These are challenging times for capital goods companies in the DACH region. With order backlogs declining significantly in recent months, they face a variety of challenges, ranging from geopolitical tensions and economic uncertainties to climate change and industry transformations. Signs of downturn vary significantly across industries and regions, meaning companies must collate a thorough understanding of their individual business units and the contextual factors influencing each one. In response to these challenges, Roland Berger recommends a proactive and scenario-based strategy. This involves starting with immediate "no-regret" initiatives to address pressing issues, followed by structural adjustments and longer-term growth initiatives to secure future success.

DACH capital goods firms face uncertainty as machine export's early 2023 promise dims due to dwindling orders.

Capital goods companies in the DACH region are at a critical juncture amid growing concerns triggered by an uncertain economic outlook. This is despite a glimmer of hope in the first half of 2023, when machine exports appeared promising. However, this trend was largely thanks to substantial order backlogs built up during periods of high demand. These backlogs have gradually reduced in recent months, causing optimism to wane as new orders fail to adequately replenish them.

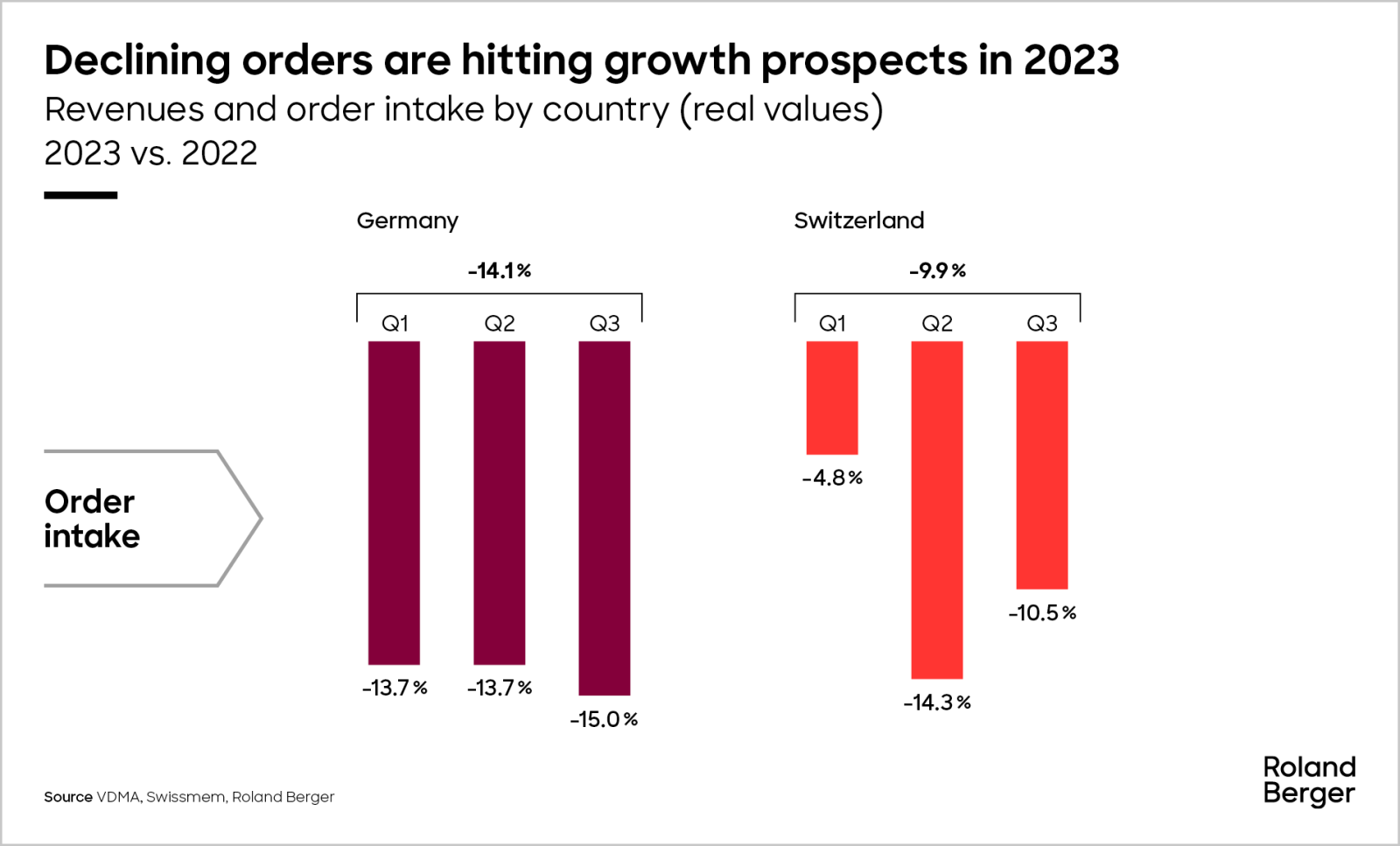

Notably, Swissmem, the Swiss association for mechanical and electrical engineering industries, has highlighted a 9.9% decline in order intake for the first nine months in 2023 compared to the previous year. During the same period, sales remained at the same level as the previous year (-0.1%). Similarly, VDMA, Germany’s Engineering Federation, reports a significant decline in orders, with a 13% drop in September 2023 contributing to a 14% decrease for the first nine months of the year. These developments underscore the substantial challenges faced by the manufacturing sector in the DACH region.

