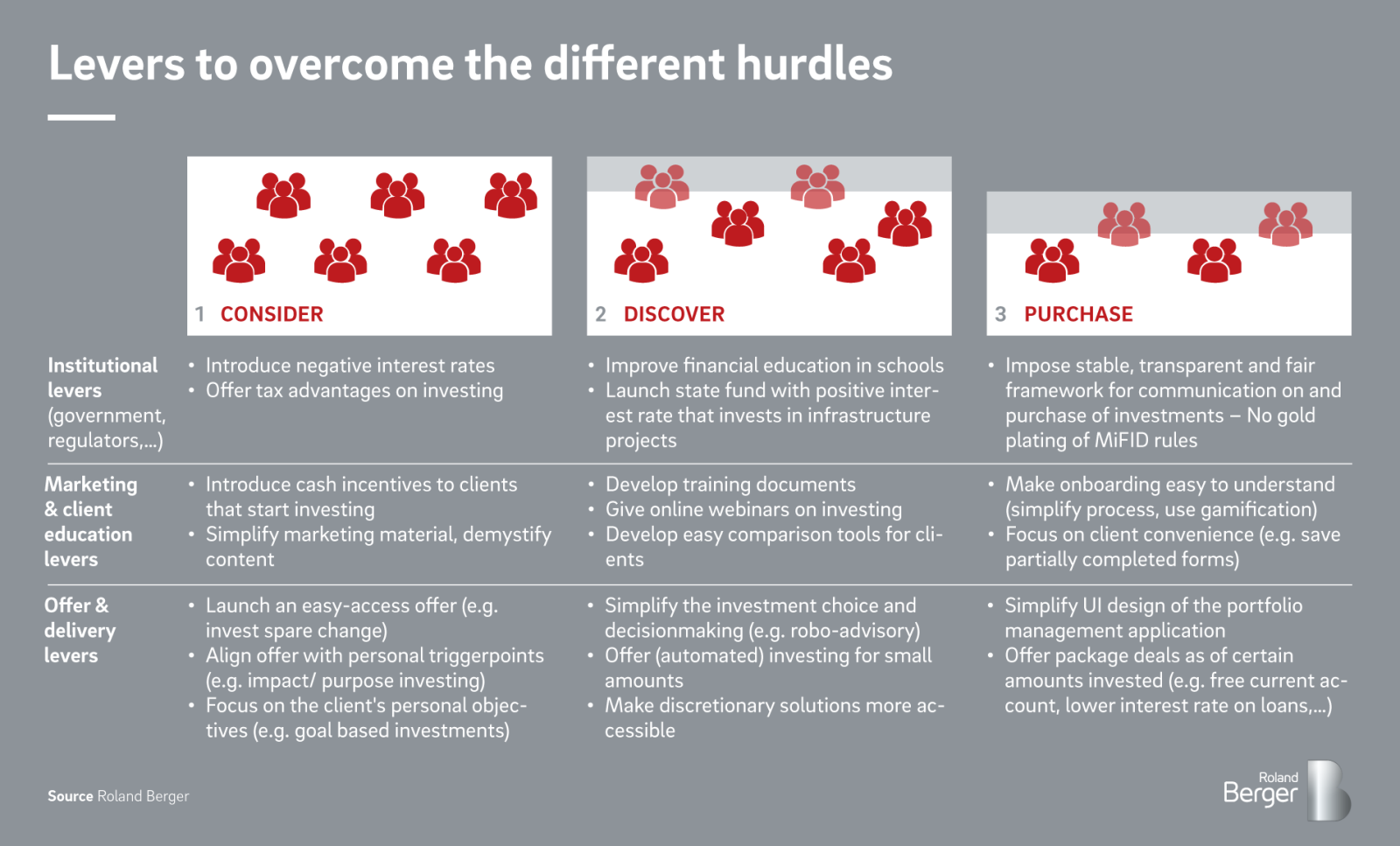

Solutions

Types of levers

Banks that want to keep potential investors on board for the whole journey will have to provide solutions to overcome the different hurdles. The hurdles to focus on will differ from bank to bank. Yet a certain degree of maturity on each one of them will be needed to actually convert clients' savings deposits to financial investments. To help achieve this, Roland Berger has identified a set of potential levers for each of the hurdles along three different dimensions.

