Recent advances have made this model viable at banking scale. Improvements in blockchain performance mean transactions can now be executed for fractions of a cent and settled within seconds. This enables production‑grade use cases across interbranch settlement, interbank transfers, cross-border payment, loans, trade finance and escrow without replacing

core banking systems

wholesale.

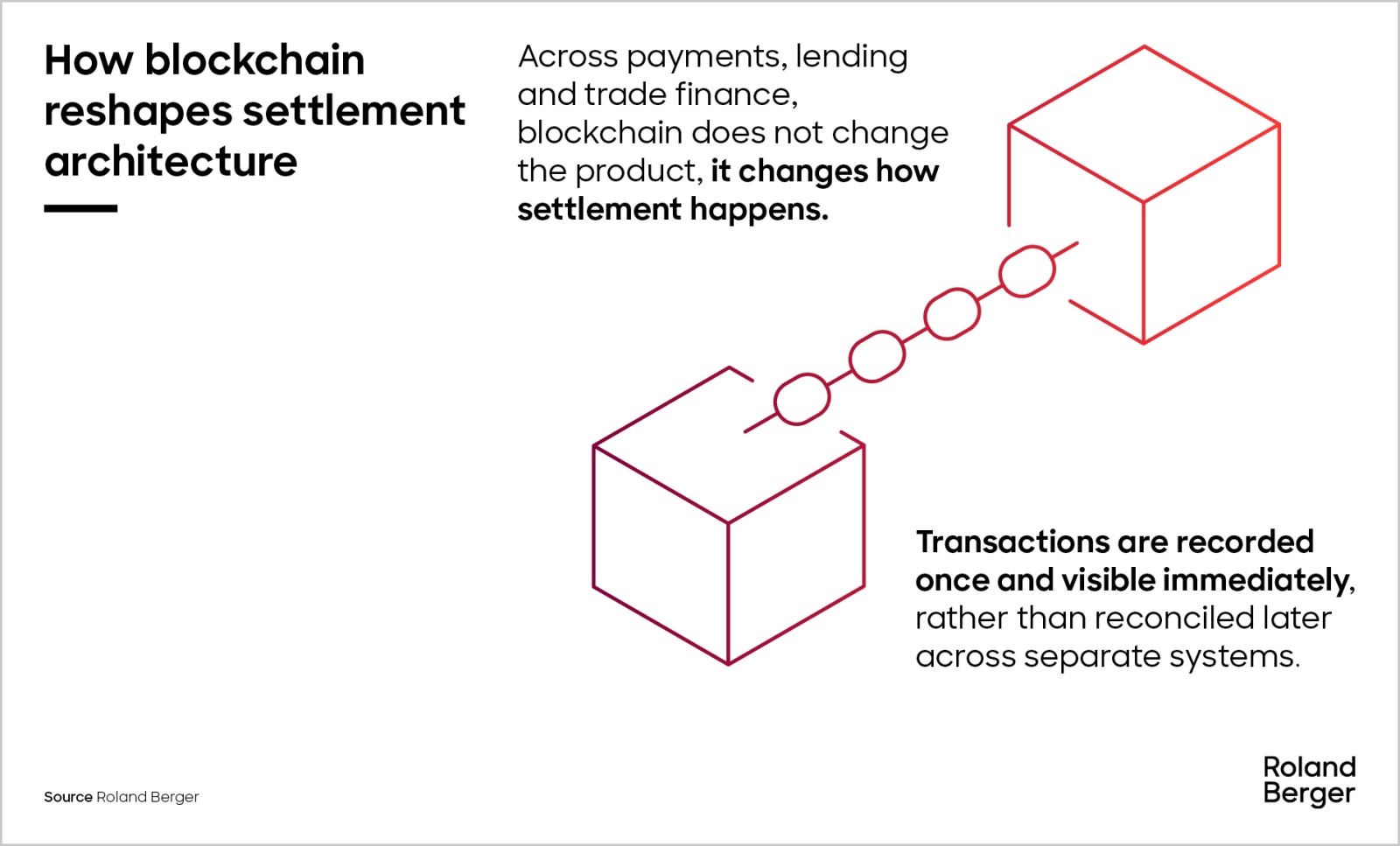

Banks are slowly starting to apply this model. Tokenized deposits allow real client balances to move continuously on‑chain within a regulated banking environment. Blockchains can compress interbank settlement from T+1 or T+2 to near real time. In lending, shared ledgers provide a single source of truth for balances and repayments. In trade finance and escrow, smart contracts automate verification and release of funds when predefined conditions are met.

Across these use cases, banking products remain unchanged – but settlement does change. Batch processing gives way to continuous synchronization.

Competitive pressure from stablecoins

The urgency to modernize settlement is reinforced by the rise of

stablecoins.

Mentions of stablecoins in SEC filings accelerated sharply through 2025, reflecting growing institutional attention. Industry estimates suggest that up to USD 6.6 trillion in bank deposits could be at risk if stablecoin adoption accelerates. Stablecoin‑based transfers can be completed in under a minute and at substantially lower cost than conventional wire transfers.