Prominent industry leaders have sounded the alarm regarding the uncertain outlook. What stands out in the current situation is the unprecedented complexity confronting market participants. Geopolitical tensions, macroeconomic uncertainties, high interest rates, climate-related challenges, and industry-specific transformations such as hydrogen, electric vehicles, AI, and e-commerce are all unfolding simultaneously and often overlapping, potentially magnifying their impact.

"Seizing business opportunities around service and modernization have proved effective strategies, diversifying revenue streams and building customer loyalty."

We believe these companies are at a critical stage in terms of proactively addressing these challenges,

adopting a forward-looking approach,

and executing decisive short-term action. Some leading companies have already initiated workforce reductions in overheads and operations of between 5% and 15%, hoping to shed ballast accumulated over years of growth, increase their structural flexibility, and prepare for anticipated revenue declines.

While companies in the DACH region have long grappled with structural deficits, competitors in North America have been able to adapt to cost challenges more swiftly during a downturn. They haven’t just done this by reducing indirect costs but also by shutting down plants, offshoring the value chain, and outsourcing to suppliers, among other methods. Meanwhile, Chinese competitors are keen to capitalize on the current situation and further establish their presence in the global landscape. This started early in areas like solar panel production, before moving on to various machinery segments such as textiles, extrusion, and injection molding, as well as battery production, wind turbines, and now the

automotive industry,

to name just a few.

