_large_image.png)

![{[downloads[language].preview]}](https://www.rolandberger.com/publications/publication_image/Roland_Berger_WEB_24_2673_Infrastructure_investment_outlook-DT_download_preview.jpg)

New solution page on shifting paradigms in infrastructure investment, focusing on how Investors must rethink their strategies and be more proactive.

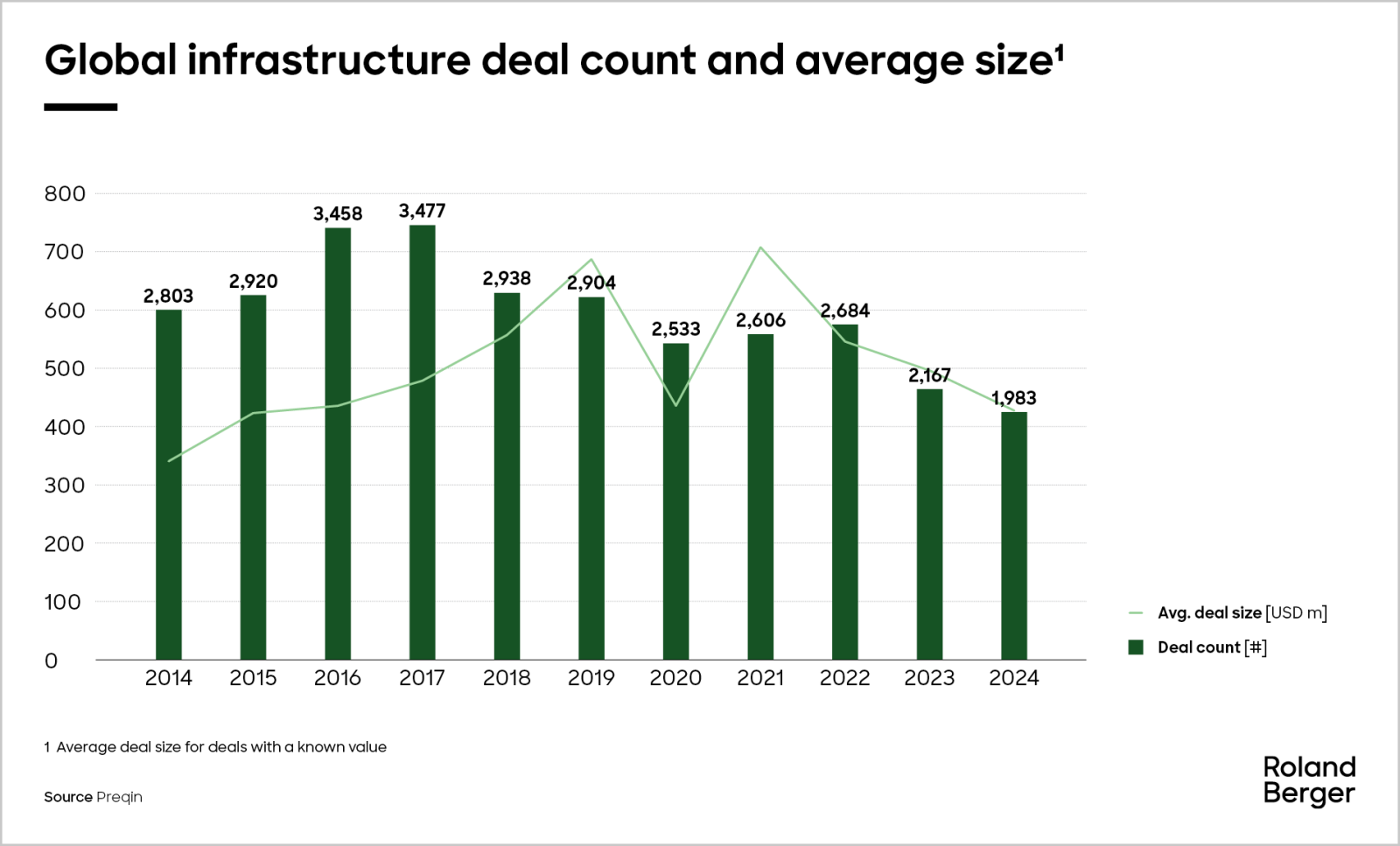

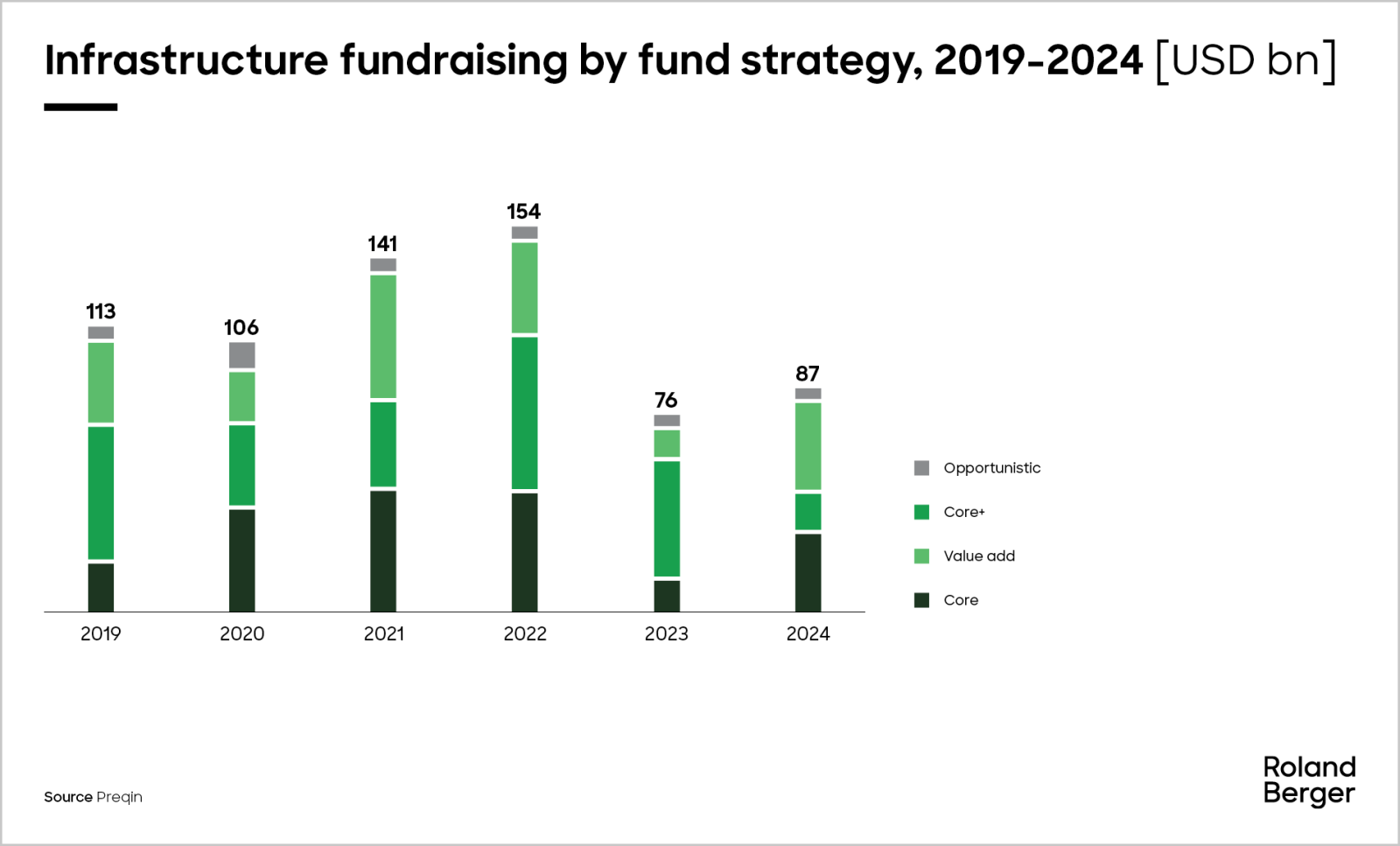

Despite a soft start to 2025, infrastructure investors are cautiously optimistic that favourable trends will continue to drive the need for infrastructure capital.

Siongkoon Lim

Partner

London Office, Western Europe