What the new normal could look like in construction

The German construction industry must act now to gear up for an uncertain future and be in a position to shape it actively

Looking at the impact of the coronavirus crisis on liquidity and profitability, the German construction sector is in a good position compared to other industries, and also other countries. We don't anticipate seeing the crisis hit companies in the construction trade until the first two quarters of 2021.

Economic impact of the Covid-19 pandemic and state of the construction industry

The effects of coronavirus restrictions are becoming increasingly apparent: The International Monetary Fund (IMF) forecasts that real gross domestic product (GDP) will shrink by around 3% worldwide, growing 5.9 percentage points less than the 2.9% growth we saw in 2019. That said, the effect on the construction industry will vary in the different regions of the globe. While the United States will see mass layoffs in the construction sector as in many other industries and building activity in southern Europe is anticipated to contract by 60-70%, China's economy, including the construction sector, is already largely back on track, with the data showing an improvement in the situation there since March/April.

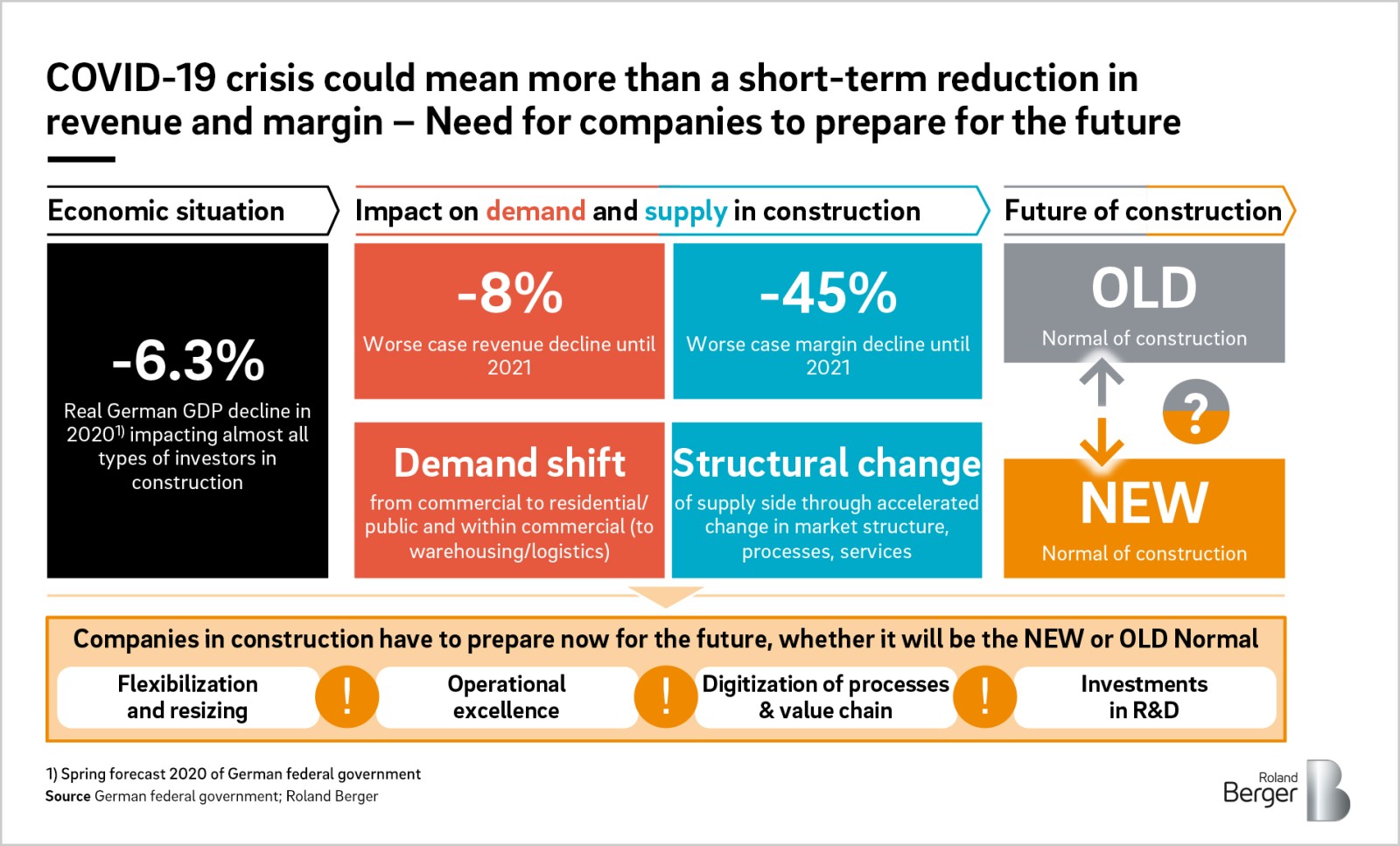

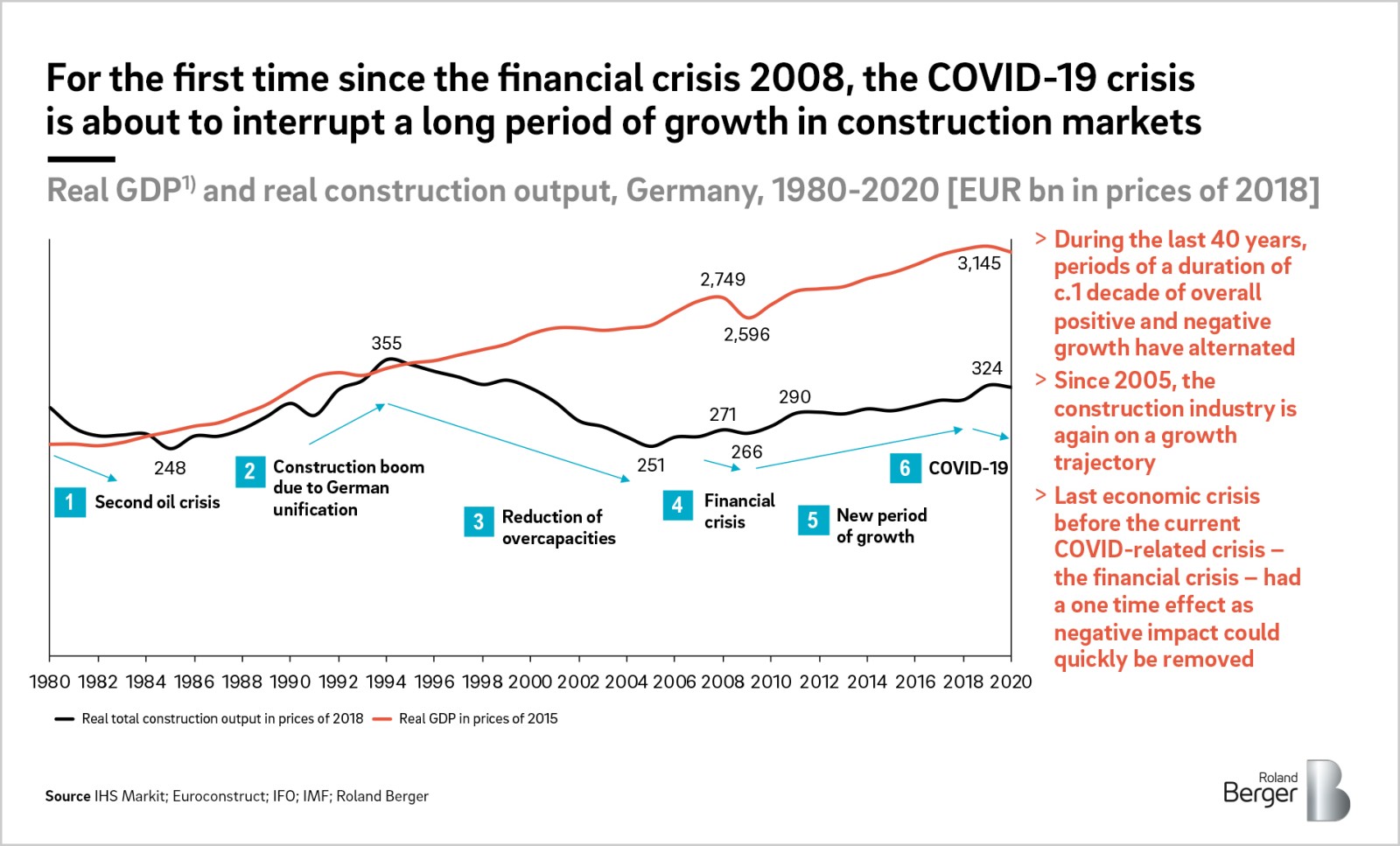

Germany is likely to feel the impact of the Covid-19 crisis even more keenly than the global economy as a whole. According to the German government's spring projection, Germany's economy will shrink by 6.3% in real terms in 2020 – coming in around 6.9 percentage points lower than the 2019 growth rate. The coronavirus crisis thus brings to an end more than a decade of economic growth (the last decline in real GDP came during the financial crisis in 2009). Covid-19 may turn out to be the German construction industry's fourth major crisis in the last 40 years, after the impact of the second oil crisis in the 1980s, the decade-long reduction of overcapacities that followed reunification and the brief decline that occurred during the financial crisis.

"Regardless of whether the construction industry moves into a new normal or reverts to the old normal, companies must act now and take the crisis as an opportunity to actively shape the future of the construction sector."

