At Hannover Messe industry leaders showcase their latest solutions. We help them make the courageous decisions to unlock value in a sustainable industry.

Capital goods players outperform expectations in a challenging year

Roland Berger's annual deep dive finds that the capital goods industry exhibited a year of revenue growth and increased profitability despite a slowdown in real volume growth

2023 was a challenging year with slowdowns in the end markets served by Capital Goods players and continuation of difficulties presented by geopolitical tension and supply chain bottlenecks. Weathering these impacts, the industry was able to hold onto price increases to grow both revenue and profitability. In-depth analysis by Roland Berger looks at the performance of ten key segments of the capital goods industry – and investigates what lies ahead for each one.

"Winners are winning on two scores: First, they have managed to increase their invested capital by roughly 40 percent compared to 2020. And second, that puts them in a position to continue growing now, while others are struggling."

A key theme of last year's Capital Goods study was the strong uncertainty in the market. While industrial players had continued to grow coming out of the pandemic, backlogs were expected to soon start drying up, supply chain bottlenecks remained a challenge – including a clear trend towards localizing key parts of the supply chain – and geopolitical tensions were on the rise everywhere. Industry experts and market participants were therefore cautious in their outlook for 2023.

Balancing out these challenges was the potential for a strong year if capital goods players were able to maintain the high selling prices established through the pandemic from late 2020 to 2022, while at the same time improving their cost base. Possible strategies included passing on the cost of raw materials to customers, improving efficiency and de-risking supply chains and leveraging technology across operations.

