Explore the growing challenges and promising solutions in global waste management. Discover how population growth, consumption patterns, and regulatory initiatives shape the future of municipal solid waste. From regional disparities to the imperative of effective waste management, uncover insights into recycling innovations and investment opportunities. Join the journey towards a cleaner, more sustainable future.

A global perspective on Extended Producer Responsibility

By Dragos Popa

Smart regulation or stealth tax?

Extended Producer Responsibility (EPR) is a widely used policy tool under which producers pay fees that cover the environmental impact of their products throughout their lifecycle. In Europe and other developed regions, this helps close the gap between recovery costs and the market value of recyclable materials – and in so doing achieves recovery rates of above 80 percent in top-performing countries.

Globally, however, coverage remains limited , leaving municipalities to shoulder much of the burden. With the worldwide market for EPR projected to grow from around EUR 20-25 billion today to as much as EUR 120 billion by 2050, we take a look at how these systems work, what developments they are subject to, and where the key opportunities and risks lie.

How EPR works – and where it matters most

EPR systems function through material and financial flows that connect producers, operators, collectors and recyclers. Producers pay fees to EPR operators based on the weight of materials placed on the market, with rates that vary by country and material – typically ranging from EUR 100-500 per ton and averaging around EUR 150 in Europe. Operators then pay tariffs to collectors and recyclers, frequently higher for materials with lower recovery rates to ensure recycling remains viable. Recycled volumes count toward legal targets, with penalties for non-compliance often significantly exceeding the fees. Oversight and transparency are critical, as misreporting is widespread and operator costs, which usually account for five to 20 percent of revenues, can be inflated in monopoly situations.

Mandatory EPR systems were first developed in Europe for packaging and have gradually expanded to product categories with short to medium lifecycles, such as tires, electronic equipment, batteries and textiles. Today, these five segments dominate the global EPR market, each with distinct dynamics, levels of maturity and regional adoption.

