Roland Berger offers strategic approaches and proprietary solutions for sustained success in the financial services industry.

Operations in retail banking

From cost factor to powerhouse for customer experience

Operations within financial institutions face a paradigm shift. Long viewed as nothing but a cost factor, the responsibility for long-term customer care and securing customer loyalty is increasingly moving into the domain of operations. Particularly in the retail sector—with its numerous customer touchpoints and standardized, recurring activities—the potential for transformation is substantial. It is now increasingly evident that banking operations, too, hold immense promise to become a powerhouse of customer retention, operational efficiency, and innovation.

Financial institutions are placing greater focus on creating a positive and seamless customer experience. While “instant approvals” (e.g., in consumer finance) are already established in many areas, customers still have to wait 24 to 48 hours for their funds due to processing in operations. At the same time, the benefits of automation are expected to reduce cost pressure on banks and enable smaller units, especially within operations functions.

Against the backdrop of regulatory requirements, heightened competition, and new technological possibilities, banks must not just rethink their processes – they must be bold enough to give every part of their operations functions a renewed significance. Until now, end-to-end process optimization has often been approached solely from a sales perspective, with operations incl. any outsourced components not considered as an equally integral part of the strategy. However, with the increasing anchoring of the customer experience in operations and the trend toward smaller operations units, these functions must now be defined as the core and foundation of process design.

In retail banking, operation functions cover a wide array of activities that vary significantly depending on the organization. They represent back-office processes that ensure the smooth running of banking operations and predominantly involve simple, rule-based tasks with particularly high volumes. These functions are usually centralized within financial institutions but can also be located in different parts of the organization. Depending on the customer segment, specific focal points for operations tasks arise. These include payment processing, account and loan administration, fraud prevention, regulatory reporting, securities processing, general administrative tasks related to client relationships as well as IT-supported process automation and efficiency improvements.

"Regulation, competition, and customer demands leave no time for standing still. If you don't act now, you will miss the opportunity to establish your banking operations as a strategic asset."

Operations in the past and today’s challenges

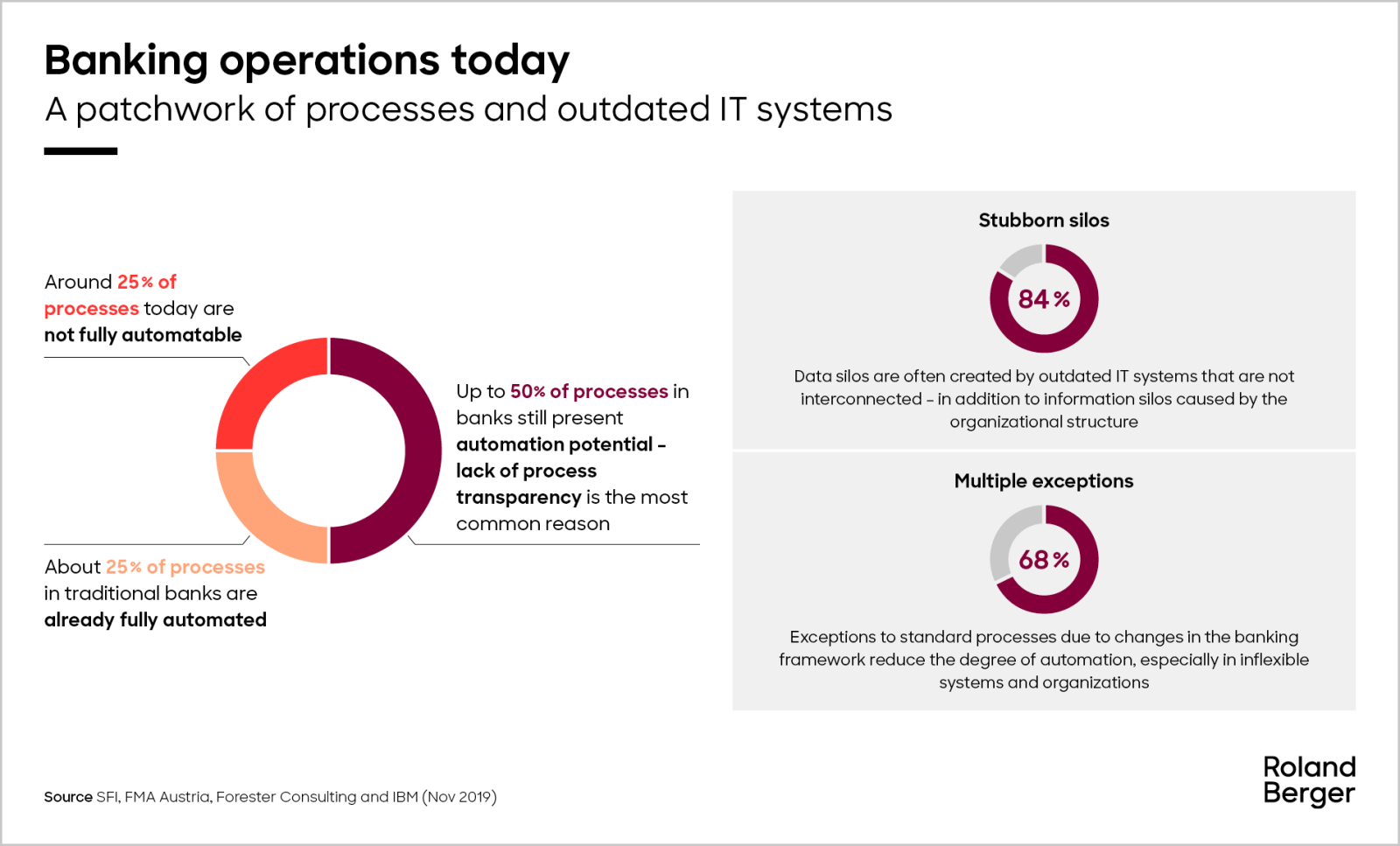

Traditionally, banking operations – especially in retail banking – were strictly separated from customer-facing functions such as sales, advisory or product management. Organized as back-office units, operations focused on transaction and payment processing, settlement, compliance, and risk mitigation.

The primary objectives of retail operations were efficiency, accuracy, and stability – delivering services reliably but with little direct interaction with customers. As such, operations functions played only a limited role in shaping the customer experience and were often perceived more as support functions or cost centres rather than sources of value or innovation.

This clear organizational separation led to siloed processes, fragmented accountability, and frequent handovers between departments and functions. End-to-end process thinking was rare, and customer journeys were often disjointed as a result. In many banks, operations evolved over decades around specific products or business lines, resulting in a patchwork of legacy systems and manual workarounds. This product-focused orientation of systems – shaped by market and market-follow functions – stands in contrast to the broader customer-segment-based setup of operations functions and tasks. The lack of integration and exchange between front and back office became increasingly problematic as digital technologies advanced and customer expectations shifted towards faster, seamless, and personalised services.

At the same time, growing regulatory requirements and rising cost pressures placed additional demands on operations functions. These historical structures – while robust in the past – have become constraints for many banks today, limiting their ability to respond quickly to change, implement large-scale innovation, and deliver the consistent high service quality that modern customers expect.

To stay competitive long term, banks will need to take advantage of the opportunities brought by modern technologies and automate their operational processes from start to finish. To learn more about a path to more efficiency and innovation in banking operations, please download a copy of the article.

Request the full PDF here

Register now to access the full study and explore AI’s role in financial innovation. Furthermore, you get regular news and updates directly in your inbox.

Further readings