More than 80% of respondents think public charging has become easier in the last six months.

Adam Healy

Partner

London Office, Western Europe

After a period of rapid expansion, 2023 saw a slowdown in EV sales and infrastructure growth in some regions, painting a mixed picture in our latest EV Charging Index. Meanwhile, the charging market looks vibrant as OEMs increase their involvement. Infrastructure development is still struggling to match vehicle sales, but consumers believe public charging is improving, with fast DC charging on the rise in all almost markets.

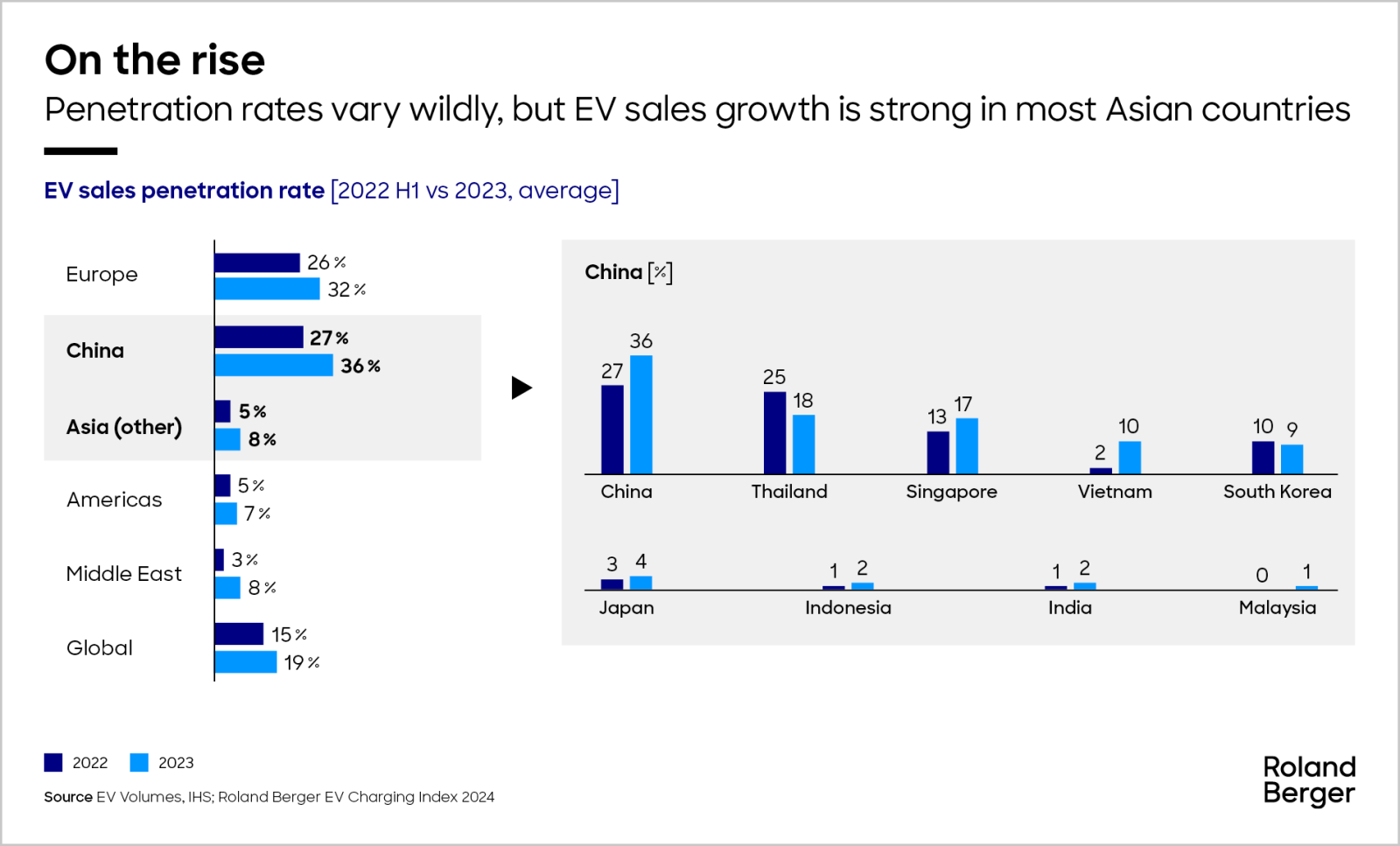

The EV sector currently faces numerous headwinds, including high energy costs, inflation, and reduced subsidies as some governments shift their funding focus from vehicles to charging facilities. Global sales penetration rates continued to rise in 2023, but there was strong variance across countries, influenced by factors in policy, supply, and demand. Asian countries and the Middle East saw the biggest rises, but South Korea and Germany both saw sales penetration rates decline.

