Inflation has returned – and alongside, we are currently witnessing a reversal of monetary policy by central banks around the world.

Corporate Financing: The big squeeze

By Matthias Holzamer and Markus Held

Rising debt financing costs and how to mitigate against them

Can European businesses still handle their debts? With interest rates having risen sharply in recent years, Roland Berger undertook a second annual study to gauge the impact of higher debt financing costs on eurozone companies, with a focus on Germany. We have discovered that leverage ratios will settle at a high level as interest rates gradually decrease and profit margins improve. The urgency to manage cost of capital remains high.

"The increased interest levels combined with the challenging leverage ratio and interest coverage outlook as well as the ongoing transformational pressure in various industries will lead to an increasing importance of alternative financing concepts and providers."

Inflation and rising interest rates have been a major drag on European business in the past few years. Just as margins were being squeezed, costs increased – especially the cost of borrowing. The European Central Bank’s (ECB’s) rapid notching up of interest rates to tackle inflation has resulted in soaring debt financing rates, with exponential increases after a long period of very low rates.

In April 2023, Roland Berger assessed the growing financing pressures on eurozone companies in a report entitled “Falling earnings, rising interest rates – How companies can solve their financing dilemma". A year on, we have returned to the subject. In a new and updated study, we re-examine the impact of rising debt financing rates and declining margins on eurozone firms. In particular, we forecast costs and margins to 2026 for all major German industries (with a case study on construction), analyze their leverage risk and provide an outlook for different types of alternative financing.

