Digital sales are set to transform the European used-car market. What are the key success factors?

The used-car market has always been heavily reliant on selling cars the old-fashioned way – face-to-face in a dealer’s forecourt. But digitalization is changing the way the industry does business, with more and more sales taking place online. In this report, we review the European used-car market, assess the impact of digital sales and outline key success factors relevant to all market players.

Digital sales usually offer a much smoother customer journey.

The European used-car (UC) market is thriving. While the coronavirus crisis has undoubtedly affected sales, the long-term outlook is good. The market is currently worth EUR 410 billion and is expected to grow at 3-4% a year in the near term.

Yet the industry has a problem. The process of buying a car remains relatively antiquated, as low margins and stiff competition mean retailers have little left over to invest in digital sales channels or business models. Most still rely on traditional methods, and this is holding the industry back. Fully online transactions promise to help overcome existing pain points in the customer journey.

"A digitally oriented business model that successfully integrates our six factors will ensure a competitive online business "

The UC market can be split into two segments: B2C (retail) and C2C. B2C represents 40% of volume, but 55% of value due to its domination in sales of recent vehicles (less than eight years old). This share is increasing, driven by private leasing penetration.

The recent-vehicles market, the main target of B2C players, represents 70% of the total UC market value. Following a drop in 2020 due to the Covid crisis, it should recover quickly and grow from EUR 290 billion to EUR 365 billion in 2025 (+4.5% p.a.).

The B2C trade is dominated by traditional physical dealers. Franchised dealers account for 66% of all UC transactions, and non-franchised dealers 33%. This leaves just a fraction of the market occupied by two new categories: online retailers, such as Aramis Group, and

new retailers

. The latter are established players upstream in the value chain (leasers, auction platforms etc) that have started to also directly retail their vehicles online. They include Leaseplan with CarNext and Arval with Autoselect.

Across Europe, the UC retail trade is highly fragmented. The top five local players in each country account for just a small cumulated market share (for example, 5% in Germany, 15% in Spain). This fragmentation, combined with the fact that most dealers have little investment capacity, mean their operations remain very traditional.

The shift to online sales

Buying a used car from a physical dealer is cumbersome. Many used-car websites offer a poor user experience, and customers often need to visit several different points of sale. The purchase process is also bumpy. Customers do not like the complexity and amount of paperwork involved, for example.

European used-car customers are increasingly turning to direct online purchases

As in many other retail sectors, online sales are helping to smooth UC customer journeys. They provide solutions for most of the pain points, including instant access to a wide range of vehicles, tailormade recommendations and less or even no paperwork.

While European used-car players are increasingly moving online, they still have a lot to do. Several pain points, such as paperwork for financing or same-day payment, have not yet been fully resolved and digitalized, and no player has yet built a trusted brand.