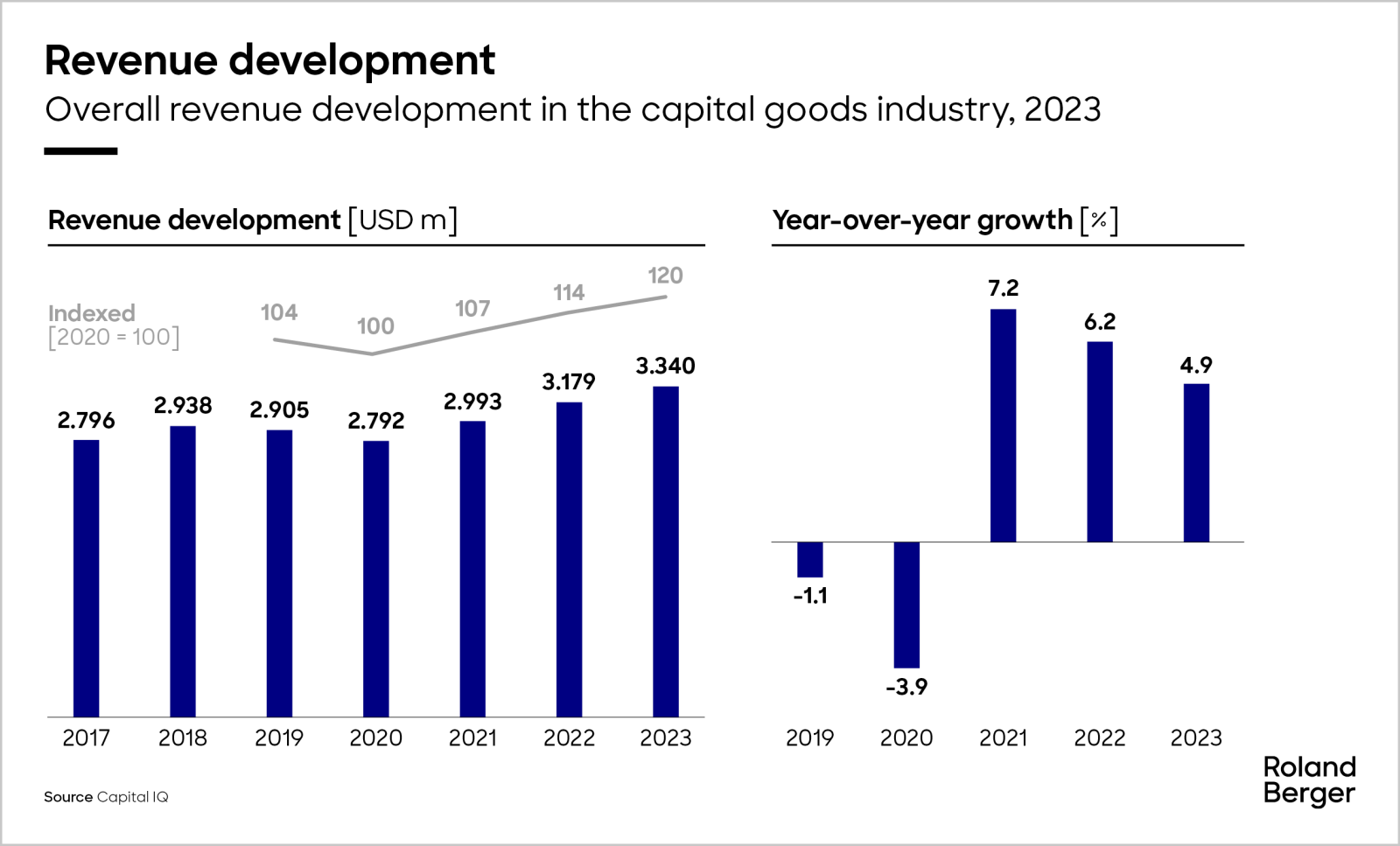

Expectations did become reality and difficult market environments came to fruition. Despite the challenges, the capital goods industry exhibited a relatively strong year in 2023, recording around five percent top-line growth. True, that was down on the eight percent plus growth rates in 2021 and 2022, but the growth in 2023 was also much less driven by the catch-up effect following the pandemic. Growth in 2023 was the result of the industry’s ability to sustain the price levels that had recently been established. Another important contributor to growth were government incentive programs and public investment, such as the US’s Inflation Reduction Act, which helped buoy and level real volume demand.

