China's economic trajectory is undergoing a profound transformation. After years of investment-driven growth and export-led expansion, diminishing returns and shifting demographics are forcing a strategic pivot. Policymakers now emphasize domestic consumption and indigenous innovation to build a more resilient, self-reliant economy. Technological advancements - from AI to green tech - are positioning China as a formidable global competitor. Yet, the transition to a consumption-led model remains uneven, and geopolitical headwinds are intensifying. Our current issue of RBI Quarterly explores how China's evolving growth model, technological ambition, and shifting global alignments are reshaping its role in the world economy.

Pressures amid a strategic shift in the Chinese economic model

In the face of an increasingly polarized international environment and an intensifying

US–China rivalry,

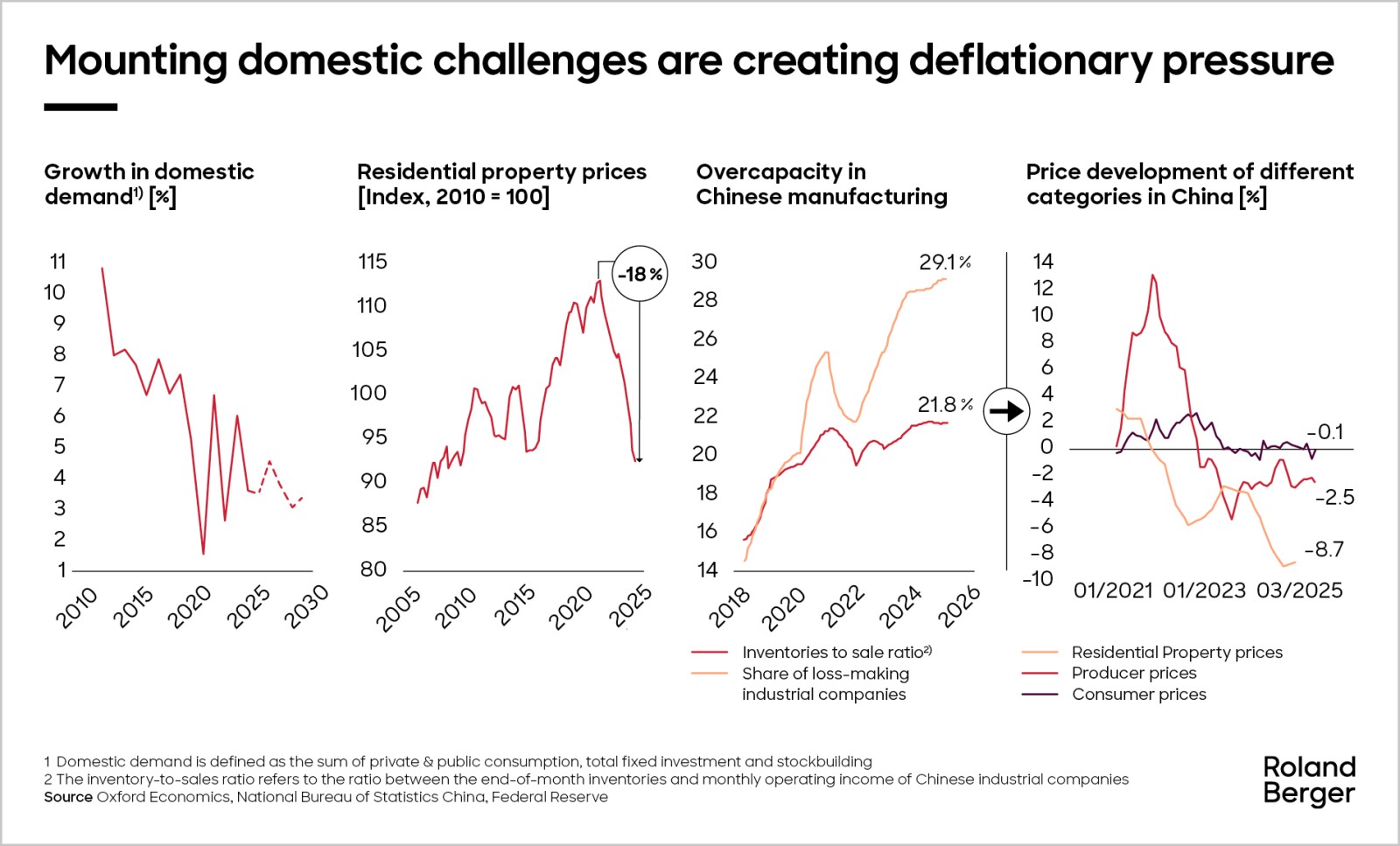

China is undertaking a decisive pivot away from its long-standing export-driven, investment-heavy model toward one that focuses on domestic consumption and stabilization. However, the transition is proving difficult. Structural imbalances - long masked by credit-fueled investment-driven growth - are surfacing in the form of weak domestic demand, a deeply troubled property sector, and industrial overcapacities, which are causing deflationary pressures.

Taken together, these trends suggest that China may be slipping into a balance sheet recession, where private sector entities prioritize debt repayment over spending or investing, even when monetary policy is loose. In response, Beijing is deploying fiscal stimulus and loosening regulatory constraints. The 2025 Two Sessions - the annual gathering of the country's top political bodies - marked a decisive shift with expanded deficit targets and specific support measures. However, fiscal transfers to households – such as tax cuts or stimulus checks - are largely ineffective during a balance sheet recession because households are not constrained by a lack of income, but rather by damaged balance sheets.

