In the new report by the international management consultancy Roland Berger, you can learn how to harness the growing potential of the green hydrogen market.

Ports and green hydrogen: Match made in heaven?

Green Hydrogen: The Future of Port Decarbonization

New research by Roland Berger predicts green hydrogen will decarbonize ports and their neighboring industries and lead to new port infrastructure (hydrogen production, import and refueling) in the coming years. Here’s what port authorities and concessionaires need to know.

"Ports are expected to use their strategic position, infrastructure, and logistical know-how to reduce emissions for not only themselves, but also neighboring industries, ground transportation and shipping. "

How will the world meet its ambitious emissions targets by 2030? That’s the gazillion dollar question, with a complex global answer that’s still a heavy work in progress, both politically and commercially.

One thing we do know: Green hydrogen (a clean but still-expensive energy source that only emits water vapor) will play a leading role in decarbonizing the world, especially in hard-to-abate industries such as transportation and shipping.

In the coming years, ports are expected to use their strategic position, infrastructure, and logistical know-how to reduce emissions for not only themselves, but also neighboring industries, ground transportation and shipping. Not only will they become an important hub for low carbon hydrogen, they could act as a clearing house to redistribute green hydrogen flows from seacoast to inland regions.

Obviously ports must decarbonize their own operations and handling equipment as part of that process. What’s more, flows of carbon, as part of the nascent industry of carbon capture, usage, and storage (CCUS), will also appear in the ports’ landscape to complete their set of tools in the fight against global warming.

Nevertheless, we believe that port hydrogen strategies will play a pivotal role in the coming years, especially in Europe, where tighter emission regulations and penalties are primarily concentrated. That said, where should port authorities, concessionaires and stakeholders place their emphasis? Who should they partner with? And what does the immediate future hold for port hydrogen policy?

This is what we know, according to new research conducted by Roland Berger.

Understanding port hydrogen dynamics

Before examining the most viable application of green hydrogen at ports, it’s helpful to summarize the advantages and disadvantages of hydrogen in general. For instance, hydrogen is the most abundant element on earth. It is also 100% sustainable and does not emit polluting gasses during combustion or production. And it is easily stored and versatile as a fuel.

That said, hydrogen is also more expensive to generate power, requires more energy than other fuels, and is highly flammable when not handled properly. That’s according to traditional standards, however. So with technological advances, those conditions are expected to improve moving forward.