Under pressure

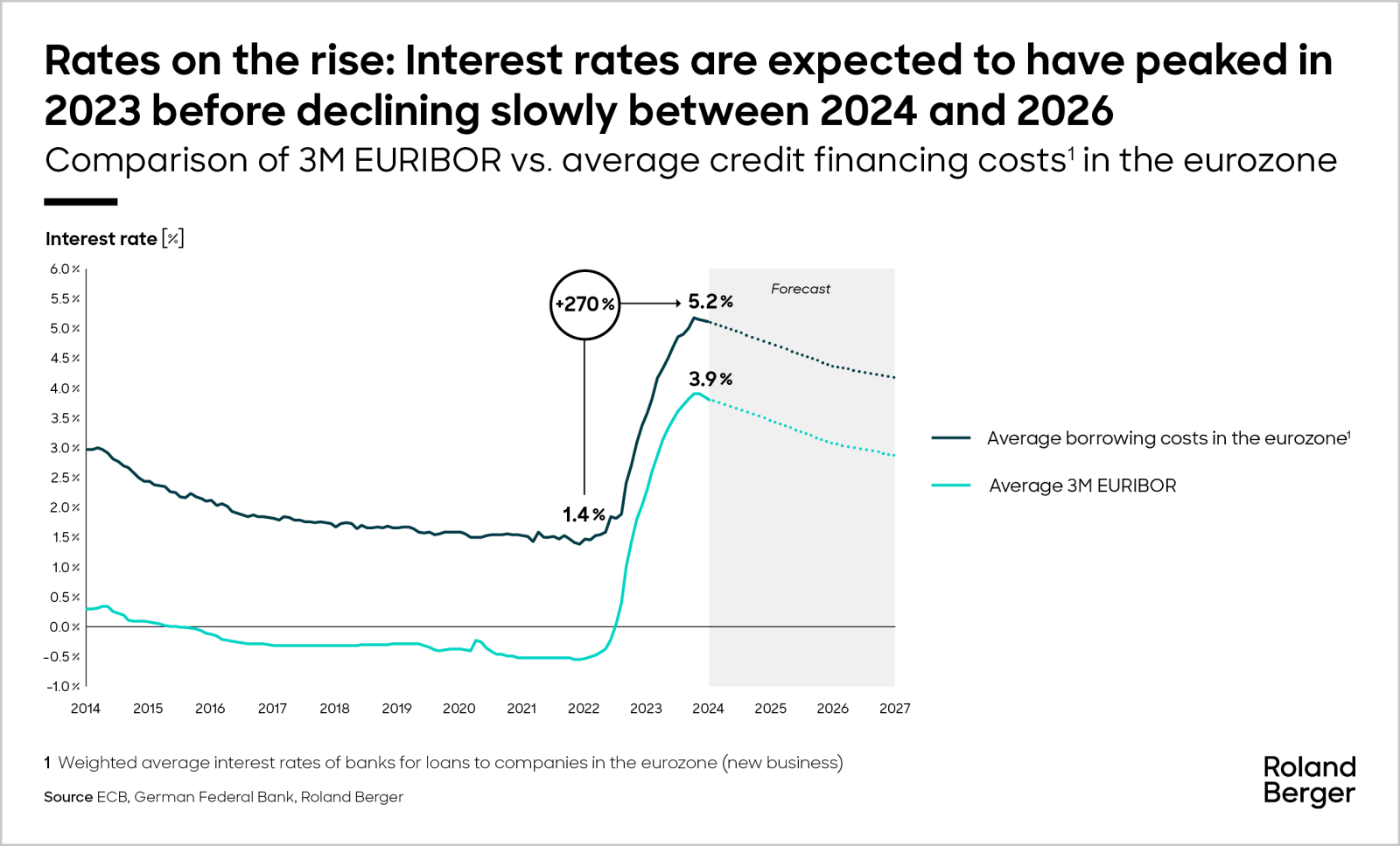

The three-month Euribor interbank rate rose from -0.6% in January 2022 to more than 3.9% in December 2023. This drove average borrowing costs for new businesses in the eurozone up from 1.4% to 5.2% in this time frame. Individual circumstances in each country mean that actual debt financing costs vary considerably across the eurozone, however, with a spread of 3.2 percentage points between the highest (Estonia, 6.9%) and lowest (Malta, 3.7%) values. Roland Berger estimates that after peaking in 2024, interest rates will gradually decline through to 2026 but remain at a generally high level compared to 2022.

"The regime change in interest rates is here to stay – with money no longer free but actually quite expensive CFOs need to actively manage cost of capital."

These rises will result in significant additional interest costs for eurozone companies. The total loan portfolios of eurozone companies have risen by 2% per annum since 2014, reaching EUR 5,114 billion in December 2023. Medium-term (1-5 year) loans accounted for EUR 1,091 billion of this amount. If these positions are refinanced, eurozone companies may face additional interest costs of up to EUR 41 billion because of the increased interest rate level.