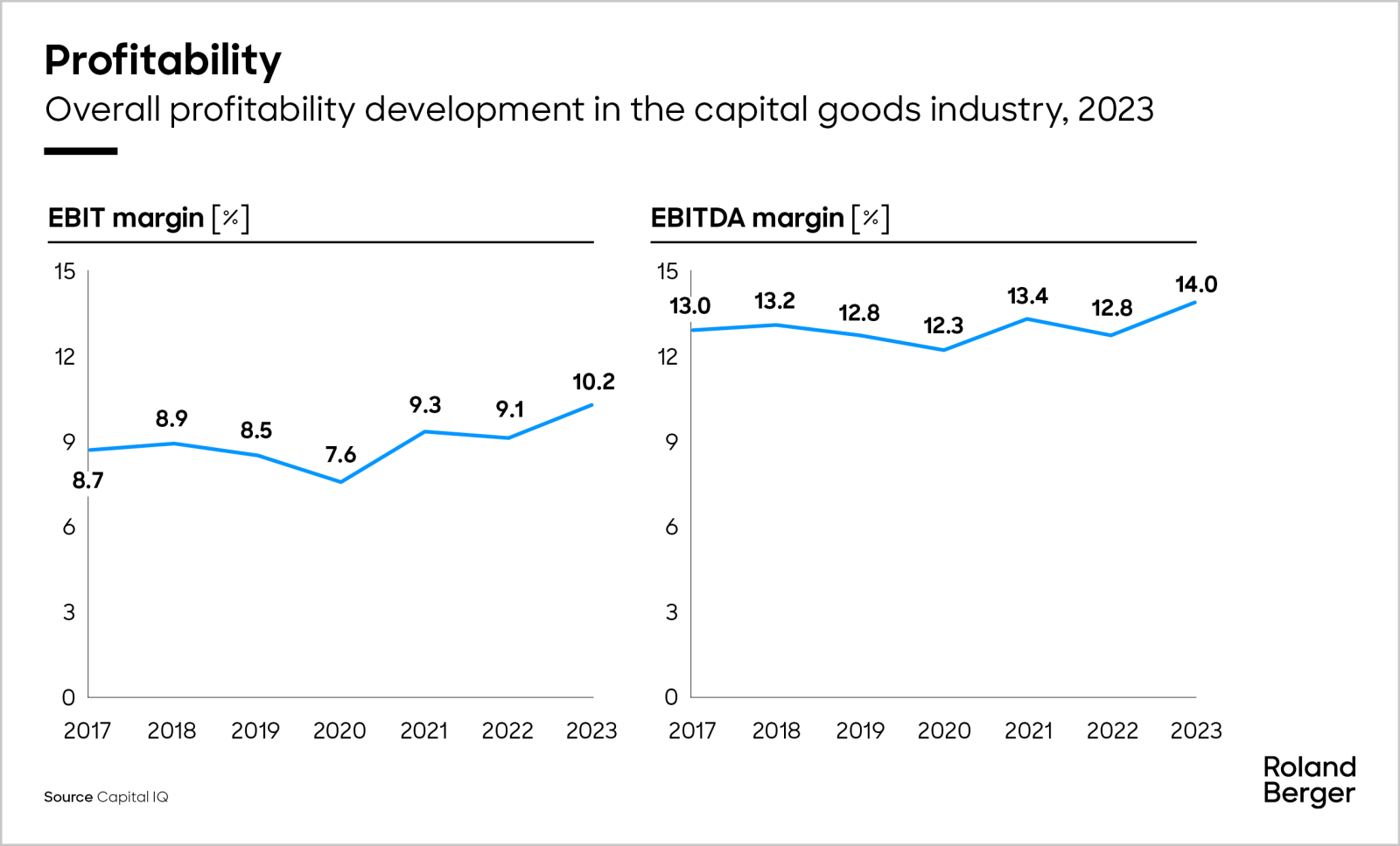

Even more impressive is the fact that the industry was able to increase its profitability by more than one percent compared to 2022, pushing up EBIT to 10.2 percent and EBITDA to 14 percent. Both these figures are higher than pre-pandemic levels. Capital goods players, in addition to sustaining price levels, successfully passed on material price increases to customers and improved supply chain efficiency. That differs from their approach in previous years, when they were more focused on stabilizing supply chain dynamics.

"Capital goods companies' profitability is now higher than before COVID-19. That is quite an achievement – the ability to hold on to price took many observers by surprise."