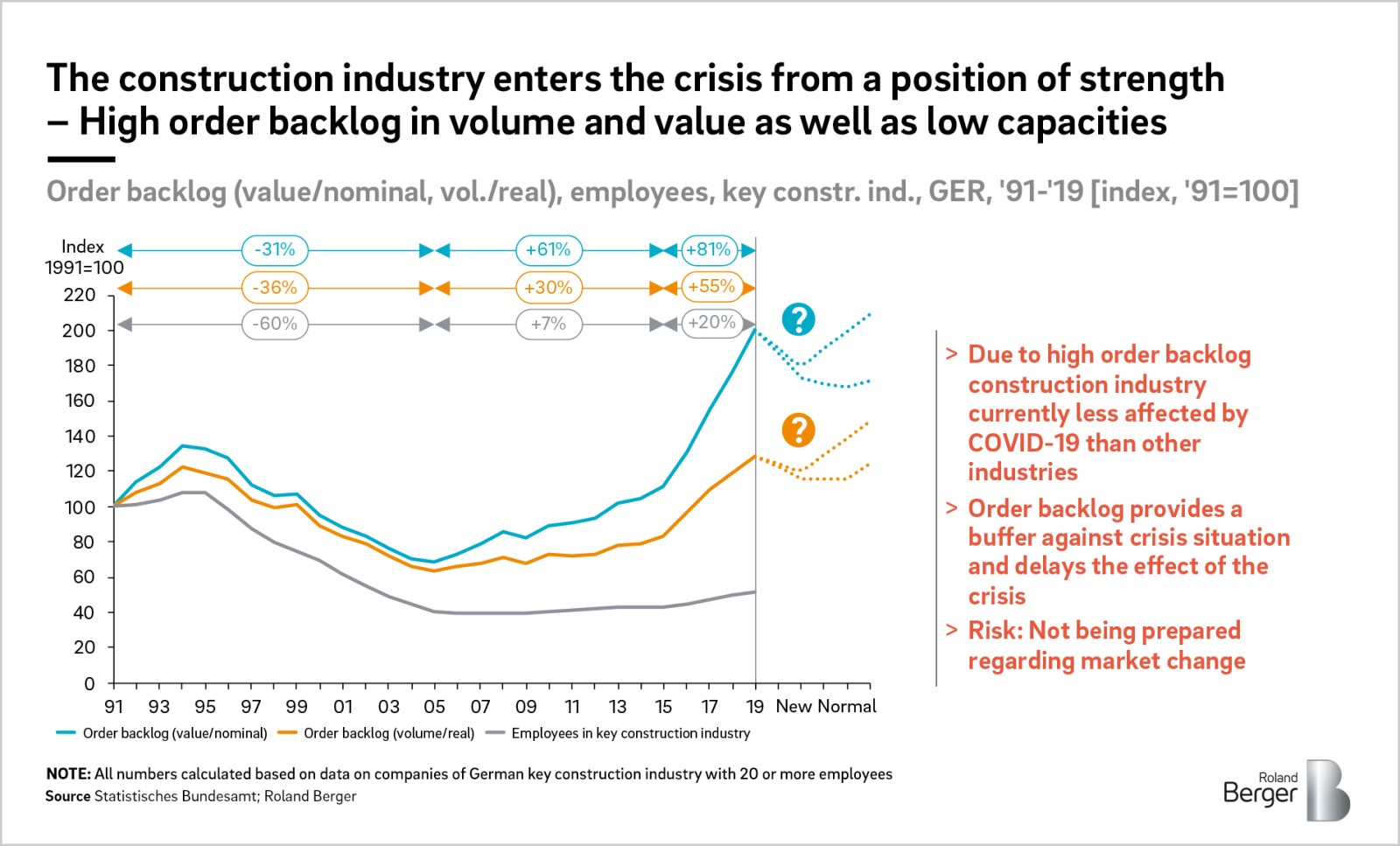

However, the current situation is not comparable with any of the earlier crises in the sector as the cause is fundamentally different and the construction industry is entering this crisis in a much stronger position, both in terms of the general economic conditions under which it's operating, such as low (mortgage) interest rates, and the circumstances within the sector itself. These include coming out of a growth phase spanning more than 10 years, low or even undercapacities (with the construction industry now employing about half as many people as it did in 1991) and an order backlog of a volume and value not seen in 30 years. But the German construction industry already began to show the first signs of a coronavirus slowdown in March 2020, when new orders in the sector were more than 7% down on the volume seen in March 2019.

8% real decline in revenues and 45% lower margins due to reduced or postponed construction spending as a result of the Covid-19 crisis

On the demand side, Germany's construction industry will primarily feel an indirect hit from the effect the coronavirus crisis is having on investor groups. Private household investments will likely be impacted by the increased level of (perceived) uncertainty around unemployment (+19% unemployment in April 2020 compared to April 2019) and short-time work (more than 10 million employees had been put on short-time work by the end of April). Politicians may be willing to use rent caps to support tenants affected by the coronavirus crisis. Behavioral changes such as regular working from home have the potential to make living in the countryside more attractive – but in most cases there is already sufficient accommodation available there.

In commercial construction, companies' demand for building work may decline due to the massive slump in sales and profits some firms are experiencing, a typical reaction to the coronavirus crisis being to completely cut all non-essential spending. Furthermore, the structure of demand may also change as a result of (permanent) changes in behavior: fewer hotels (as there will be fewer business/leisure trips), fewer offices (as there will be more remote working), less retail space coupled with increased demand for more warehouse/logistics space (as there will be more online shopping).

Public sector construction spending can be expected to suffer, mainly under the weight of the mounting debts faced by cities and local authorities who are responsible for the majority of such spending. Levels of debt were already high here and the situation is now being exacerbated by the loss of business tax revenues in the wake of the Covid-19 crisis. Economic stimulus programs – which tend to be linked to sustainability criteria – or any debt relief granted by federal or state governments to the local authorities would likely help stabilize construction spending on modern infrastructure (e.g. high-speed internet, intelligent building control in the context of the Internet of Things) and "green" public buildings. In order to meet this demand, a large proportion of construction companies will need to invest in expertise and equipment, in some cases substantially, as relatively few companies so far specialize in these segments.