Structural reforms - including enhanced social safety nets and urbanization - will be critical to restoring momentum. While China faces headwinds, its large population, policy agility, and potential for income growth offer significant opportunities if the transition is managed effectively.

"Chinese firms are no longer just reacting to global constraints — they're actively shaping the next phase of globalization on their own terms."

Amid mounting macroeconomic pressures, China's tech sector is undergoing rapid and resilient transformation. Triggered by escalating US export controls, Chinese firms have accelerated domestic innovation in semiconductors,

AI,

and hardware. The result is a surge in homegrown breakthroughs - from Huawei's home-made 7nm chip-powered Mate 60 Pro to the rise of domestic AI leaders like DeepSeek - signaling a shift toward tech self-sufficiency.

Rather than succumbing to constraints, China has transformed adversity into momentum. A vast STEM talent pool, reverse brain drain, and strategic state support are fueling a virtuous cycle of R&D, commercialization, and capital reallocation. As domestic firms adopt locally made chips, the ecosystem strengthens from design to foundry.

By 2024, China had emerged as the global leader in 57 of 64 critical technologies, surpassing the US in the breadth of its innovations. Despite geopolitical tensions, China's rise up the technological value chain is not only resilient, but also accelerating.

"What we are witnessing is not just a simple shift of the Chinese economy, but a strategic overhaul of how and where Chinese companies create value."

Faced with structural headwinds at home and rising geopolitical pressure abroad, Chinese companies are accelerating their model of

globalization.