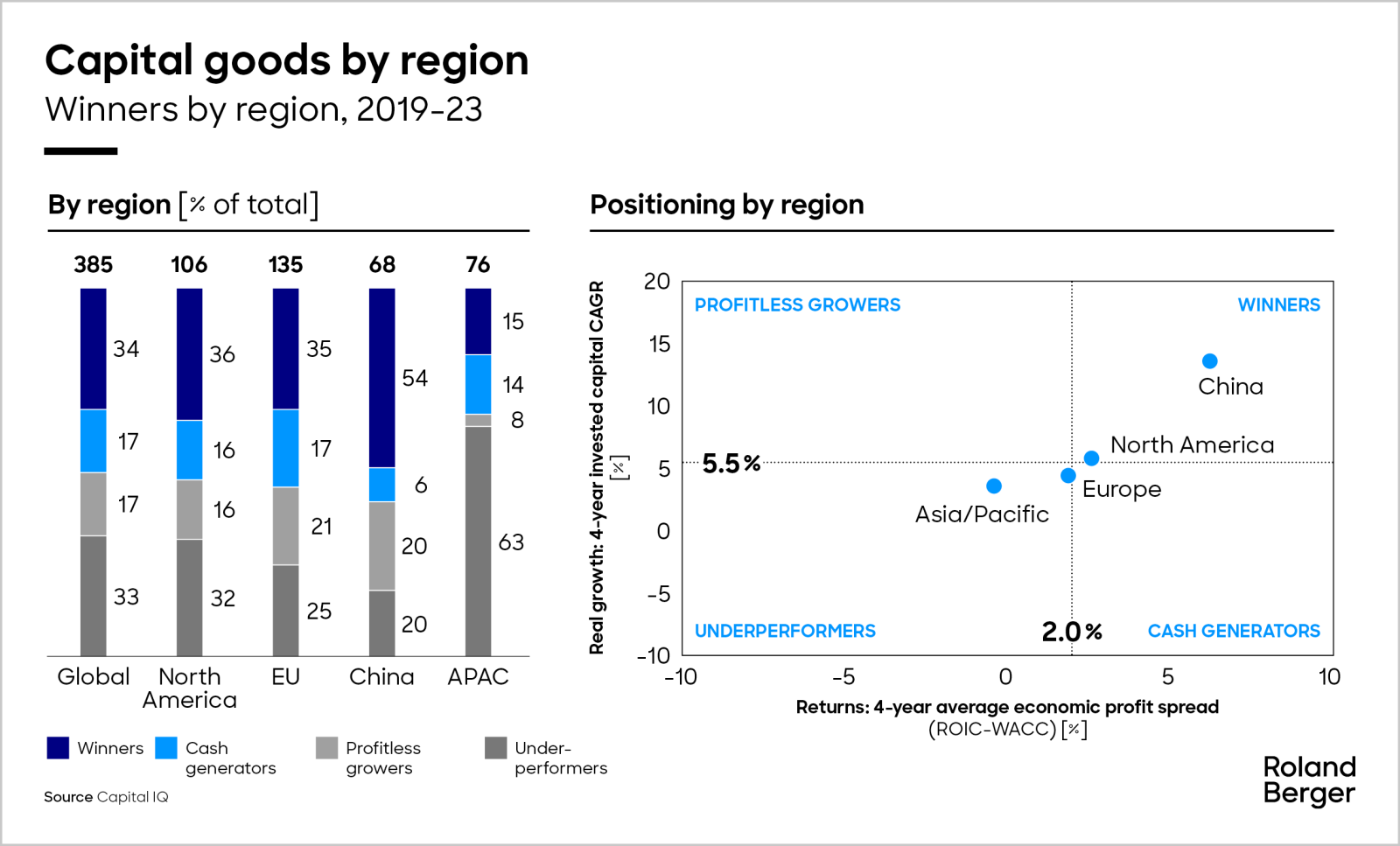

High interest rates presented a unique challenge to the industry in 2023, as in 2022. No surprise, then, that invested capital grew slower than revenue and profitability in 2023. Yet, the companies we call "Winners", despite being fewer in number than other players, are responsible for 65 percent of the total growth in invested capital in our dataset. Compared to 2020, these Winners have increased their invested capital by around 40 percent, while other players saw a decrease of five percent overall. This confirms the resilience of Winners and their ability to continue to build for the future, despite a challenging overall economic environment. They also enjoy a consistently lower debt-to-equity ratio, remaining at approximately 0.6 since 2019, while other players have only recently started to come back down to their pre-pandemic levels (the group we call "Cash generators" are closest, at around 0.7 in 2023).

How does this picture differ regionally? The overall strength of the North American economy is visible in our results. Thus, while other regions have lost Winners, North America has held steady. China, affected by the challenging economic environment, has seen elevated growth rates compared to other regions but the slowdown in growth here is also visible in our results. Europe experienced slower GDP growth due to lower consumer spending and elevated energy prices but overall its capital goods players have proven resilient.

Looking ahead

In the short-term future, we expect a year of continued top-line growth, albeit at a slower pace. Uncertainty about outcomes will remain, driven by factors such as geopolitical tension and ongoing conflicts. 2024 will also see many elections with global implications, including the US Presidential elections, elections to the EU parliament and to the Indian Lok Sabha (lower house of Parliament). Central-bank decision timelines on interest rates will likewise affect the economy. And it remains to be seen if the currently high price levels that contributed to the 2023 results will be sustainable in the long term. However, we expect weakening inflationary pressure in Europe and the ramp-up of infrastructure programs in North America to help support growth.

"With more than 40% of the world's population potentially going to the polls this year, 2024 is inevitably a year of uncertainty."

Winners will likely enjoy a particularly advantageous position due to their strong balance sheets and the investments they have made in the current environment. Other players will be limited in terms of making capital investments due to the now higher interest rate levels. By continuing to make investments, Winners can thus put even more space between themselves and their competitors.

The mid to long-term future remains difficult to predict, due to the many sources of uncertainty. In 2025 and beyond, as in 2024, Winners will continue to benefit from the investments that they are able to make while others cannot. They also stand to benefit from a first-mover advantage in new technologies, such as artificial intelligence (AI), advanced robotics and next generation manufacturing. Technologies like these will continue to mature and generate significant gains in efficiency and productivity for those that adopt them. This combination of advantages – having the resources to expand, plus early investment in productivity-boosting technology – is something that Winners should capitalize on.

