The electric vehicle and EV charging market enjoyed a surge in late 2022 despite continued high energy prices.

EV Charging Index: Expert insight from Spain

E-mobility is gaining traction in Spain, despite underlying technological and financial uncertainties

Main page

Spain’s EV market is showing encouraging growth, despite uncertainty around the dominant technology and financial viability. Its public charging infrastructure is expanding rapidly, although the availability of fast charging remains an issue.

"Growth in Spain’s public charging network is encouraging, but there is still much to do regarding availability and interoperability."

Strong growth for EVs, but underlying uncertainties persist

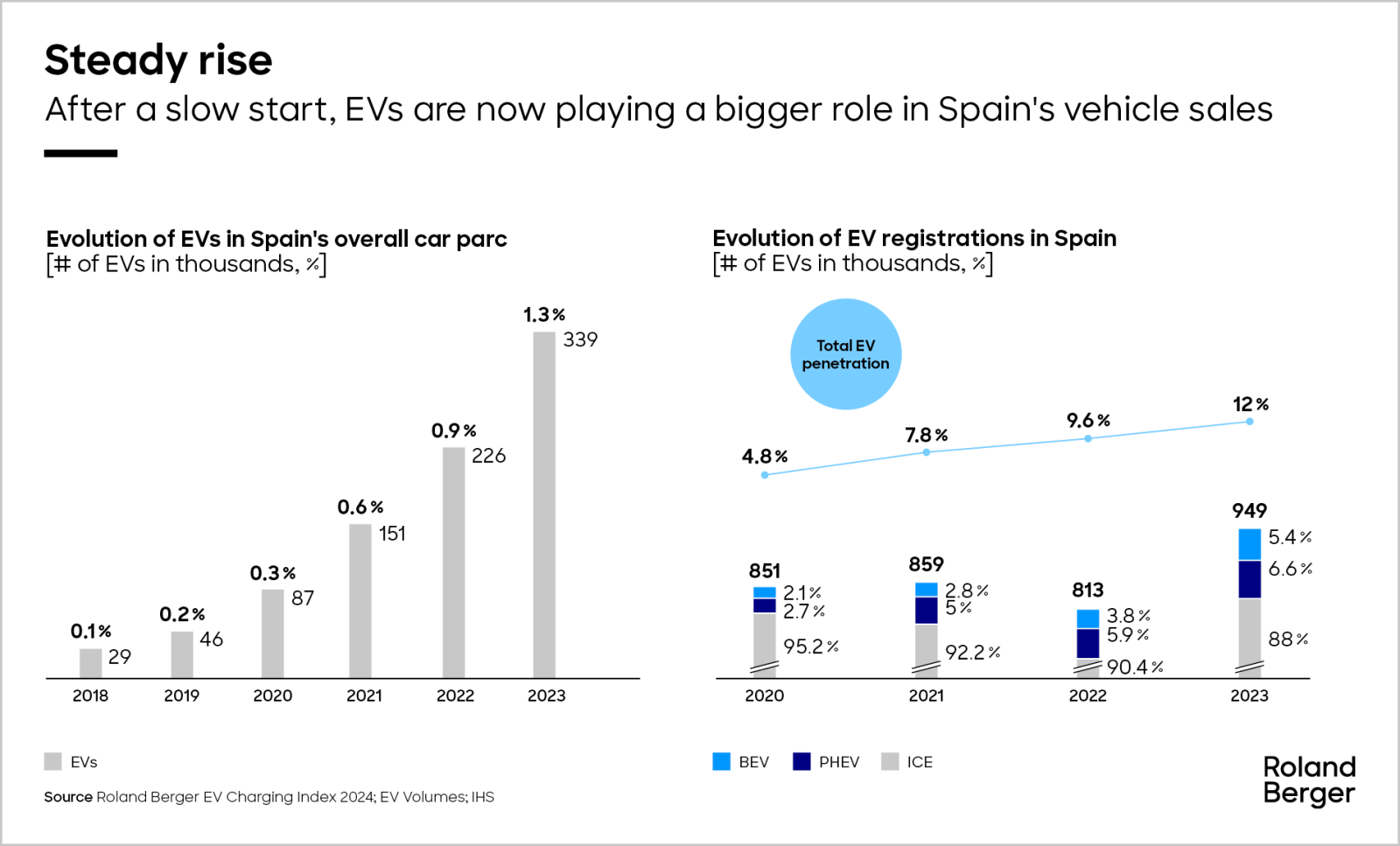

The Spanish EV market continued its strong growth trajectory in 2023. More than 100,000 new vehicles were registered, as the sales penetration rate rose from 9% at the end of 2022 to 12%.

Economic incentives, including subsidies of up to EUR 7,000 for vehicle acquisition and funding for charging infrastructure, have been crucial in driving adoption. These incentives help close the pricing gap and address the issue of charging availability. However, uncertainties persist, particularly regarding the dominant technology in the medium term (hybrids vs. full electric vs. biofuels), and 2024 already shows signs that hybrids are set to remain mainstream.

This uncertainty is being fueled by OEMs’ declarations of delaying electrification goals and pushing for biofuels. The reduction or removal of subsidies in more mature markets has also raised concerns among potential buyers around EV ownership, with leasing accounting for almost a third of EV sales in Spain.

Encouraging public infrastructure growth

In 2023, Spain added approximately 9,000 new public charging points, giving it a ratio of 11.6 charge points per EV, slightly behind Europe’s leading nations. This growth is being driven by various regulations and initiatives to foster infrastructure expansion, particularly in parking areas and gas stations. Law 7/2021, for instance, mandates that by 2023, petrol stations with an annual sales volume of more than 10 million liters must have at least one fast-charging point of 50kW or more. It also requires 2.5% of parking spaces in public lots to have charging points.

Economics explains the current network mix, with two thirds of charge points at 22kW or below and less than 10% of charge points currently above 50kW. Amid the uncertainty, most charge point operators (CPOs) are deploying slower but cheaper charge points to lock in premium locations with the aim of upgrading to faster technology as the market matures. But while slow charging may meet the needs of the average EV user today, Spain still lacks sufficient fast-charging infrastructure.

Beyond this, there is also still much to do regarding charge point availability and interoperability, which remain key challenges for the sector.

Diversity in the charging market

Spanish utilities, especially Iberdrola, and Endesa through its Enel X arm, lead the market in both slow and rapid charging segments, with both making strong commitments to the sector.

Independent CPOs such as Zunder and Wenea have different focuses: Zunder is concentrating on en-route stations, while Wenea is installing more destination charge points. Eranovum stands out with a mixed portfolio and its own generation capabilities, which could prove advantageous by giving it access to cheaper electricity.

Large international players such as Ionity and Tesla are focusing on the fast-charging segment in select locations along major high-speed routes in Spain, competing primarily with Spanish challenger Zunder.

Meanwhile, large oil companies are entering the market through partnerships with leading players. BP, for instance, has partnered with Iberdrola to deploy 12,000 charging points, while Cepsa has partnered with Endesa. Repsol appears to still be deciding on the right strategy, although it is already developing its own charging network.

Further readings

Register to receive future EV charging updates

Register now to to discover the latest insights, emerging trends and upcoming challenges in the EV and EV charging markets.