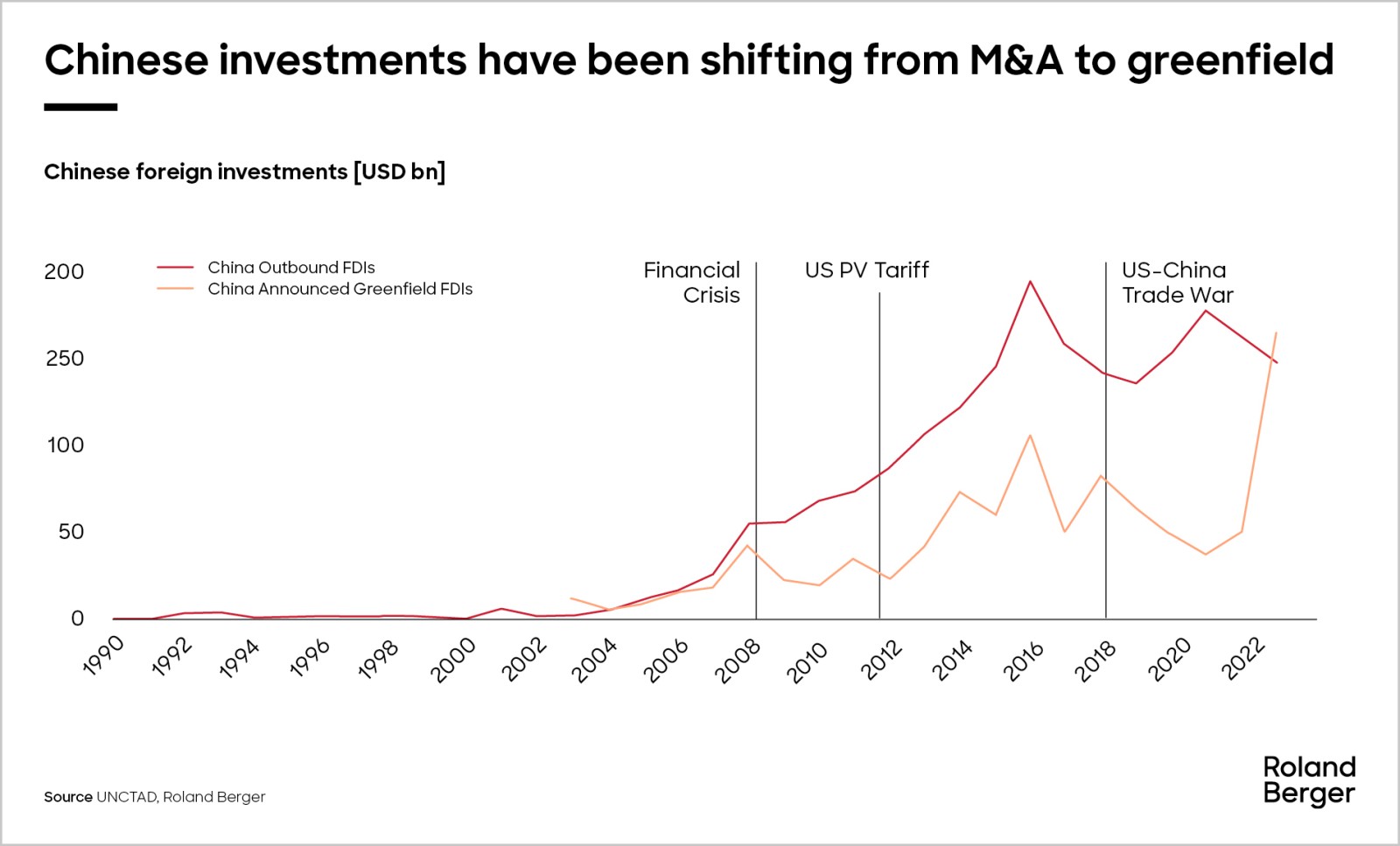

What began as a response to an earlier wave of deflation and a tariff shocks on Chinese solar PV manufacturers in 2012 has evolved into a comprehensive internationalization strategy — not merely remaining the "world's workbench" and exporting goods, but building global footprints across supply chains, factories, R&D, and brands.

The 2008 financial crisis marked the beginning of China's M&A-dominated foreign direct investment (FDI), as Chinese firms seized opportunities to acquire distressed global assets. Meanwhile, the 2012 PV anti-dumping tariffs sharply accelerated China's shift toward greenfield FDI to bypass trade barriers. The US–China trade war, which began in 2018, had already prompted Chinese firms to shift production to countries such as Vietnam and Mexico to avoid tariffs and maintain access to key markets, such as the US and the EU. The need for supply chain resilience was reinforced by the subsequent pandemic, while ongoing trade tensions further incentivized Chinese firms to invest abroad.

From home appliances and electronics to EVs and clean energy, Chinese firms are adapting to localization demands and tariff barriers by investing in production hubs across Southeast Asia, Europe, and the Americas. Cross-border platforms like Temu and Shein are reshaping global e-commerce, while industrial giants in the renewable energy sector are establishing vertically integrated supply chains abroad. Amid a prolonged period of producer price deflation and a tightening global trade environment, the imperative to "sail out or sell out" has become more urgent. Chinese companies are now drawing on lessons from Japan's lost decades to secure their future growth through strategic globalization.

Download PDF

Article

Navigating disruption: China's economic model in a world in transition

China's economic trajectory is undergoing a profound transformation. After years of investment-driven growth and export-led expansion, diminishing returns and shifting demographics are forcing a strategic pivot.

![{[downloads[language].preview]}](https://www.rolandberger.com/publications/publication_image/roland_berger_web_25_2214_china_in_the_context_of_global_resetting_dt_download_preview.jpg)