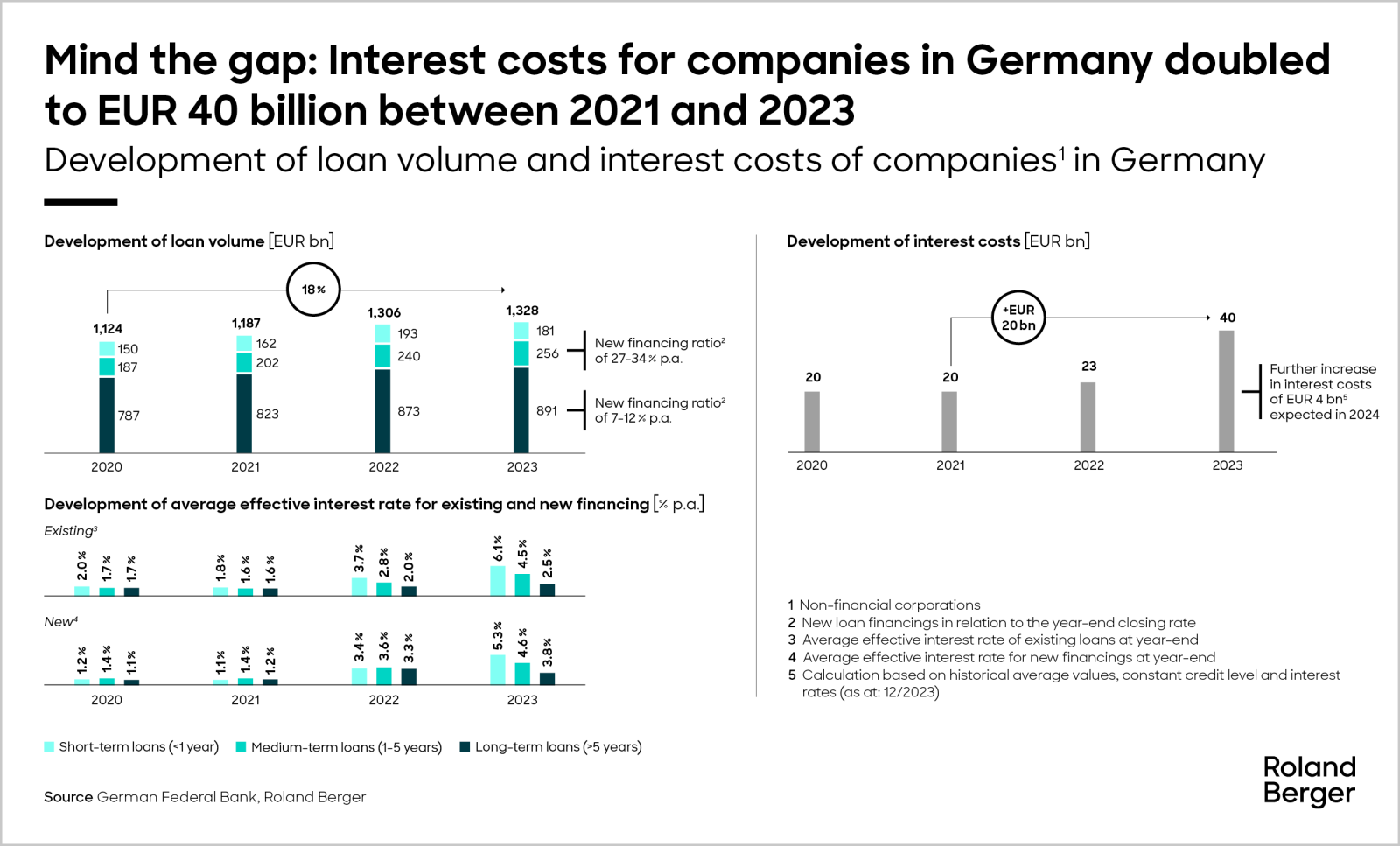

The experience of German companies in the past few years highlights the challenges. Loan volumes in the country increased by around 19% between 2020 and 2023, from EUR 1,124 billion to EUR 1,334 billion. In 2020, interest costs were EUR 20 billion. But by 2023, after several sharp rises in interest rates and the loan volume increase, interest costs had doubled to EUR40 billion. They are expected to reach EUR 44 billion in 2024.

At the same time as having to deal with higher interest costs, eurozone companies are facing several other challenges. These range from the aftermath of the COVID-19 pandemic and the outbreak of war in Ukraine to the energy transition and lack of qualified labor. Such challenges have a significant impact on the finances and operations of all major industries. In the full report we look specifically at the problems faced by the construction industry .

Forecasts and outlook

To better understand the effects of higher interest rates and costs on eurozone companies, Roland Berger carried out a study to forecast leverage and interest coverage ratios for German industries to 2026. The key results are detailed in the full report, with selected highlights and analysis given below:

Costs and margin forecasts

- We expect interest rates will fall from 3.5% in 2024 to 2.9% in 2026, and remain at a generally high level

- EBITDA margin declines are expected in all industries in 2024 due to continued rising costs. Margins will stabilize in 2025 and grow in 2026.

Leverage

- We calculate that the 0.8 percentage point year-on-year EBITDA margin decline in 2023 led to a leverage increase of 47.6% across German industries

- Our analysis shows that German industries with already high leverage, such as Aerospace & Defense, show the greatest risk of additional leverage

Interest coverage ratios

- There was a significant year-on-year decline in the average interest coverage ratio (EBITDA/interest) in all industries in 2023 (10.51x), with a projected significant decline in 2024.

- Interest coverage ratios are expected to recover ground from 2025, with a slight improvement expected in all industries by 2026.

With financing challenges mounting up for eurozone companies, our study also includes outlooks for different forms of financing, from bank loans to bonds and IPOs. We find that the right financing vehicle for a company depends heavily on its credit rating and the associated credit risk premiums, as well as the available collateral portfolio and the resilience of the available cash flows.

For more information, please download the full report or contact one of our experts. We look forward to hearing from you.

Request the full PDF here

Register now to access the full publication and learn more about the impact of higher debt financing costs on eurozone companies, especially Germany.

Further readings