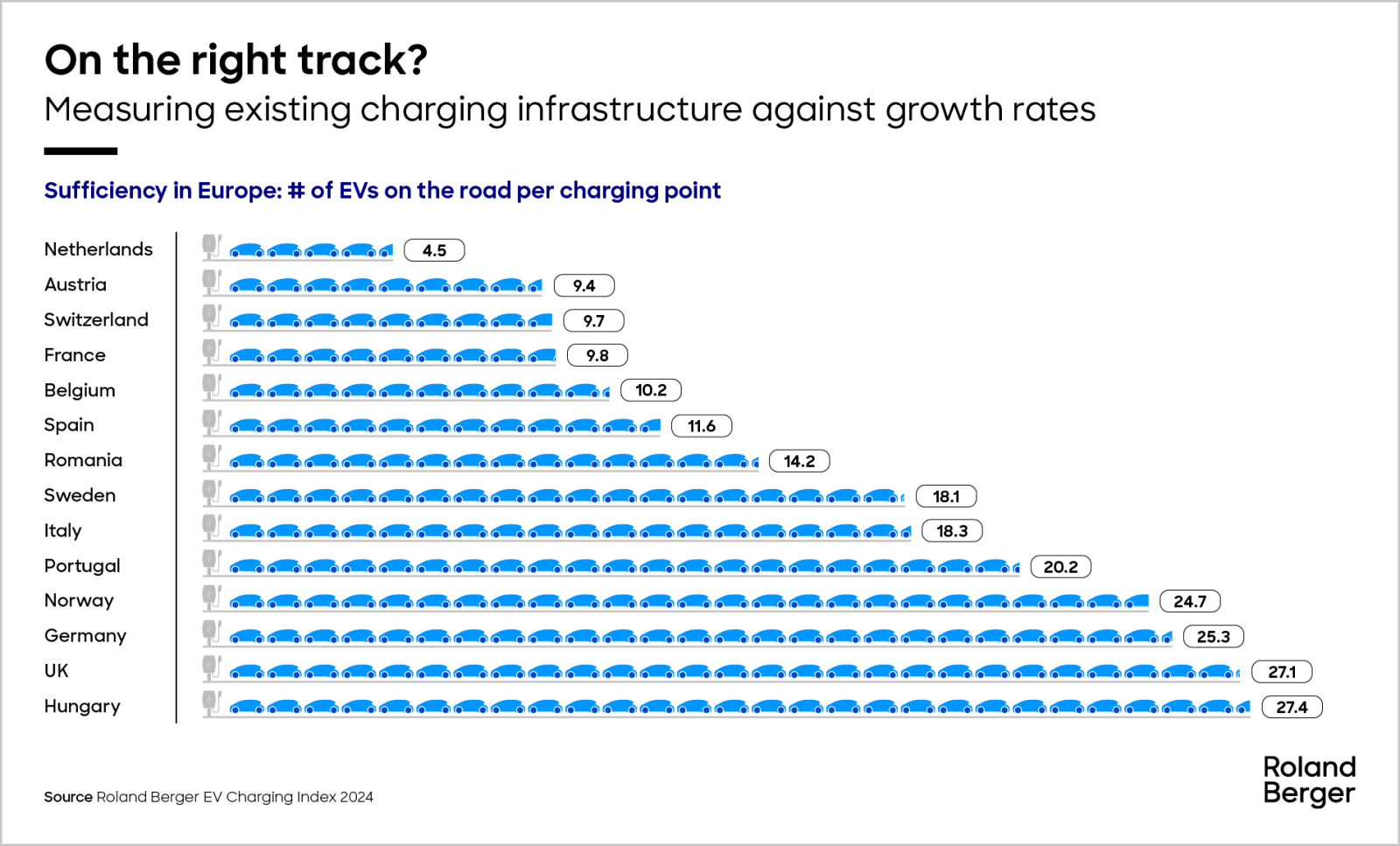

Infrastructure development has been mixed, not yet catching up with EV sales which impacts charging sufficiency ; but customer satisfaction improved across the board as more DC chargers are installed.

