Roland Berger advises companies on industrial goods and services, combining outstanding industry expertise and excellent technical know-how.

Autonomous and uncrewed vessels: A new wave of opportunity

How to navigate and exploit the latest high-growth megatrend in shipbuilding

Autonomous vessels promise numerous advantages over conventional ships, presenting clear opportunities for players in the maritime ecosystem. But market entrants also face several challenges, from unproven technologies to undecided regulations. In this article, we assess the trends, use cases and risks in the industry to help companies embark on their journey in this exciting new direction of shipbuilding. They need to move fast.

"With the IMO currently defining regulations for autonomous ships, players should act now and go through their innovation roadmaps to check if they are on the right track. We can help."

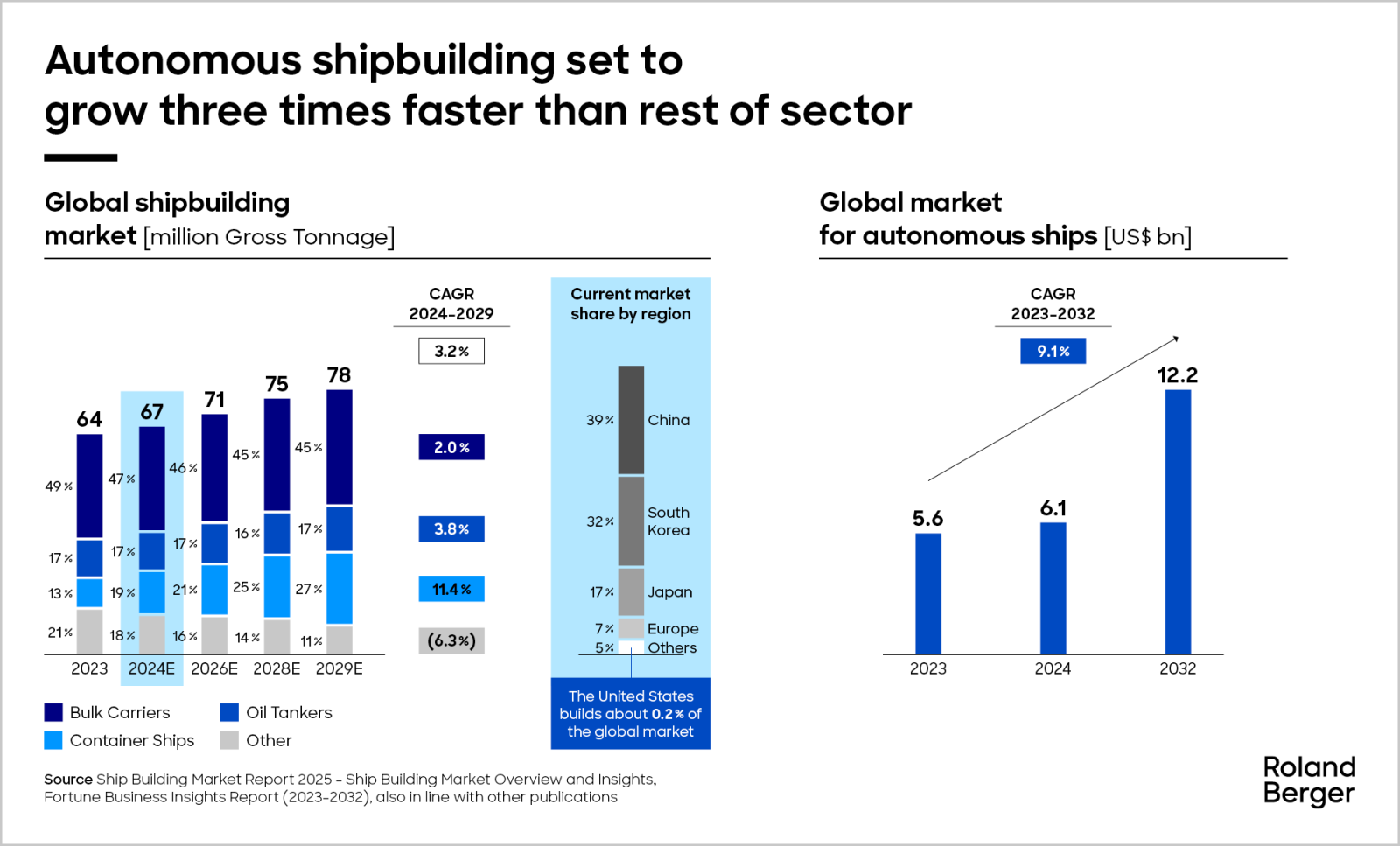

The case for autonomous and uncrewed ships seems obvious. Cheaper building and operating costs, increased efficiencies, reduced cargo delivery times, fewer accidents and lower emissions are just a few of the potential advantages. For these reasons, autonomous vessels are now at the forefront of innovation in the maritime industry, in both the military and commercial sectors. Indeed, the global market for autonomous ships is set to grow by 9.1% between 2023 and 2032 compared to 3,2% for the overall market.