Tokenized deposits could offer banks a strategic response: delivering blockchain‑based programmability and near‑instant settlement while keeping funds within the regulated banking system and preserving deposit‑based lending capacity.

Turning blockchain into value: A playbook for banks

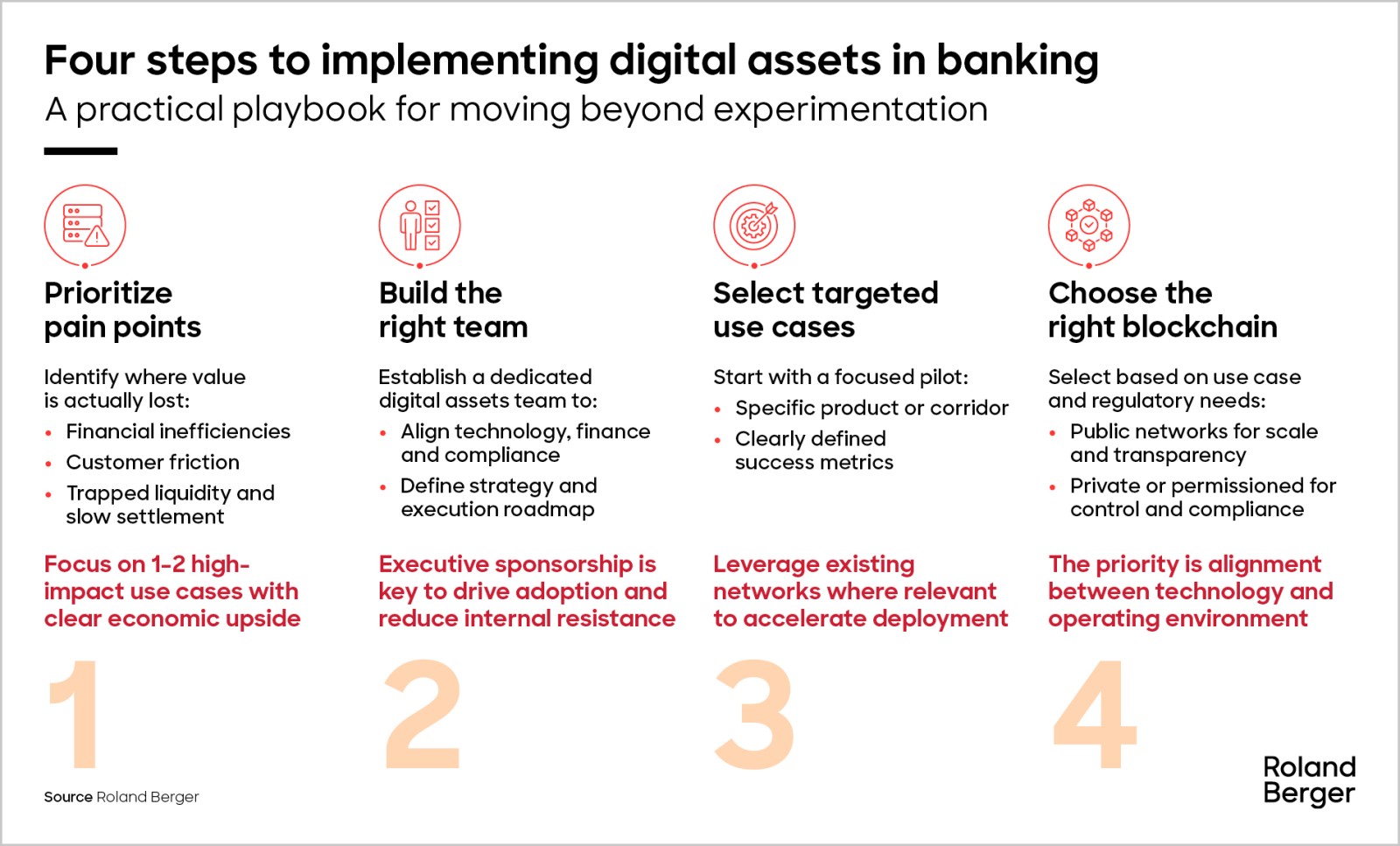

While pilots have demonstrated technical feasibility, widespread adoption remains limited. The constraint is no longer technology, but institutional execution.

A pragmatic path forward starts with prioritizing high‑impact pain points where settlement friction creates a clear economic cost. Banks should then establish a dedicated

digital assets capability

with senior sponsorship to bridge technology, finance and compliance. Rather than attempting a full infrastructure overhaul, targeted use cases – such as specific payment corridors or asset classes – allow measurable impact and controlled risk. Blockchain selection should follow regulatory and operational intent, balancing public, private and permissioned architectures, often within a multi‑chain approach.

![{[downloads[language].preview]}](https://www.rolandberger.com/publications/publication_image/roland_berger_26_2108_me_blockchainforbanks_cover_download_preview.jpg)