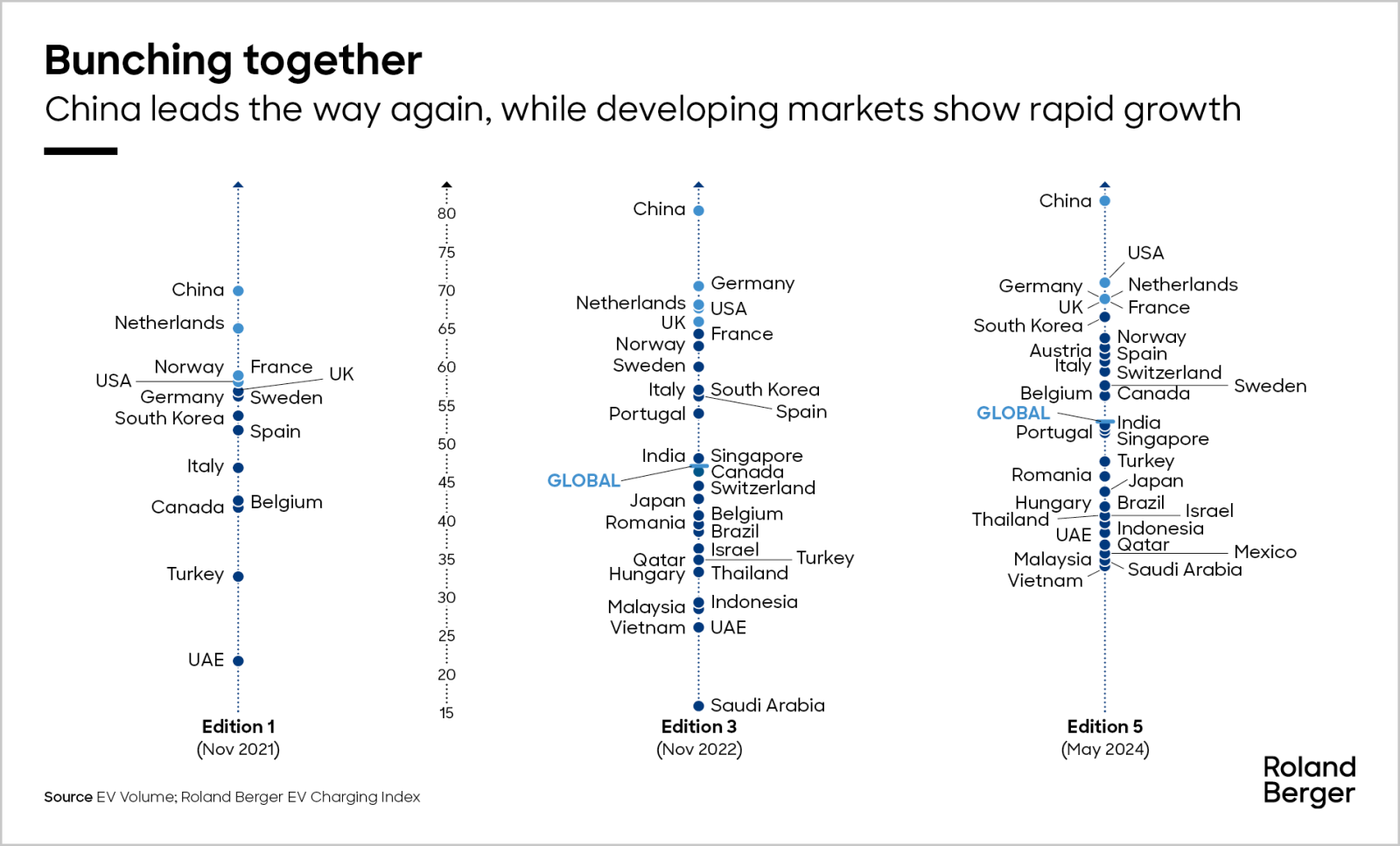

So what does this mean for our overall rankings?