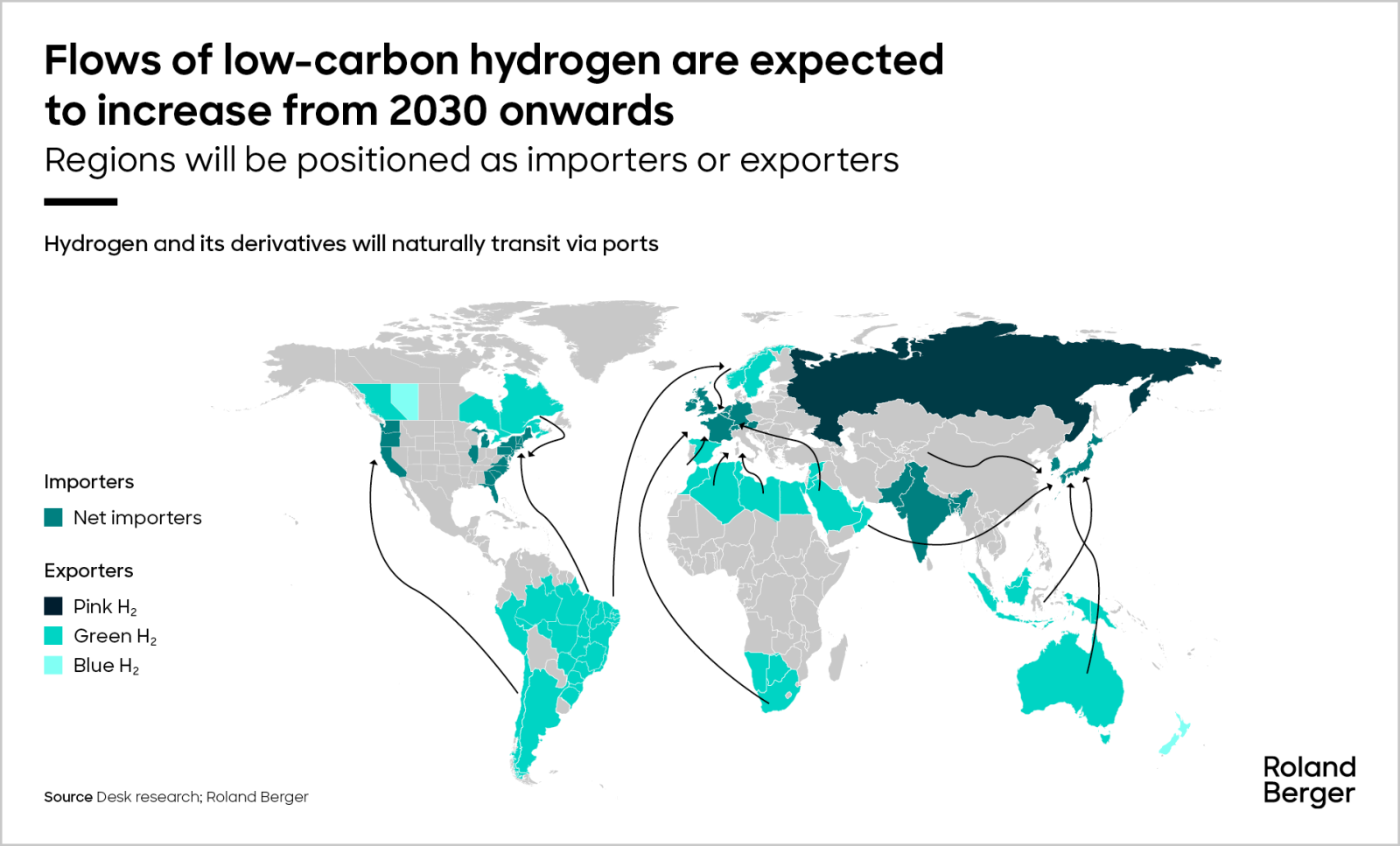

When compared to other alternative fuels, however, low carbon hydrogen is the leading option and experiencing a boom in market momentum, based on our latest research. Since most industry associations and regulators have already pledged for decarbonization—the EU for example is targeting 10 Mt of local H2 production and 10 Mt of H2 import by 2030—synthetic fuels, produced based on green hydrogen, like green methanol or green ammonia are key to decarbonizing the shipping industry and is expected to compete with biomethane as low carbon fuels. By 2050, we expect cross regions flows of H2 to fulfill the global demand for green H2 as follows (magnitude of 500 Mt p.a.):

"We expect a trend of re-regionalization of energy-intensive industries, gathering close to landing ports where green energy is abundantly available and potentially cheaper, and clean hydrogen clusters to be formed around ports where industries will gather."

Given the geographical position of those flows, ports will become the de facto cornerstone for clean hydrogen. Since they play the largest role in the global supply chain, ports will also play a considerable role in decarbonizing every industry it serves. That includes but is not limited to the global flow of goods and materials, ports being the host site for many industries, the starting point for many marine and road transportation efforts, and being well positioned near offshore wind power plants, crucial to produce clean hydrogen.

Given EU’s clean hydrogen import objectives, many ports are expected to become the import/export hub for low carbon hydrogen and redistribute those decarbonized gains from seacoast to inland regions. Such flows are expected under various forms: liquid hydrogen, ammonia and liquid organic hydrogen carriers (LOHC). After all, shipments of these sources started in some European ports as early as last year, namely Germany, Spain, Rotterdam, and Amsterdam.