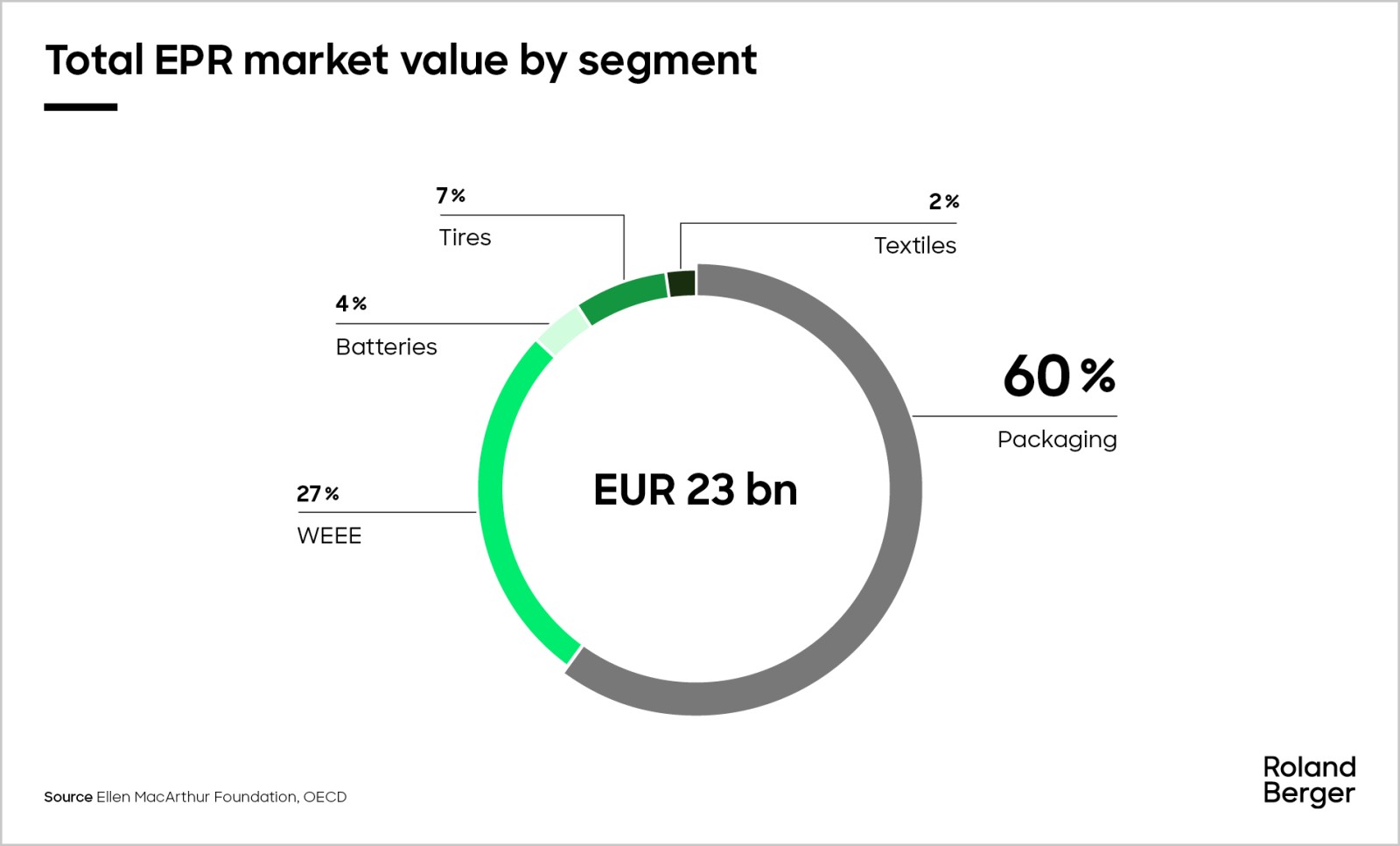

Packaging: The largest and most mature EPR segment worldwide

The packaging EPR market is worth an estimated EUR 14 billion, with Europe accounting for 80 percent. EU targets since 1994 have driven recycling rates to an average of 65 percent, with collection exceeding 70 percent. Outside Europe, coverage is around ten percent in Asia and still in its infancy in North and South America, Oceania and Africa.

Waste electrical and electronic equipment (WEEE): A major but underperforming segment

The global WEEE EPR market is valued at EUR 5-6 billion, with Europe accounting for 50 percent and Asia 30 percent of this total. Average collection rates remain modest at around 50 percent, partly due to hoarding and resale. Coverage is highest in Europe at 40 percent, followed by Oceania and South America, while North America and most of Asia lag behind.

Batteries: Small in value, but growing fast

The global battery EPR market is valued at around EUR 1 billion, reflecting recent regulatory focus. Coverage is roughly 30 percent, with collection rates at 50 percent of POM (put on market) volumes. Besides Japan and South Korea, China has had a mandatory scheme since 2016, while Europe updated its regulations in 2023. Elsewhere, coverage remains limited.

Tires: High collection rates where schemes exist

The total value of EPR for tires is estimated at around EUR 1.7 billion, with Asia and Europe accounting for approximately 75 percent. In Europe, collection rates exceed 90 percent, supported by take-back at the point of sale and strict anti-dumping laws. Outside Europe, coverage is significantly lower, with patchy adoption in Africa and the Americas.

Textiles: Still in its early stages

The textile EPR market is small, valued at around EUR 0.5 billion. France is the main pioneer, with Hungary, Latvia and California also introducing mandatory schemes. Broader adoption is expected from 2025, when the European Union will require separate textile collection.

"EPR is here to stay! In spite of the temporary cooldown in the global sustainability landscape, we strongly believe that mandatory EPR is one of the most successful policy instruments to drive material circularity."

Regional dynamics

Future development of EPR systems will be uneven across regions, reflecting differing regulatory priorities and enforcement capacity. Europe remains the global frontrunner, driven by strong legislation such as the Packaging and Packaging Waste Regulation (PPWR), though delays to broader sustainability laws may slow momentum in some countries. North America shows a split picture: Canadian provinces continue to expand and harmonize systems, while the United States faces stalled adoption as deregulation and postponements take hold. In South America, Brazil leads with the most comprehensive framework, and others such as Chile, Uruguay and Colombia are moving forward, albeit gradually.

In Asia, progress is steady: Japan, South Korea and Vietnam are at the forefront, India is strengthening its plastic waste regulation, and China is cautiously expanding coverage. Africa is still in the early stages, with South Africa leading and other countries experimenting with pilot schemes. Oceania is mostly driven by Australia, where implementation has begun across key segments, although enforcement and infrastructure are developing slowly. On a global level, EPR will thus remain the central tool for advancing circularity – but its impact will depend on effective governance, transparency and system maturity.

From cost center to catalyst

The EPR concept has proven effective in holding producers accountable for the environmental impact of their products. In mature systems, producer contributions cover the costs needed to achieve high levels of circularity. But elsewhere, progress has been limited – and EPR is often seen as a regulatory burden or stealth tax. With sustainability slipping down global agendas, it is now vital that EPR evolves from cost center to catalyst for meaningful impact.

Several catalyzing aspects are necessary to enable this evolution: globally or regionally aligned industry advocacy to drive mandatory EPR, for example as part of the Global Plastic Treaty, with alignment across the value chain a key success factor in high-performing systems; capacity-building through developing expertise at institutional or authority level via training, exchanges and best practice-sharing with successful systems; education that integrates circular economy principles into all levels of learning, from schools to universities; communication and engagement to raise awareness of circular economy topics at all levels, including consumers, through guidance on proper disposal, separate collection and waste reduction through reuse; and technology and innovation, with funding and incentives to continuously improve system performance.

Request the full PDF here

Register now to access the full study and explore how EPR advances circularity and transforms global industries. Furthermore, you get regular news and updates directly in your inbox.

Further readings

_person_320.png?v=1687234)