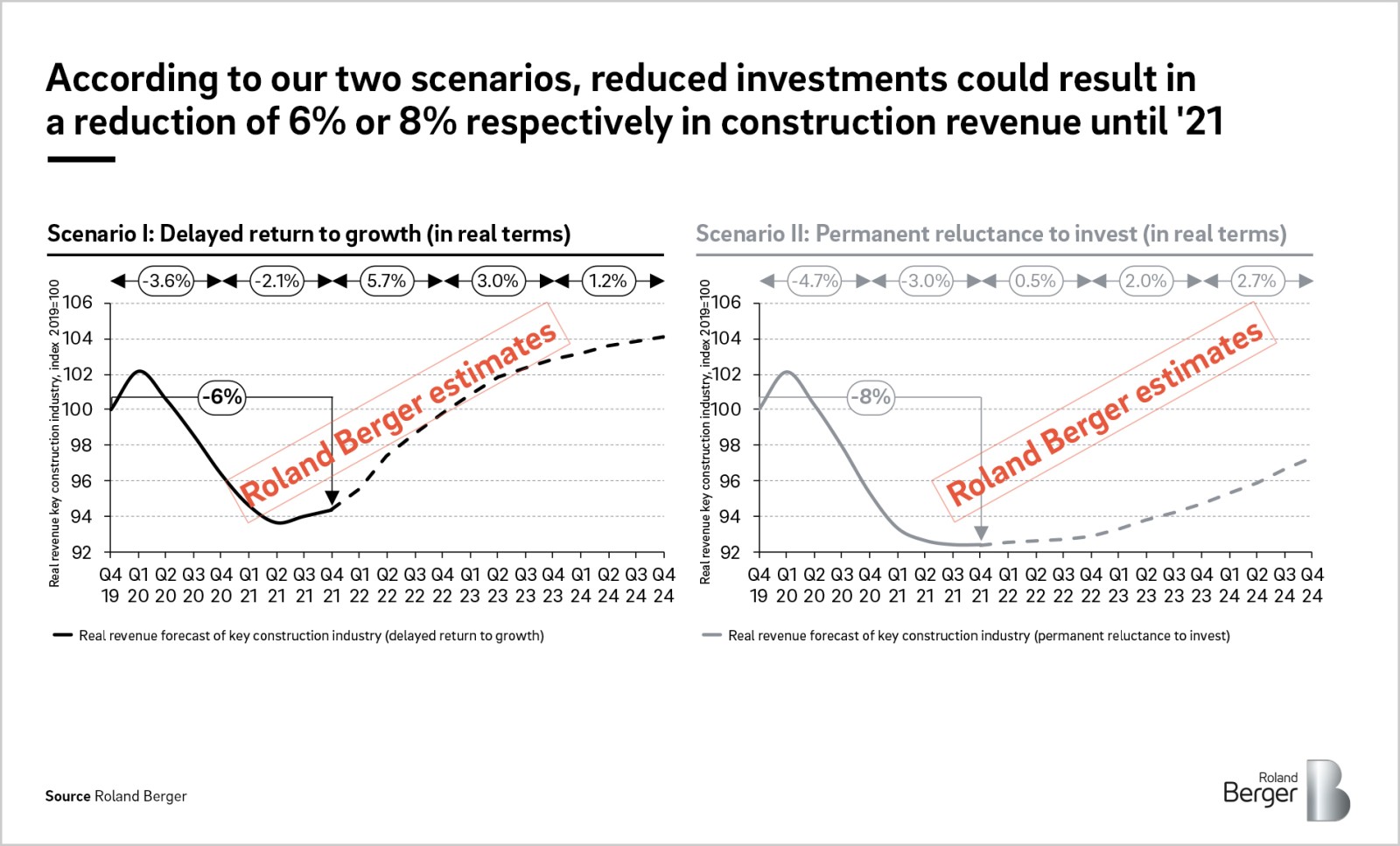

Against the backdrop of shrinking investments and the changing demand structure, Roland Berger has drawn up two scenarios for how the revenue trend could develop for construction companies. The scenarios are based on regression analysis of selected indicators combined with empirical values from past crises. The scenarios show that the construction industry will likely reach its nadir in the first or second quarter of 2021, somewhat later than the economy as a whole. At the end of 2021, real revenues may thus be 6% lower than at the end of 2019 in the base scenario (U-shaped recovery), and as much as 8% lower in the negative scenario (L-shaped recovery).

Given the nature of construction projects with their lengthy planning, approval, financing and execution phases, we believe that the full impact of the coronavirus crisis will be felt here later than in many other industries – not until the end of this year or early next year. So the sector will only get back to something approaching pre-crisis levels towards the end of 2022. We anticipate that the biggest losses will be driven by commercial construction, where a 6% drop in real terms could be seen in 2020 owing to the collapse in revenues – with some firms making zero sales during lockdown. This effect will likely continue into 2021, where a further decline of 2-3% is possible. Housing construction will likely feel the impact in the latter part of 2020 as households express lower demand for newbuild homes (about 2% lower in real terms in 2020). The crisis impact could extend into 2021 (-1% to -2% in 2021). If policymakers react with countermeasures as described above, offering suitable economic stimuli or debt relief programs for municipal authorities, public spending has the potential to exert a stabilizing influence, bringing growth rates of between 0% and 1% in real terms in the years 2020 and 2021.

