Explore key trends and winning strategies in the global natural gas market. Download our latest study for actionable insights.

The waste-to-energy imperative

By Yvonne Ruf

Your 2026 roadmap to maximizing value

The era of expansion is over: the future market is about optimizing what already exists, not building more. Europe’s Waste-to-Energy (WtE) sector stands at a strategic inflection point. With over 500 operational Waste-to-Energy plants forming the backbone of Europe's circular economy, the market, especially in Central Europe and Scandinavia, is on the verge of reaching maturity.

But maturity does not mean stagnation. As regulatory pressures intensify, consolidation accelerates and strategic acquisitions reshape ownership structures. At the same time, feedstock availability shrinks and aging assets demand attention. Against this backdrop, operators face a fundamental question: How do we extract maximum value from existing infrastructure in an increasingly competitive landscape?

A stable foundation facing fundamental change

Europe’s WtE landscape processes hundreds of millions of tons of residual waste every year through a diverse network of facilities. For example, Germany’s WtE landscape processes approximately 25 million tons of residual waste annually in a network of predominantly small-to-medium scale facilities, averaging 270,000 tons per year per line. Unlike markets built on massive centralized plants, as in the United Kingdom, the German decentralized model reflects the sector’s evolution. With 66% of plants under municipal ownership, public service mandates have historically shaped investment cycles and commercial strategies differently than in purely competitive markets.

The numbers tell a clear story: Over the next decade, the total addressable EPC market in the DACH region will reach EUR 12 billion. But this value will not come from new capacity. Germany expects only around two new plants, with approximately five scrap-and-rebuild projects on the horizon. Instead, 35% of market value will derive from component retrofits and 28% from recurring maintenance. The strategic shift is unmistakable – from building to optimizing. However, the exception is Eastern Europe, where markets like Poland and the Czech Republic are still in an early growth phase: Regulatory catalysts like landfill bans are only now arriving, triggering a new-build pipeline that sets this region apart from its western neighbors.

This transition comes precisely as operators face mounting pressure from multiple directions. The combination of regulatory escalation, feedstock volatility, and aging infrastructure creates a complex strategic puzzle. Those who master it will thrive; those who don't will watch margins erode.