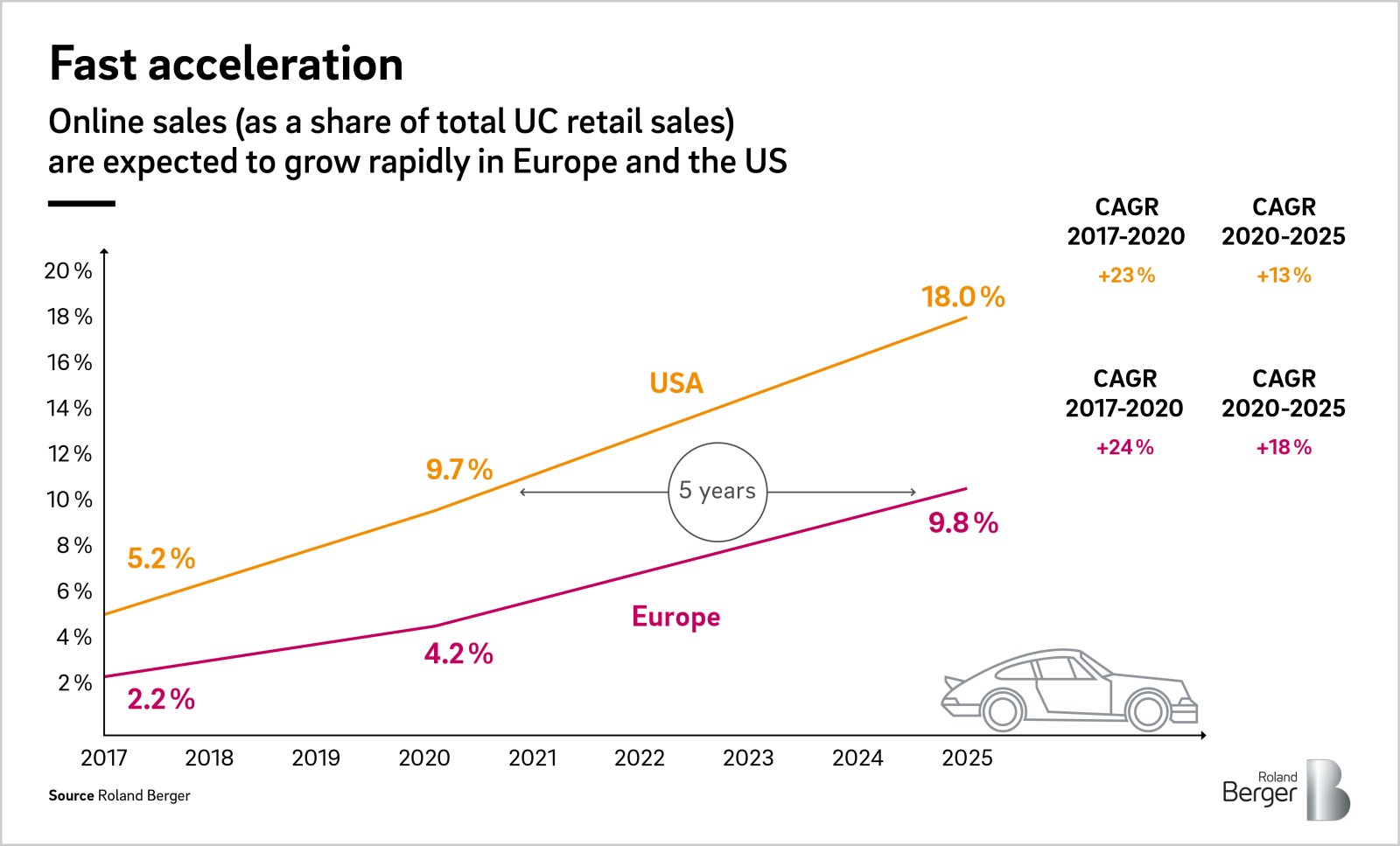

The situation is better in the US. There, the CAGR for overall online UC retail sales is forecast to almost double between 2020 and 2025, to 18%. We expect the European UC market to follow: online UC sales are forecast to double and make up 10% of the European B2C market by 2025.

Investors are convinced about the digital transformation of the used-car market and are prepared to make huge funds available – more than EUR 1 billion was invested in 2020.

The key factors behind a successful digital transformation

To be a successful online player, companies need a digitally oriented business model. We have identified six key success factors:

Build a strong and well-known brand: This will help to reassure and encourage potential buyers to make an online used-car purchase.

Adopt a data-driven business: Players should generate and collect in-house and external data from their website, then implement advanced data processing to enhance their sourcing/appraisal, logistics and refurbishment, and sales.

Combine online and physical locations: Physical points of pick-up and delivery are key for both brand awareness and cost optimization.

Set up advanced refurbishment centers: Refurbishment drives used-car quality. It should be done in-house as this enables differentiation from the competition.

Tightly control logistics flows: Close management of logistic flows, such as home deliveries, is key to offering cost effective, fast and reliable delivery and pick-up to end customers.

Ensure vehicle sourcing is efficient and diversified: To offer the right mix of vehicles at the best prices, players need to leverage multiple sourcing channels, such as customer trade-ins, auctions and leasing companies.

A digitally oriented business model that successfully integrates our six factors will ensure a competitive online business. They represent entry barriers that require significant investment in the short term, but will drive-up profitability – and consolidation – in the longer term. Players must move fast to adopt them, and identify the right investments to exploit the coming boom in online sales.

Study

Click and drive: How to ride the boom in online used-car sales

Digital sales are set to transform the European used car retail market. Roland Berger outlines the key factors behind a successful digital transformation

![{[downloads[language].preview]}](https://www.rolandberger.com/publications/publication_image/roland_berger_726_used_car_market_coverasset_download_preview.jpg)