Such dramatic revenue contractions will result in a similarly high drop in margins. While return on sales (in the construction industry average) rose almost continuously from 2.5% to 7.4% between 2001 and 2015, it has been stagnating or falling slightly ever since. According to our forecasts, the drop in revenue of 6% and 8% projected in the two scenarios would result in an additional margin reduction of -34% to 4.7% in 2021 in the base scenario and -45% to 3.9% in the negative scenario (on the assumption that 56% of costs fluctuate with revenues, such as costs for materials and external services; figures before additional cost-cutting measures).

The future of construction – will we see a new normal or go back to the old normal?

The question now is whether the coronavirus crisis will merely lead to a (short-term) decline in revenues and margins and the construction industry will then revert back to how it was pre-crisis, or whether current developments will accelerate in such a way as to result in a new normal for construction. If the construction sector really does move into a new normal, what will this future look like?

It's certainly possible that we'll see a change in the demand structure within the building sector – with the importance of commercial construction falling and the relevance of residential and public sector construction rising.

Specifically, there could be a reduction in travel activity resulting in lower demand for hotels, for example. This will affect business travel in particular, as things like virtual meetings have become established as the norm during the coronavirus crisis. The trend towards remote working could have a similar effect, additionally meaning that less office space would be required. Companies could permanently decide to spend less on investments that are not absolutely necessary (e.g. prestigious office buildings) and place a stronger focus on social or sustainable values.

People getting used to online shopping will lead to a shift away from retail towards more warehouse and logistics buildings.

Demand in residential construction is still strong at the moment, and financial support from the public sector could ease the burden on low-income households but this may also include a rent cap, which would depress profit margins on residential real estate and thus dampen (commercial) investment willingness.

On the supply side, we are likely to see companies doing more towards digitalizing their value chain (e.g. internal processes and go-to-market) and making their business more resilient. This includes construction site digitalization and supplier regionalization in a bid to make the supply chain more resistant to global shocks.

Sustainability may well turn out to be another focus topic for construction companies in the new normal – consolidating the circular economy, for example, or increased energy efficiency, reduced CO2 emissions and "green" products for a Green Deal.

In addition to this, new products and solutions that reduce the spread of disease could become more established on the market. The spectrum could range from antiviral HVAC systems to modified work/office furniture.

It's equally possible that the market structure may change. Large and well-funded companies have the potential to emerge from the crisis as the winners – perhaps by cheaply acquiring promising firms whose business is suffering in the crisis. This may enable them, among other things, to diversify geographically or achieve upstream/downstream integration along the value chain. By contrast, smaller tradesmen and construction firms as well as construction suppliers and distributors could disappear owing to a lack of financial firepower and a lower degree of diversification. The advancing pace of digitalization along the value chain could also put pressure on builders' merchants, as it would be easier for building materials producers to circumvent the classic three-tiered structure of the building materials market and sell their manufactured products directly.

Social distancing rules are becoming increasingly important as a result of the coronavirus pandemic, and the closed borders make it clear just how dependent the German construction industry is on workers from other EU countries. Both of these factors create restrictions for the way the sector can function now. Coupled with efforts to increase cost efficiency, the coronavirus crisis may accelerate the use of new construction technologies (such as industrial modular construction or IoT-based safety applications on construction sites).

Where necessary, new decision-makers are also being established, with the result that the marketing and sales approach is evolving more towards a one-stop shop solution.

Companies must act now

Irrespective of whether the construction industry moves into the new normal described above or returns to the old normal, companies in the sector must take action now to be able to shape their future successfully. They need to tackle this in three stages:

- To remain able to act during and immediately after the crisis, companies must secure sufficient liquidity and be capable of reacting fast to any changes that may occur. By now, companies should already have ensured that this is the case for their business.

- Construction industry players should be thinking about consistent digitalization along the value chain and ways to make their business flexible and adjust the scale of operations, as well as examining the possibility of strategic acquisitions, in order to meet the challenges of the coronavirus crisis and be able to take advantage of the resulting opportunities. Their aim must be to build an agile and powerful organization.

- Finally, if they want to adapt to the new normal, players must focus on the green transformation, together with regionalization and flexibilization along the value chain, and increased investment in research and development as core elements of the transformation. This is the only way that construction companies can hope to position themselves successfully for the long-term future.

If you like to receive a more comprehensive analysis as a PDF, we will be happy to send it to you after the registration below.

This is an updated version of an article originally published on April 5, 2020.