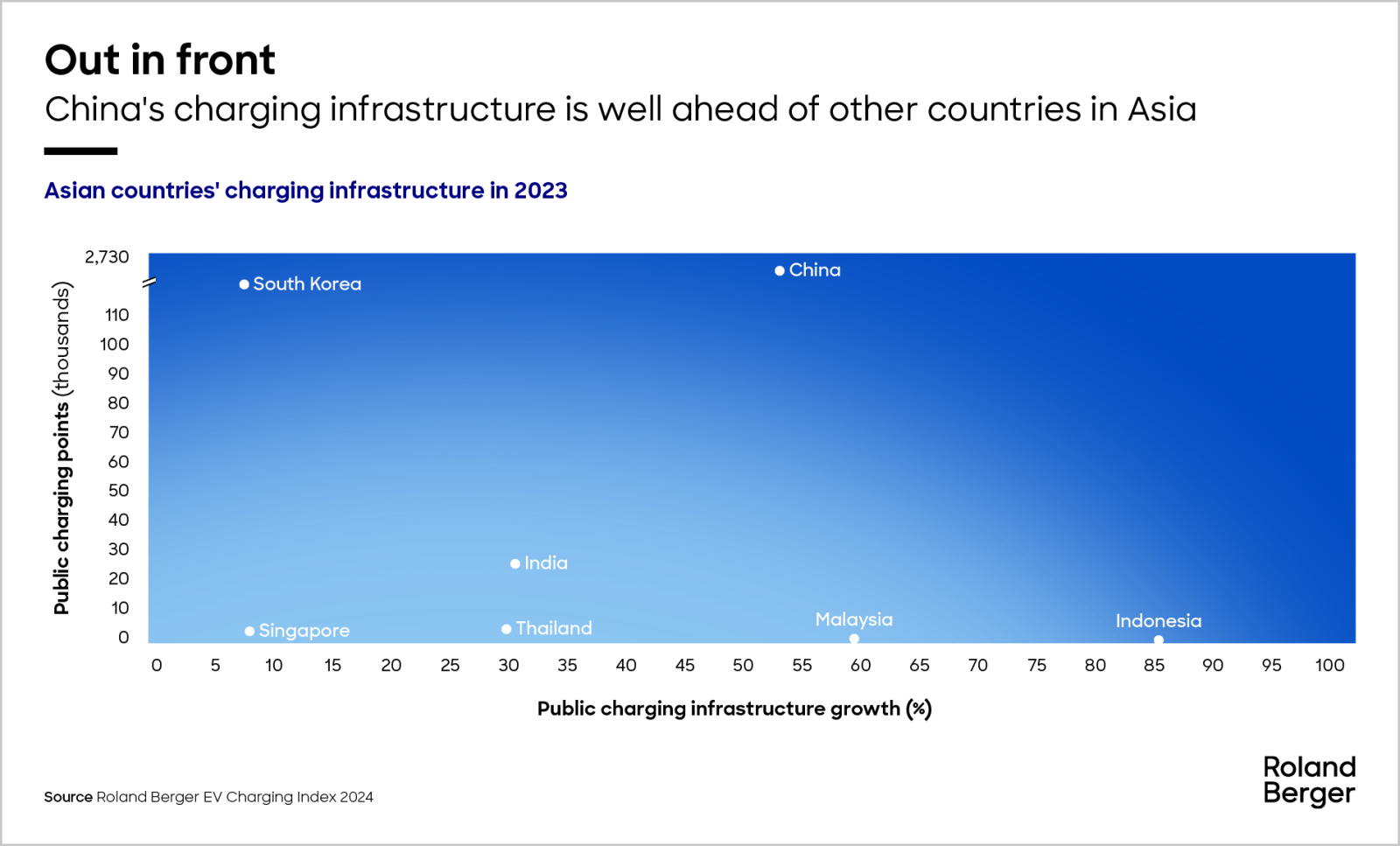

China is still scoring at the top of the rankings. Its closest competitors – Germany, the United States, and the Netherlands – have all seen their scores either stagnate or decrease, a trend seen across most established markets in 2023. Meanwhile, developing markets in the Middle East and Southeast Asia are showing rapid growth in EV sales and closing the gap to the leading nations.

This fifth edition of the EV Charging Index covers 32 markets in five regions – Europe, China, the Americas, the Middle East, and Asia (other) – and 31 indicators. It is based on industry interviews, primary research, and a survey of more than 15 800 participants, conducted in Q2 2024. In it, we present the overall findings and focus on four main areas: EV penetration, policy, infrastructure, and market dynamics.

In addition to the summary below, you can download the full report here. You’ll also find detailed insights from our local experts in certain markets.

Note: Some rankings have changed due to changes in the scoring methodology implemented in 2025

While some developing markets showed the strongest growth rates for EV sales, China continued its impressive progress with a 36% sales penetration rate in 2023. With more Chinese OEMs launching new models, pricing is becoming increasingly competitive.

Other established markets fared less well. In Western Europe, some mature markets, such as Germany and the Netherlands, have lowered or removed subsidies, slowing the pace of EV growth. In the United States, plug-in hybrids are proving increasingly popular, comprising 20% of US sales in 2023. This reflects continued skepticism of the public charging infrastructure – a sentiment shared by consumers in Western Europe.