Three forces reshaping competitive dynamics

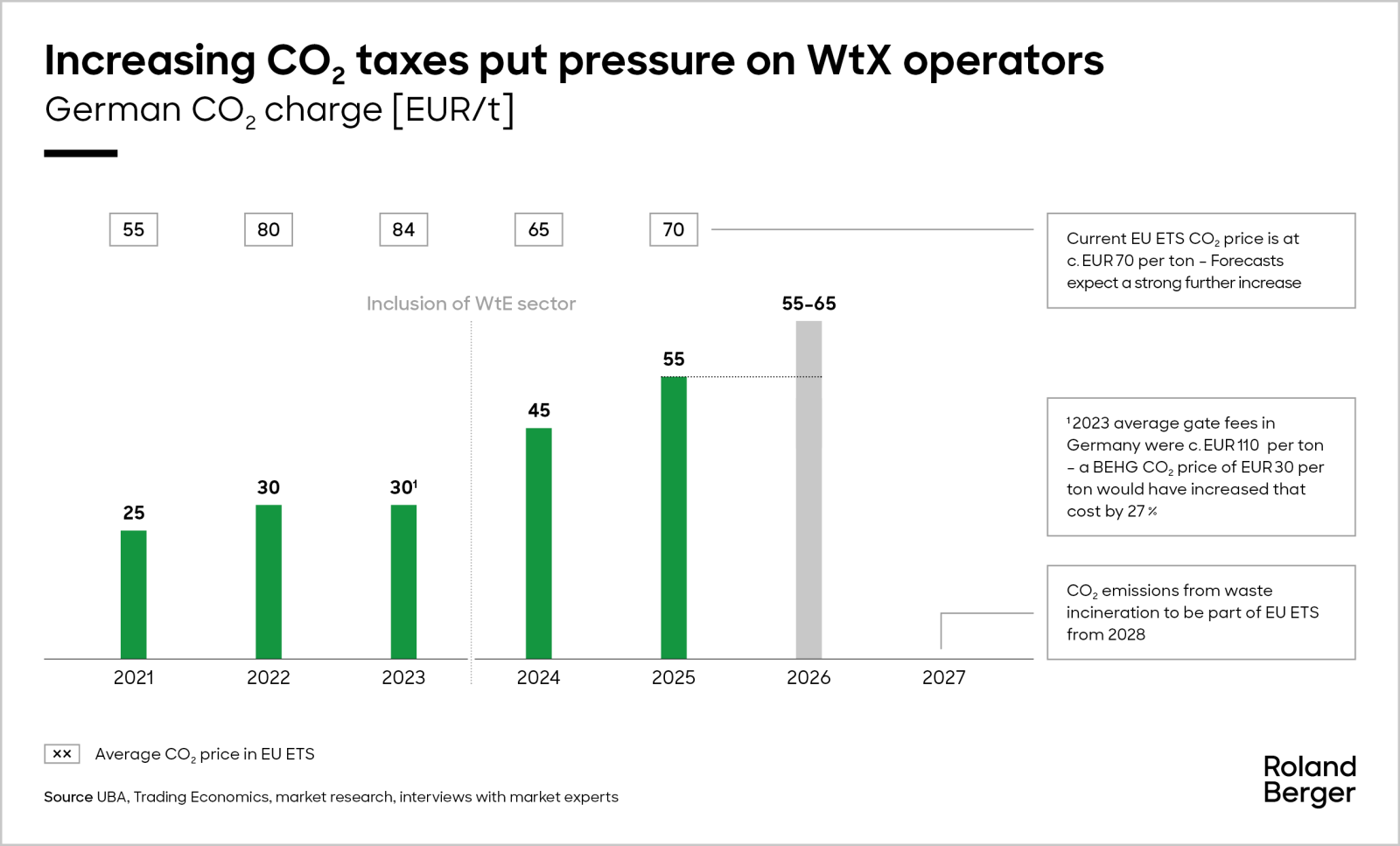

1) The regulatory imperative: From national tax to European market

Several European countries have introduced or expanded national carbon pricing mechanisms ahead of full EU-ETS integration. In Germany, the Fuel Emission Trading Act (BEHG), effective January 2024, introduced costs of EUR 55 per ton for fossil-derived CO2 emissions in 2025 as one prominent example. Many operators face immediate commercial risk as long-term contracts lack adequate cost pass-through clauses. But national schemes like BEHG represent only the opening act.

By 2028, WtE plants across the EU will likely enter the EU Emissions Trading System (EU-ETS). While this levels the playing field for e.g., German operators currently at a competitive disadvantage, it dramatically raises stakes industry-wide. Operators must choose: purchase high-volume CO2 allowances, invest in capital-intensive infrastructure like carbon capture, or fundamentally manage the carbon content of waste inflows. Mandatory monitoring, reporting, and verification requirements for plants above 20 MW took effect in January 2024, with final EU inclusion decisions expected by 2026.

The impact creates market segmentation. Public operators often benefit from cost-recovery models tied to municipal waste fees, allowing easier cost pass-through and reducing immediate financial exposure. Private operators lack these mechanisms, facing intense pressure to either absorb costs – directly impacting margins – or renegotiate contracts in highly competitive conditions. The era of treating emissions as externalities has definitively ended.