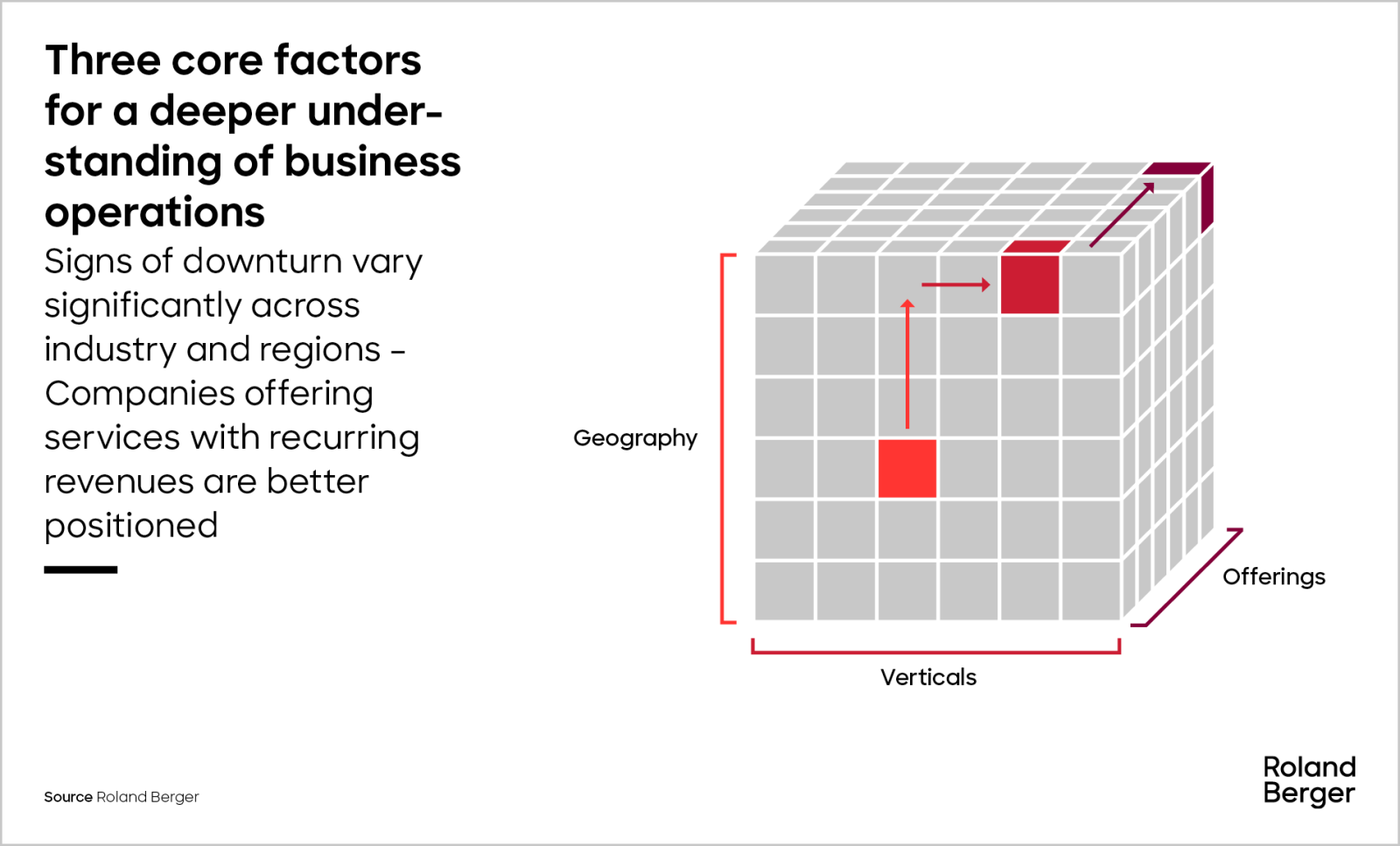

Signs of downturn vary; services with recurring revenues could be key

Capital goods companies in the DACH region face a complex array of circumstances, often marked by substantial differences across industries and regions. It is therefore essential for managers to gain a thorough understanding of their business units and the contextual factors influencing them. A matrix of three core dimensions can be instrumental in understanding the context in which a company operates: geography, verticals, and offering.

1. Geography: China at a crossroads

The economic slowdown is impacting major economies across the globe, albeit with varying degrees and underlying causes. China, the catalyst for economic growth during recent decades, faces challenges stemming from its restrictive Covid policies, with concerns emerging about the political climate and stability of foreign investments. The country’s domestic real estate sector, a cornerstone of economic growth, is facing serious challenges, mainly due to default risks coupled with lower demand, potentially further dampening economic prospects. China has announced several measures to bolster its economy, including an 11-point plan that targets domestic consumption.

Meanwhile, escalating tensions between China and the United States have culminated in mutual sanctions, with the future of China as a global economic driver increasingly challenged. In response to tariff threats and supply chain vulnerabilities, many global companies with primary markets in North America and the EU have begun shifting production to Southeast Asia or adopting a regionalized approach to their key markets – shifting to Mexico for the US, for instance, and Portugal or Eastern Europe for Europe.

However, Roland Berger believes these short-term instabilities should not obscure China’s promising medium- and long-term growth prospects. Investing in China remains both important and prudent during this transformative phase and still offers excellent growth potential, albeit more in the 5% CAGR dimension, rather than the double-digit growth of the past. In short:

China is normalizing as an economy.

In contrast, the US economy is facing unprecedented inflation levels while simultaneously dealing with weakened market demand. To counter these challenges, the government has introduced stringent monetary policies and enacted legislative measures under its Inflation Reduction Act aimed at boosting demand. Although there have been some recent positive developments in the job market and a modest uptick in retail sales, a cloud of uncertainty continues to loom, leading experts to express growing skepticism regarding a near-term economic rebound.

Amid these economic dynamics, it is important for DACH-based industrial firms to recognize the ongoing importance of the United States as a trade partner, particularly in sectors benefiting from government support like renewable energy and industrial automation, or from regionalization activities of companies with major market exposure to the US such as EMS or automotive.