Overall, our survey shows considerable divergence in infrastructure development. China’s charge point growth has matched its impressive progress in EV sales, for instance, but in the United States public charging growth slowed in 2023. Indeed, despite a growing focus on charge point development, vehicle-to-charger ratios stagnated or declined slightly across all regions except the rapidly evolving Middle East market.

Where things have improved is in fast charging, with the share of DC chargers in public charging infrastructure growing across all regions. On a global level, almost a quarter of all public chargers are now DC.

Despite mixed sentiment among investors, the charging market is proving increasingly dynamic. Buoyed by advantages in technology and cost-efficiency, Chinese players are expanding their international footprint, especially in Europe. In Europe and the US, new market participants from adjacent value chains are joining in, including utilities companies and supermarket chains.

While OEMs are yet to be major players in most markets, they are increasing their involvement, where they can help drive EV sales by expanding infrastructure. According to our survey, branded charging networks are an important factor when buying an EV, particularly in China, India, and the Middle East.

Participants continue to test new business models and technologies. A wide range of solutions likely to be appropriate for different use cases are still to emerge, and there is still no clear direction as to where the market will land. For more information on our EV Charging Index rankings as well as the latest developments in EV sales, e-mobility policies, charging infrastructure, and charging market dynamics, please download a copy of the full report.

Register now to get the full study and discover the latest insights, emerging trends, and upcoming obstacles in the EV and EV charging markets in different regions.

_person_144.png?v=1687234)

_person_144.png?v=1776278)