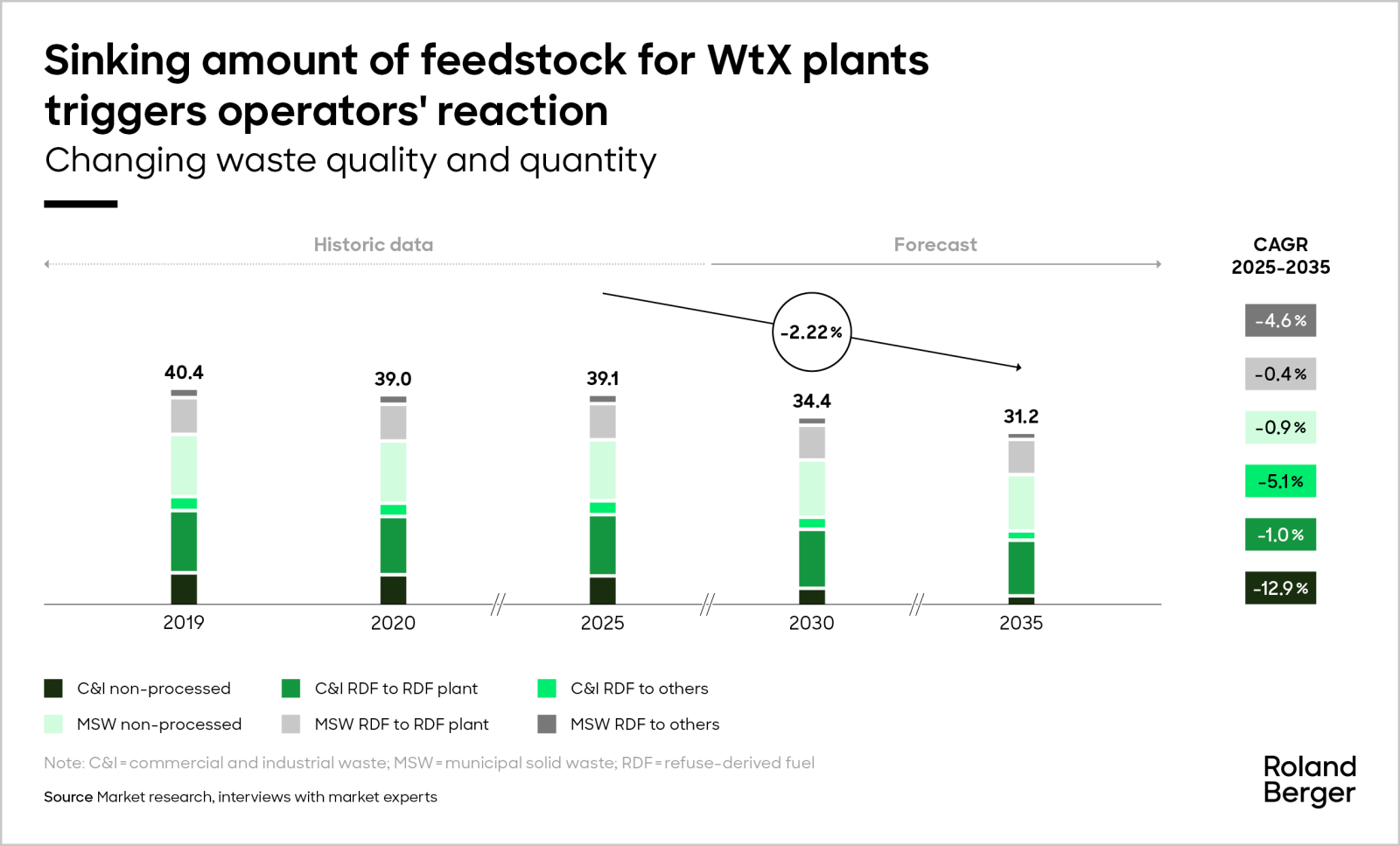

2) The feedstock dilemma: More waste, less fuel

While total waste generation from municipal solid waste and commercial/industrial sources will rise slightly due to economic growth, the volume available to WtE plants tells a different story. Non-recycled waste is expected to decline at -2.2% CAGR until 2035 as national and European recycling rates increase toward targets of 55% by 2030 and 65% by 2035.