The European Union, already grappling with a range of challenges, is currently experiencing a noticeable decline in momentum. A longstanding European economic powerhouse, Germany now faces major hurdles and is on the verge of relinquishing its global dominance in the automotive industry due to the transition to electric vehicles.

According to a

recent survey by Roland Berger,

which involved more than 650 restructuring experts across the DACH region, there is growing pessimism regarding the future, and concerns are mounting that Germany may lag behind on the international stage. Key worries revolve around skilled labor shortages, elevated inflation rates, and continuously escalating energy costs. A substantial 62% of the respondents in our survey anticipate a wave of restructuring in the months ahead. Certainly, industrial companies in the DACH region will be keen to see their home economy support global growth while simultaneously reducing their reliance on domestic markets.

"In current uncertainty, companies must act swiftly with 'no-regret' activities to address pressing issues."

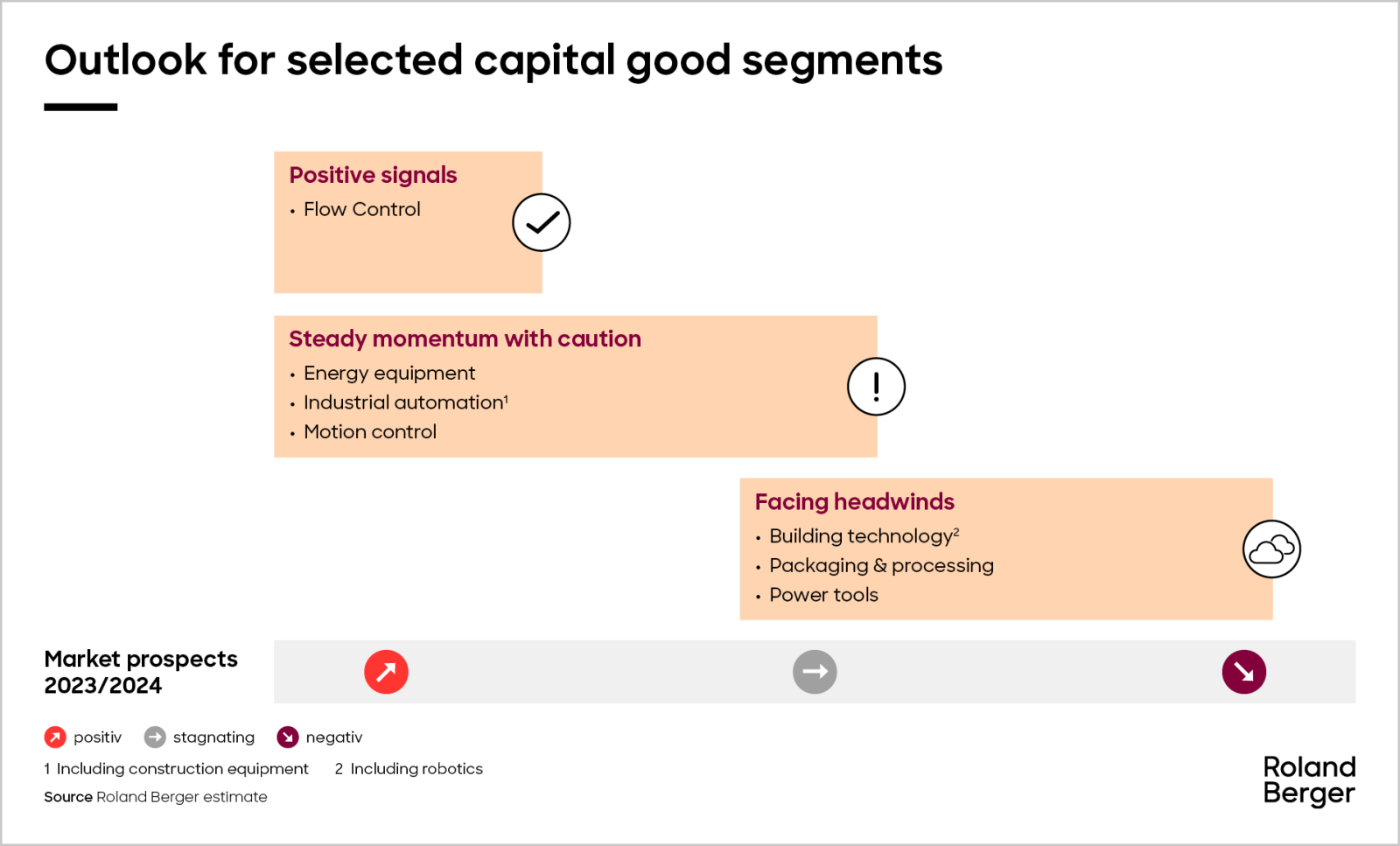

2. Verticals: Strong variation in growth prospects across industries

The outlook for various industry segments varies significantly. Sectors such as metal processing, automotive, and textile machinery are under significant pressure, as are energy-intensive enterprises in general. The capital goods segments that experienced a surge during the pandemic, particularly those linked to areas like home improvement and textiles, are now experiencing a swift normalization or correction phase. This is resulting in reduced demand, coupled with margin pressures from heightened pricing competition. The effect is reinforced by high stock levels throughout the value chain, leading to lower order levels and thus less need for production capacities and related investment in capital goods.

The construction industry shows regional variations. Economic uncertainties and rising interest rates are placing pressure on residential construction, with experts expecting activities to remain subdued at least until mid-2024. In contrast, non-residential and infrastructure projects remain more resilient, benefiting from localized production and government-backed initiatives. China faces unique challenges from the struggles of major real estate companies. Despite government interventions, market consensus sees a risk of prolonged stagnation in China's real estate sector until 2025 and low-digit growth until 2030.

