ASEAN supply chains are also deeply integrated with Northeastern Asian neighbors. Economists usually use the flying geese pattern to explain the labor division in the region, with Japan as technology leader vis-a-vis newly industrializing economies and developing countries. In maximizing each economy’s competitiveness regarding cost and technology, the frequent cross-border transportation of a good during its production life cycle in the network of multinational enterprises (MNEs) leads to vibrant regional supply chains.

In the new RBI Quarterly, we will take a deep dive into the electronics and

automobile industries

– the main drivers of the regional merchandise goods exports – to illustrate the nature and trends of the alternative Asian value chain. Although the archetype textile and clothing industry is more conspicuous due to their consumer goods character, it mainly concerns CLMV (Cambodia, Laos, Myanmar and Vietnam) and accounts only for a small portion of their exports.

Because of its strong footprint in both the electronics industry and automobile production, ASEAN will play a bigger role in the re-configuration of global value chains with the goal of increasing supply chain resilience.

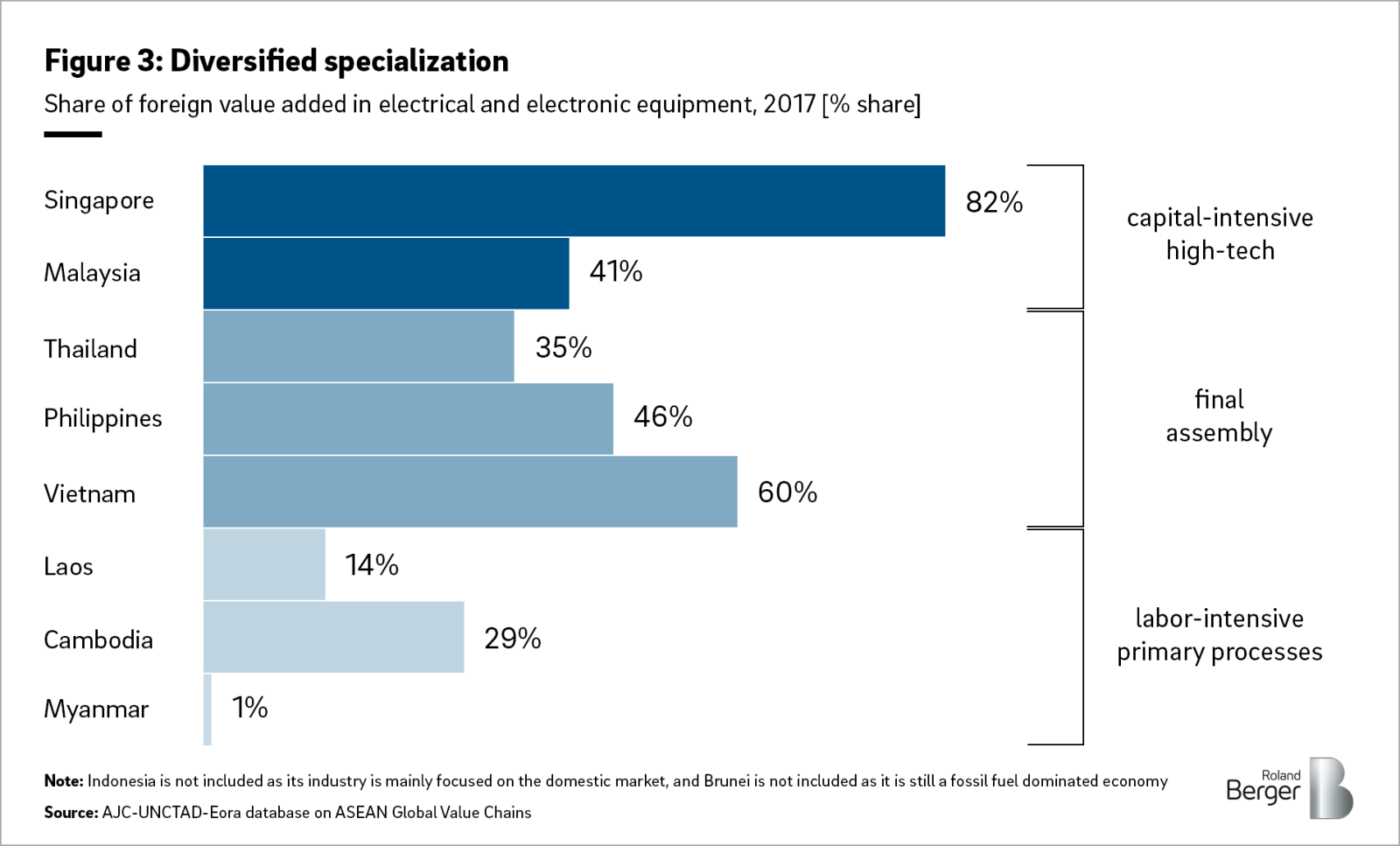

Due to integrated regional division of labor, we observe expansion of Japanese, South Korean and Chinese multinational firms as strong (and rotating) leaders – akin to the flying geese paradigm. However, the industry in the region is challenged by the conundrum of FDI-led industrialization that is mainly based on the technology input and supplier chain network of multinationals instead of competitive, indigenous companies.

Plenty of obstacles ahead

Southeast Asia will therefore certainly not replace China overnight as the world’s factory. For this to happen, its supply chains would need to become much more efficient and integrated. At present, commerce between ASEAN countries still faces too many obstacles. On the one hand, a lack of quality infrastructure inhibits a seamless flow of goods from the outset. On the other hand, essential regulation and legal agreements between countries are lacking as regional disputes and national ambitions stand in the way of beneficial consensus.

Additionally, the strong dependence on Chinese goods poses an additional impediment to the region’s ability to become the new global workbench. Likewise, the transition to a low carbon emission economy presents a major challenge for Southeast Asia. If not achieved fast enough, the region’s competitive advantages could dwindle rapidly.

Instead of a full trend reversal, we rather expect de-risking production strategies gaining further momentum, whereby a growing number of multinationals will reduce their exposure and start building up supply chain roles in Southeast Asian countries. As a natural outcome of this process, a growing share of the global value chain would almost automatically move to the region – and might help Southeast Asia to recreate the conditions that made China the world’s production powerhouse.

We thank Yu Wang for her contributions to this article.

![{[downloads[language].preview]}](https://www.rolandberger.com/publications/publication_image/roland_berger_ins_1125_rbi_quarterly_supply_chains_in_southeast_asia_cover_download_preview.jpg)