From big picture to detailed analysis – Deep dive into individual segments of the capital goods industry

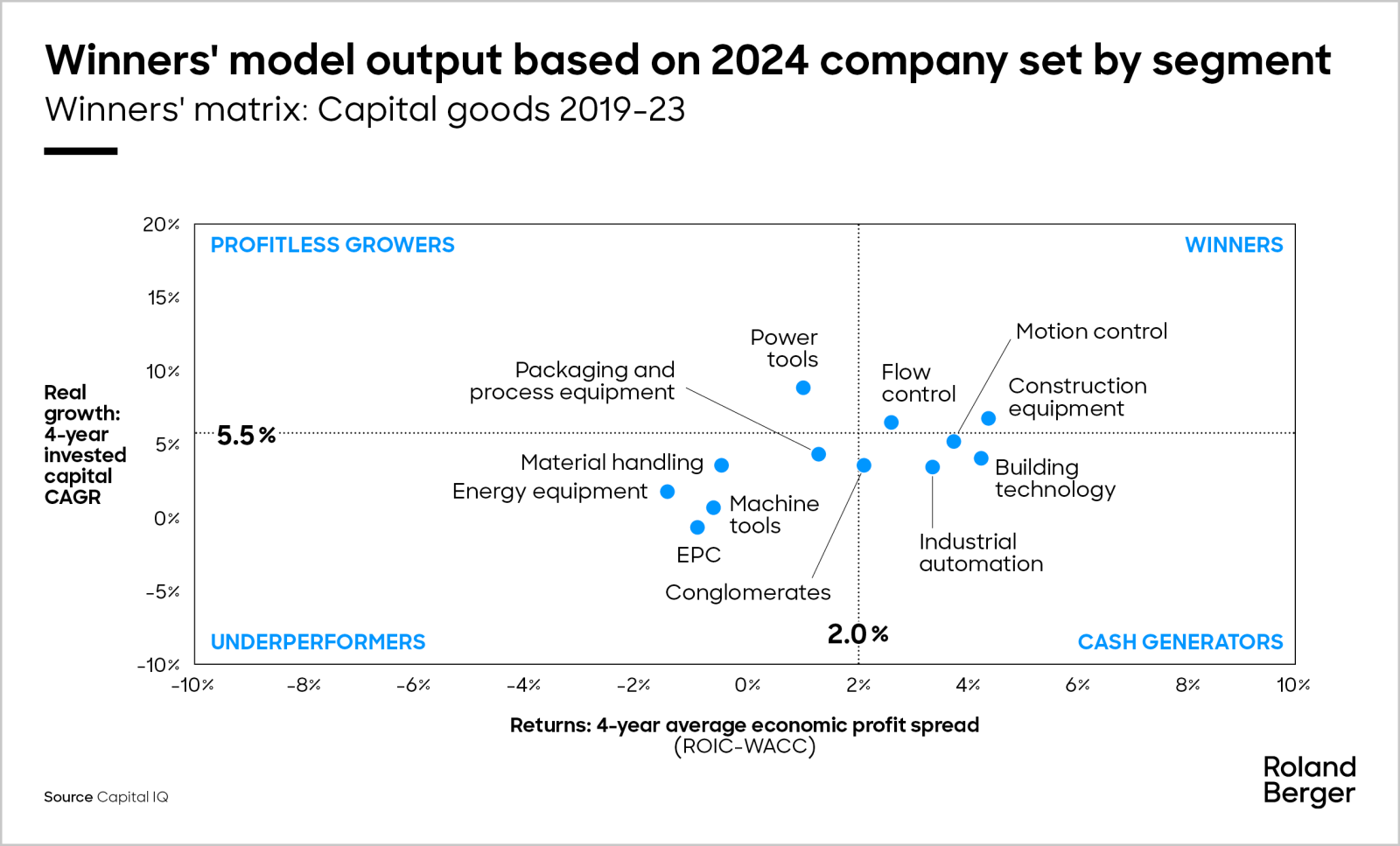

Our analysis this year looks at 10 pivotal segments of the capital goods industry: building technology, construction equipment, flow control, industrial automation, energy equipment, machine tools, packaging and process equipment, motion control, power tools, EPC (engineering, procurement and construction) and material handling. Once again, we examined 386 publicly traded capital goods players, took a deep dive into each of these individual segments and isolated those factors that set the Winners apart from the rest.

Request the full PDF here

Register now to access the full study, to learn more about the performance of key segments of the Capital Goods industry.

Further readings