These are also challenging times for capital goods companies supplying the automotive sector. The industry is undergoing major structural transformation, requiring established players to regain their market position and adapt their technology portfolio accordingly. Companies in this space must contend with delayed investments, demand volatility, and regulatory impact.

Nevertheless, certain sectors continue to perform well despite the challenges. Aerospace and environmental technology companies are thriving, along with those involved in energy transformation projects like hydrogen/electrolysers, carbon capture and usage technologies, or power transmission. In particular, companies focusing on renewable energy are profiting from an increasing number of public and private investments. At the same time, the oil and gas industry is facing an unexpected resurgence, driven by geopolitical events and uncertainties about energy security. There are also sectors that have proven resistant to economic downturns such as pharmaceuticals and medical technology. They have experienced stable or even growing demand and thus also increased their need for production equipment.

3. Offering: Companies with recurring revenue streams are well positioned

Capital goods companies in sectors like elevators, turbochargers, power generation equipment, and processing and packaging machinery have found resilience through service-and wear-part oriented models. Elevator companies, for example, offer maintenance and modernization services, while turbocharger manufacturers provide diagnostics and repairs. Power equipment providers offer maintenance and digital solutions, and machinery manufacturers extend services beyond manufacturing.

Seizing business opportunities around service and modernization have proved effective strategies, diversifying revenue streams and building customer loyalty, which are particularly crucial in times of economic uncertainty. Overall, the transition toward service and modernization offerings aligns with the broader industry trend of delivering comprehensive solutions and services.