Case studies

Consider – Offer & delivery: Spare change investment solutions

Smart spare change investment solutions help consumers put spare money aside for investment purposes. The consumers' everyday spending is rounded up to the nearest euro and at a certain point (e.g. when a set target amount is reached) the balance is automatically put into an investment plan. Such smart investment solutions help consumers overcome the "Consider" hurdles. Even though many people feel they do not have enough money to invest, this technology allows them to do so in an effortless way. To promote the investment behavior of its clients, KBC, for instance, launched such a spare change investment solution within its mobile banking app in 2018.

Discover – Offer & delivery: Robot advisory solutions

Robo-advisory is a digitalized service whereby an online platform provides automated investment advice to clients, based on mathematical rules or algorithms linked to the client's risk profile, with little or no physical human interaction. Through their user friendliness and investment portfolio customization algorithms, robo-advisors decomplexify the product for customers and simplify the investment decision-making. At the same time, the digital solution allows banks to avoid the need for costly human advisors and make the service available to a mass consumer base. Lastly, a more digitalized and less costly investment offering should also increasingly appeal to the young adult market. With increased technology maturity and the recognition of its potential, robo-advisory has been gaining popularity in asset management globally over recent years.

To promote the conversion of their customers' savings into investments, several Belgian retail banks have recently integrated robo-advisory into their commercial investment offering. KBC and BNP Paribas Fortis launched their smart advisory platforms Matti (developed by KBC group's subsidiary Bolero) and Lucy, respectively, both in 2020 with the goal to activate their customers' investment behavior. BNP Paribas Fortis, for instance, offers its smart investment advisor Lucy from an investment amount of just EUR 1,000, significantly more accessible than its "human" tailored investment advisory services.

When done successfully, conversion of savings to investments could increase revenues for Belgian banks by up to EUR 2 billion per year and ROE up to 1.6 percentage points

As highlighted earlier, Belgian banks are currently losing money on savings deposits, and with around EUR 300 billion parked in Belgian savings accounts (c. EUR 280 billion at the beginning of 2020 and at least EUR 20 billion expected to be added because of the COVID-19 crisis), even a limited negative return can have a significant impact on overall bank profitability. Investments in turn yield positive returns for banks thanks to the commissions and other entry/management fees.

A detailed analysis shows that the difference in revenue contribution between savings deposits and financial investments can vary greatly depending on specific circumstances. However, with a range of 1.5-4.5% on average (excluding cost of asset management), the difference is always significant.

For Belgian banks the potential upside is very significant: If banks manage to convert part of their savings deposits into investments this would generate additional revenues of up to EUR 2 billion (depending on the success of the conversion-effort and the margin on the solutions used). At a time when profits of Belgian banks are under pressure, this could generate a positive impact on ROE of up to 1.6% points (assuming a 50% profit contribution of the fees paid on financial investment products).

In addition to improving overall profitability, converting savings to investments may also be an opportunity for banks to improve their risk profile. In contrast to savings deposits, which are very liquid, investment products tend to be fixed on the banks' accounts for a longer period of time.

While the upside is there for all Belgian banks, the magnitude of it and challenges and opportunities to be faced along the way will be different. We see for example that smaller retail banks (the traditional "savings banks") face a relatively bigger portfolio of savings deposits and rely on a client base that is typically less familiar with financial investments. Large retail banks, on the other hand, have less strong relationships with their clients, and the relationship they do have with them is mainly through digital channels. This means that there will be no onesize-fits-all approach, but rather a customized conversion strategy that individual banks need to develop taking into account the different customer segment characteristics, distribution network opportunities and digital tools at their disposal.

_person_320.png?v=1776270)