However, it is not all plain sailing. While autonomous maritime technologies are advancing quickly, they remain unproven. Investing in them is therefore a risk, as is cybersecurity. In addition, the regulatory environment is a work in progress. The International Maritime Organization (IMO) is still in the process of defining regulations for autonomous ships (focus on commercial), and once they are implemented, the rules for uncrewed and fully autonomous vessels (levels three and four) are likely to cause significant disruption.

With these factors in mind, this article aims to outline the key trends and drivers in the industry, as well as use cases and attractive segments. It also highlights how industry players – from traditional suppliers to AI start-ups – can chart a path through the risks and opportunities, and determine if they are on the right track to reap the rewards.

Trends and drivers

Several market trends are impacting growth in the global commercial shipbuilding sector. On the positive side, more than 50% of the world fleet was at least 15 years old in 2023, pushing demand for modern, regulation-compliant replacements. In addition, advanced technologies such as AI and automation are increasingly available, with hybrid or electric propulsion as well as smart navigation becoming industry standards.

Deglobalization and more localized supply chains are having a more mixed effect. While they are likely to create strong demand for smaller, regional vessels, increasingly protectionist measures will probably lead to a downturn in long-distance shipping. More negatively, continued labor shortages and higher material costs are putting pressure on shipbuilders’ margins. Overall, however, growth projections are positive.

What specifically is driving growth in the autonomous industry? Regulations, such as stricter emissions rules and the upcoming IMO framework for autonomous vessels, are a factor, as are national policy initiatives like the SHIPS for America Act, which aims to revitalize the US shipbuilding industry. New technologies, from AI to communications systems that enable remote monitoring, are also driving demand, while the cost and operational efficiencies speak for themselves.

Use cases

The result is a growing spectrum of use cases across the autonomous vessel value chain. Promising examples include:

- Vessels that can monitor, maintain and service offshore equipment, such as wind turbines and oil rigs

- Passenger and cargo ferries that operate on short, repetitive routes to minimize the chance of accidents and reduce liability (for example, the electrically powered, IMO level four Yara Birkeland cargo ship)

- Emergency and search & rescue vessels that operate near high-traffic areas and are available for quick deployment

- Equipment to monitor high value assets such as ports, marinas, energy infrastructure and data centers

- Fast, high-endurance naval vessels that can detect/suppress threats to ports or other vessels, possibly as part of hybrid fleets (for example, the US Navy’s Sea Hunter and Singapore’s maritime security unmanned surface vessels).

Such use cases present clear opportunities and risks for players in maritime industries:

"Autonomous maritime technologies are advancing quickly, but they remain unproven. Market entrants need to be aware of the risk before they can exploit the opportunities."

Opportunities

Electric propulsion systems: Electric vessels offer improved maneuverability and a smaller environmental footprint.

Autonomous port infrastructure: After autonomizing ships the next step will be to autonomize harbor equipment, such as cranes and battery chargers.

Connectivity, sensors and AI: All will be in demand to operate autonomous vessels and ports.

Remote service and configuration of vital systems: Players that can provide propulsion or other key systems can capitalize on the autonomy trend.

Partnerships between hardware and software companies: Shipbuilders will need to secure software expertise.

Risks

Missing connectivity standards: Software that is incompatible with vessel or port hardware, and vice versa, will not be competitive.

Inflexible propulsion systems: Existing producers must ensure they can adapt their propulsion systems (for example, away from diesel) and ensure connectivity.

Failure to update shipyard infrastructure: Autonomous ships require a much higher focus on software, and a change in legacy shipbuilding mindset.

Technician-focused service models: Autonomous ships require less servicing and will become increasingly less reliant on human technicians.

Non-standardized regulations: Regional variations mean there will be different communication, navigation and degree of autonomy requirements in different places, making flexible products essential.

Time to act

How can players in the maritime ecosystem best navigate the opportunities and risks? With the IMO still defining regulations, now is the time to ready your ship. For example, how well-suited is your product portfolio to the autonomous ships market? Does your business model need to be adapted or value chain expanded? And what is the target state of the company? Are you ready for transformation?

Roland Berger is well-placed to support players on their journey into the autonomous shipbuilding market. From dedicated market studies, readiness assessments to preparing innovation roadmaps and developing new products, we have years of experience delivering tangible results in the shipbuilding and autonomy sectorsin all regions. Furthermore we know what it takes to transform companies and get ready for the next level We plan to publish more details on both later this year. In the meantime, feel free to contact one of our experts for more information.

Sign up for our newsletter

Further readings