This creates intensified competition for feedstock, forcing sophisticated, data-driven sourcing strategies. But quantity is only half the challenge. Quality volatility – high moisture content reducing efficiency, high chlorine content accelerating corrosion – makes active fuel management a top priority. Leading operators already implement enhanced supplier management through feedstock screening with gate cameras and license plate recognition to track supplier quality. Commercial steering links gate fees directly to pre-defined quality bands through bonus/malus systems.

The strategic goal is clear: ensuring that uniform plant utilization and stable combustion processes directly impact revenue. Feedstock inconsistency remains the primary cause of operational instability, increased wear on critical components like boilers, and reduced thermal efficiency – all eroding the bottom line.

"The WtE sector has entered one of its most exciting chapters: The real value lies not in the next plant you build, but in unlocking the full potential of the assets you already operate. Operators who embrace data-driven optimization and smarter contracts today will set the benchmark for the entire industry."

3) The reliability mandate: Aging assets, rising stakes

Europe’s mature asset base means many plants across the continent face increasing risk of unexpected technical failures and major retrofit requirements. The cost of unplanned downtime is severe – all revenue streams cease while high fixed costs continue. This makes maximizing plant availability and implementing robust asset lifecycle management a critical strategic priority.

Operators cannot afford reactive approaches. The transition from crisis management to predictive maintenance using data-driven insights represents a fundamental operational shift. Those who master this transition gain competitive advantage through higher availability, lower maintenance costs, and extended asset lifespans.

Three high-impact levers for immediate value creation

The strategic challenges are clear, but so are the opportunities. Three levers offer quantifiable, near-term value creation:

Lever 1: Gate fee and contract optimization represent the most direct revenue lever. Dynamic contracts using waste flow analytics, carbon content data, and regional market intelligence can deliver 5-10% uplift on average gate fee revenue per ton. This requires moving beyond static pricing to sophisticated models that reflect real-time market conditions and waste characteristics.

Lever 2: Capacity utilization offers 5-15% increases in annual throughput through two mechanisms: securing additional waste streams via optimized sourcing and implementing data-driven debottlenecking initiatives. Every additional ton processed leverages fixed costs more effectively, directly improving unit economics.

Lever 3: Maintenance and downtime reduction transitions operations from reactive repairs to predictive maintenance. Data-driven anticipation of failures minimizes costly unplanned shutdowns, increasing plant availability by 3-6% – translating to 11-22 additional operational days annually. Given the high cost of downtime, this lever delivers disproportionate bottom-line impact.

Beyond these primary levers, complementary value pools await. Energy sales optimization maximizes high-margin heat offtake and uses heat storage to capture peak price spreads in volatile power markets. By-product monetization strategies can transform bottom ash processing from cost center to revenue stream. Active CO2 taxation steering through waste stream management to optimize biogenic ratios directly reduces the carbon tax burden.

The path forward: Integration over isolation

Successfully navigating interconnected challenges requires integrated strategy, not siloed solutions. Our holistic framework addresses three critical dimensions simultaneously:

- Strategic advisory: Developing resilient asset strategies (newbuild vs. rebuild), performing individual strategic site assessments, and identifying market expansion opportunities.

- Commercial optimization: Designing dynamic gate fee models, optimizing energy sales contracts, and creating by-product monetization roadmaps.

- Technical & operational excellence: Leveraging advanced tools like digital twins, debottlenecking, and implementing predictive maintenance.

The winners in Europe’s evolving WtE market will be those who embrace these challenges with clear, data-driven strategies now. They will view 2026 not just as another year but as the critical decision point it represents – the moment when regulatory frameworks crystallize, feedstock competition intensifies, and asset strategies must be finalized.

For a diagnostic discussion assessing the specific potential within your assets and outlining a roadmap for value creation, our Waste-to-Energy experts are ready to help you navigate this critical transition.

Sign up for our newsletter

Sign up for our newsletter and get regular insights on newest publications related to Energy & Utilities.

Further readings

_person_320.png?v=1687234)