In addition, ports must decarbonize their own operations in the process (handling and operations equipment chief among them) and can leverage clean hydrogen for this purpose.

Since shipping has turned into a top priority for global regulators (i.e. International Maritime Organization wants to cut 50% of their carbon emissions by 2050), immediate focus will be paid to shipping efforts. For now, low carbon and its derivatives (methanol, ammonia) stand as the leading sustainable energy sources to decarbonize maritime transportation. Thus, ports are already strategically positioned to provide ships with the necessary clean energy and will need to update their bunkering infrastructure accordingly.

_large_image.png)

Overall, we expect a trend of re-regionalization of energy-intensive industries, gathering close to landing ports where green energy is abundantly available and potentially cheaper, and clean hydrogen clusters to be formed around ports where industries will gather.

Upcoming implications for port authorities or concessionaires

Given the mounting regulatory pressure, growing demand, and time required to upgrade infrastructures, now is the time for ports to embark on their hydrogen journey. But which strategy and ecosystem works best for any given port, especially those under different state policies?

After thorough review of the most viable hydrogen port archetypes, Roland Berger has identified four in particular that show the most promise:

- Integrated coastal H2 ecosystem with local production of H2 or H2 imports used to decarbonize port activities, industrials, nearby transport corridors, and bunkering H2-fueled ships (e.g., ammonia or methanol fueled ships). Large imported goods ports bordering the North Sea are expected to adopt this archetype (e.g. Rotterdam for imports, Sines for exports).

- Coastal H2-fueled industrial cluster with local production of H2 (but no H2 imports) used to decarbonize port's activities, industrials, and nearby transport corridors (e.g. Dunkirk).

- H2 bunkering hub with local production and storage of H2 solely aiming at bunkering ships. Existing hubs located on shipping routes, and with limited industrials nearby, are expected to develop this model (e.g. Algeciras in Spain, Fujairah in UAE).

- Decarbonized H2-fueled port with local production of H2 used to decarbonize port activities and bunker (rather small) H2-fueled ships. This model is expected for small to medium sized ports, with limited industrials and local maritime activities (no international shipping). Port of Valencia has already started its H2 journey with this model.

The good news is ports have several options. The bad news: which strategy is right for them? Hence, determining the right port architecture, along with H2 types and volumes, is paramount. Factors such as port location, shipping type, local or global demand, transportation access, onsite equipment, number of supply chain stakeholders, and business models will all determine which infrastructure is not only the most variable and effective, but also most profitable.

_image_caption_w1280.png?v=1687234)

Why Roland Berger?

Consequently, approaching the right technical, operational, financial, and consulting partners will be key in ensuring any given port’s successful adoption of green hydrogen. When considering your future port strategy, we hope you’ll consider Roland Berger and the more than 200 assignments we’ve completed around the New Hydrogen Economy since 2020, including those for major port operations in Europe, North American, and the Middle East.

That includes but is not limited to our recent partnership with a Spanish energy company to establish the first green H2 corridor between Rotterdam and Algeciras (Andalusia) to supply Northwest Europe with 4.6 Mt of green H2 by 2030 and 20 Mt by 2050. Our access to H2 stakeholders, supply chain players, regulators, and investors is a big reason for our selection in that and other hydrogen projects. But so is our expertise and market access to other global decarbonization projects, more than 50 Roland Berger partners specializing in low carbon energy and transportation, and proven tools and methods to implement winning hydrogen strategies.

With Roland Berger, port authorities or concessionaires can determine the right hydrogen architecture, industrial supply chain, and business model under their new role as a clean energy port. On top of that, ports can expand their clean energy journey towards broader adoption by the shipping and transportation industries. as well as future decarbonization efforts.

Thank you for considering us in this important endeavor. To learn more, please contact us today.

Sign up for our newsletter

Further readings

We also thank Erwan Gaudemer and Vladimir Cabanis for their valuable contribution to the study.