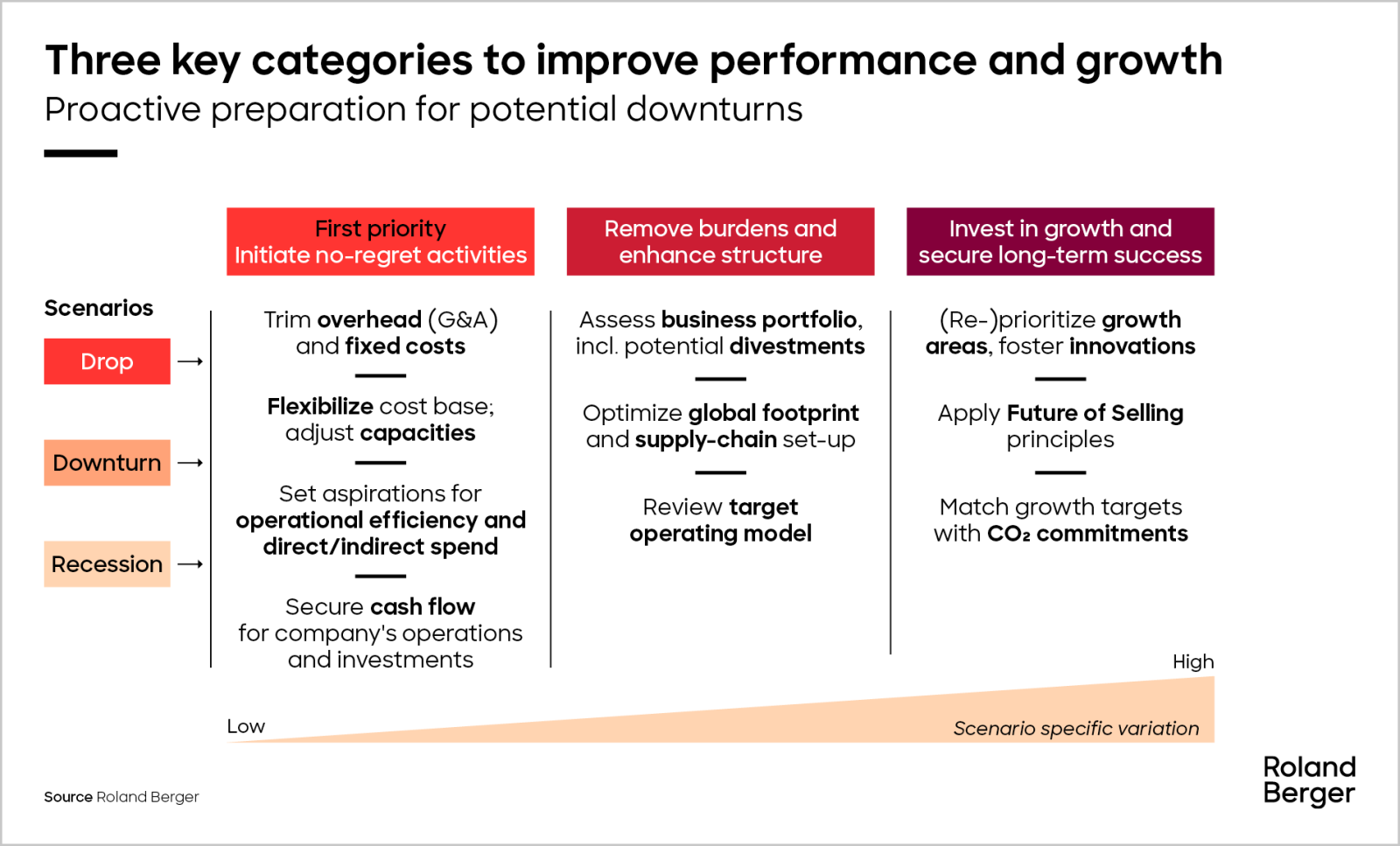

Why a proactive approach and consistent “no-regret” activities are vital

In the face of uncertainty paired with major structural changes, companies must adopt a proactive stance to successfully weather the storm. Roland Berger recommends dividing performance improvement and growth measures into three key categories that are adaptable to different scenarios: no-regret activities; structural enhancement; and long-term growth. While not imperative, we see value in adopting a scenario-based approach – preparing plans for the different degrees of economic challenge so they can be rapidly implemented depending on actual developments. See the infobox “Our perspective on scenario planning” for more details.

Start with “no-regret” activities

Initiating no-regret activities should be a standard item on every company's agenda during budget phases or regular performance reviews, particularly after turbulent times and rapid growth periods, such as those experienced during the Covid era. These activities serve to shed inefficiencies and reduce unnecessary costs without compromising the company's market success.

Typical areas of focus encompass trimming overhead and fixed costs without jeopardizing competitiveness. Additionally, transparent demand forecasts, which can mirror various scenarios, should prompt companies to proactively adjust resource levels and capacities. This allows them to make their cost base flexible by planning with a leaner resource structure and footprint, potentially relying on a temporary workforce to manage fluctuations, pushing automation of overheads, and offshoring to lower cost locations.

Furthermore, top management should establish clear ambitions regarding operational efficiency, which must be upheld during a downturn. By setting clear expectations for the leadership team, they can identify improvement measures that go beyond continuous improvement activities. These measures may include process automation and realizing cost synergies in areas such as shared services. Procurement emerges as a critical focus, as both direct and indirect expenditures have surged due to rising costs for raw materials, components, and services. Capital goods companies can seize this opportune moment to optimize purchasing expenses by engaging in rigorous procurement programs and renegotiating terms with suppliers.

Lastly, it is essential to address potential cash flow stress when entering a downturn period. Roland Berger recommends forecasting and planning cash flow development with foresight. Setting thresholds and planning with more restrictive CAPEX expenditures can help safeguard the company's financial stability during challenging times.

Remove a company's legacies and recalibrate its structure

Uncertain times present an opportune moment for companies to refocus their attention and allocate resources more strategically. Now is the right time to assess the portfolio of business fields and consider their contributions to the company's success. This evaluation can lead to divestments of non-strategic and low-performing business segments, providing clarity on where to channel resources more effectively.

Several companies have already launched initiatives to optimize their global footprints and supply chains. Some are driving regionalization and placing their manufacturing locations closer to key end markets. This might be Mexico for the US market or Eastern Europe and Portugal for Europe. Geopolitical tensions and the lessons from Covid have revealed the value of resilient regional structures, even for global enterprises. Those who operate globally should reassess their approaches to worldwide operations and consider adapting their footprint accordingly, extending beyond manufacturing to include other key functions like engineering. This strategy not only mitigates risks but also enhances cost-efficiency and reduces future carbon emissions.

In times of uncertainty, companies can also refocus by assessing their target operating model. We recommend creating a lean organizational structure for improved efficiency and agility while encompassing comprehensive end-to-end process design to optimize operations across the entire value chain. Additionally, a robust data and system architecture can support seamless information flow and analytics, which provides a great base for a migration to

S/4 HANA.

This holistic approach to the target operating model not only enhances the company's current capabilities but also positions it for future growth and digital transformation.

Emerge stronger from the downturn and secure long-term success

Emerging stronger from a crisis involves a two-fold strategy: first, optimize cost structures and ensure adaptability during downturns; second, understand the importance of prioritizing growth areas and aligning organizational resources effectively. This approach is particularly relevant for companies exposed to industries undergoing fundamental transformations like the automotive sector. Navigating such uncertain times requires long-term positioning and foresight.

The B2B sales landscape is also evolving, driven by the integration of technology like AI and the Internet of Things as well as changing customer preferences. Successful companies leverage these emerging digital technologies to enhance their market activities, enabling them to create a distinctive and personalized user experience throughout the customer journey. This not only gives them a competitive edge but also optimizes their operational processes and efficiency. Roland Berger predicts that approximately 70% of the B2B customer journey will soon be digital, with the remaining 30% following traditional approaches. Our ‘Future of Selling’ approach sheds more light on this vision.

Lastly, aligning growth targets with decarbonization ambitions is crucial. Short-term cost reduction efforts may seem at odds with carbon reduction costs, but long-term sustainability goals are non-negotiable. Striking this balance is paramount for a company's resilience and long-term viability.

Our view on scenario planning

We are frequently asked about the value of

scenario planning

and its role in preparing a range of strategic responses based on economic expectations. We recognize its great advantages and stress the importance of involving the organization in this process, including strategy identification, prioritization, and refinement. However, it's crucial to ensure that scenario planning aligns with a company's principles and scale.

Resource constraints can deter scenario planning. Nevertheless, we firmly believe that this should be viewed as an opportunity to delineate clear priorities and showcase the foresight necessary for steering the business effectively. Scenario planning enables managers to make informed decisions amid uncertainty, restoring confidence in overcoming challenges and the ability to succeed (see also: "Scenario-based management – Taking action in an uncertain world").

Conclusion

Capital goods companies in the DACH region currently face a complex array of challenges, which can vary considerably across industries and regions. Managers must gain a thorough understanding of their business units and the factors affecting them, particularly geography, verticals, and offering. Weathering the storm of economic uncertainty and structural upheaval requires companies to adopt a proactive stance. While not imperative, we also see value in adopting a flexible, scenario-based approach. Roland Berger offers an extensive range of consulting services to help your company emerge stronger from the downturn.

Download the full PDF

Article

Capital goods companies in DACH at a crossroads

DACH capital goods firms face uncertainty as machine export's early 2023 promise dims due to dwindling orders

![{[downloads[language].preview]}](https://www.rolandberger.com/publications/publication_image/Cover_Downturn_in_Capital_Goods_2023_DE_DT_download_preview.jpg)