The market for Regional Air Mobility can become an attractive market soon. Learn more about our market analysis and predictions.

Cargo drones: A potential gamechanger in the logistics industry

By Stephan Baur

The market, challenges and recommendations

In the past few decades, drones have received significant attention from industry players, investors and governments alike. Unmanned aerial vehicles (UAVs) are highly versatile, serving multiple areas of application. In agriculture, for example, they are used to assess crop needs, such as irrigation and nutrients, as well as in crop spraying and tracking livestock. Other areas of application include archaeology, meteorology, mining and construction, environmental monitoring, cargo and logistics, defense and security, and conservation. Drone size tends to dictate application. Lighter drones are useful in filmmaking, consumer entertainment, tourism and sport, for instance, while heavier drones are being developed to transport passengers. The latter evolved from their smaller, lighter siblings. Today, the entire spectrum of machines is known as advanced air mobility (AAM).

The drone economy: Where do UAVs fit in?

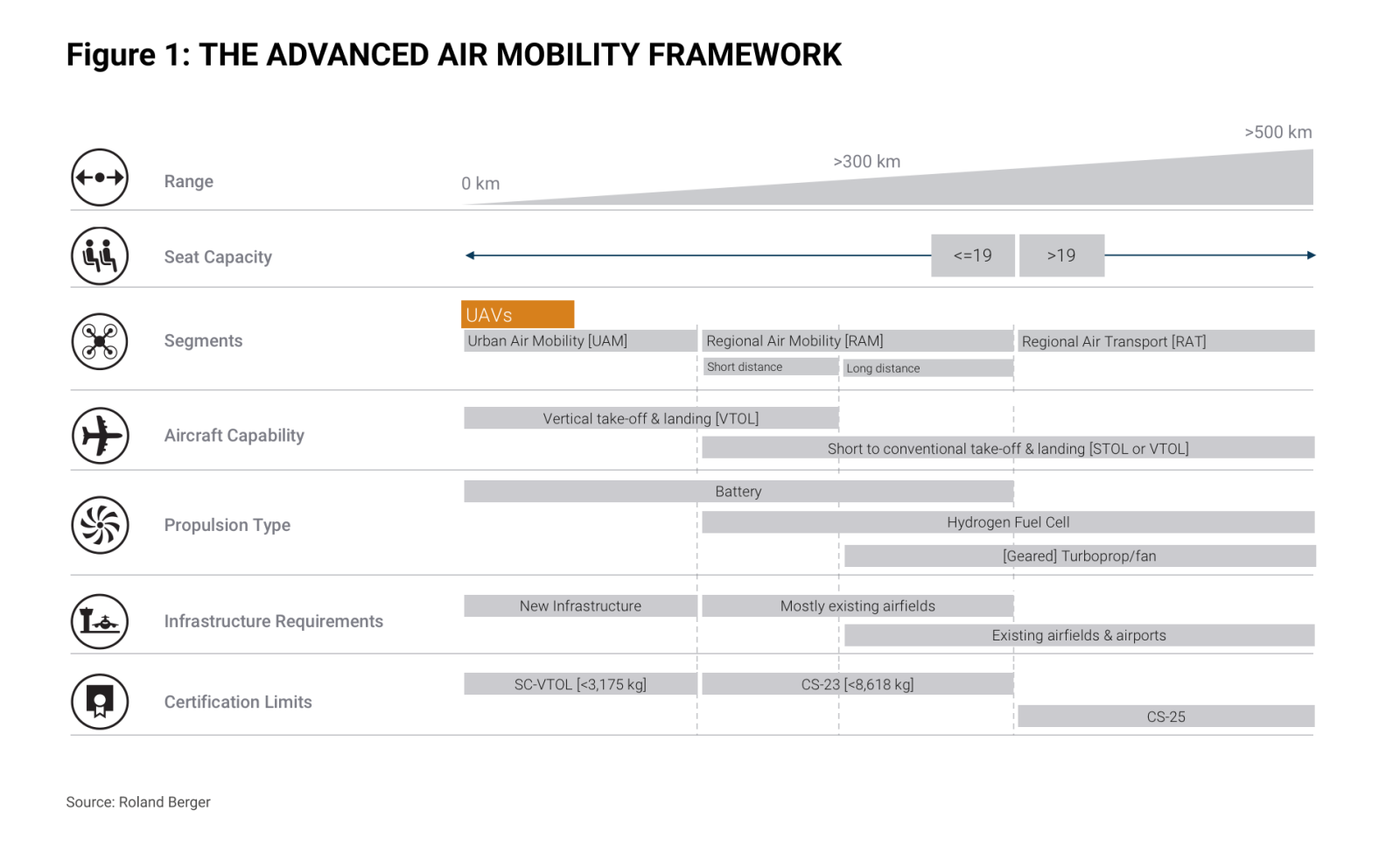

Given the rapid expansion of drone technology applications in recent years, Roland Berger believes it is useful to provide a definition and conceptualization of the overall drone economy. As such, we developed our 'Advanced Air Mobility Framework'. This shows UAVs position in the drone economy, as well as the applications and technologies they have spawned. In this article we will focus solely on the UAV subset of cargo drones for commercial purposes. As other applications are not considered, we use the term cargo drones interchangeably with UAVs.

Cargo drones: Key applications

Cargo drones come in small, mid-, and large sizes, with different performance capabilities (for example, regarding maximum payload and range). They are typically equipped with powerful sensors and next-generation software, and can be classified into four different delivery categories:

- Hub-to-hub, intra-firm warehouse deliveries (mainly short-distances): Here the drone will deliver industrial goods or products to a pre-defined delivery hub located within the firm’s premises, at an adjacent warehouse, or within a warehouse. The service is performed purely for internal process optimization and efficiency gains. Users include Amazon.

- Last-mile supply chain delivery (short- to medium distances): This service involves the drone delivering goods or industrial products to a nearby B2B customer or partner. The drone departs from either the firm’s premises or a conventional delivery truck. The solution is especially attractive in rural areas where delivery trucks need to serve many locations, leading to longer lead times. The drone can mitigate lead times and improve the overall cost structure of the service.

- Truck and ship loading/offloading (short- to medium distances): Here the drone performs the loading and offloading of trucks or ships, with follow-on distribution to warehouses, pallets or nearby industrial customers. The service could prove to be an attractive solution, especially in highly congested areas, as the drone can move goods directly from the terminal to a nearby distribution warehouse or similar location. Harbors, with their adjacent industrial areas, are a prime setting for the service.

- Intra- and intercity delivery (long distances): In this use case, drones move goods from a firm's premises in one city to another city, or within a larger metropolitan area (intra-city). This area of application is still in its infancy due to current range limitations, economics and regulatory hurdles. But the service could prove to be a game-changer for the cargo industry.

Market drivers: The disruptive forces behind the rise of cargo drones

Drone technology was largely driven by the defense industry in the 20th century. Only since the early 2000s have drones steadily established themselves in private and industrial environments, with a strong acceleration of growth at the beginning of the 2010s. This was mainly due to the falling cost of electronic components, such as lithium-ion battery packs, and the development of autonomous and artificial intelligence (AI) technology. Below we look at why these disruptive forces have made the use of drones economically viable, and attractive for market participants.

Lithium-ion batteries

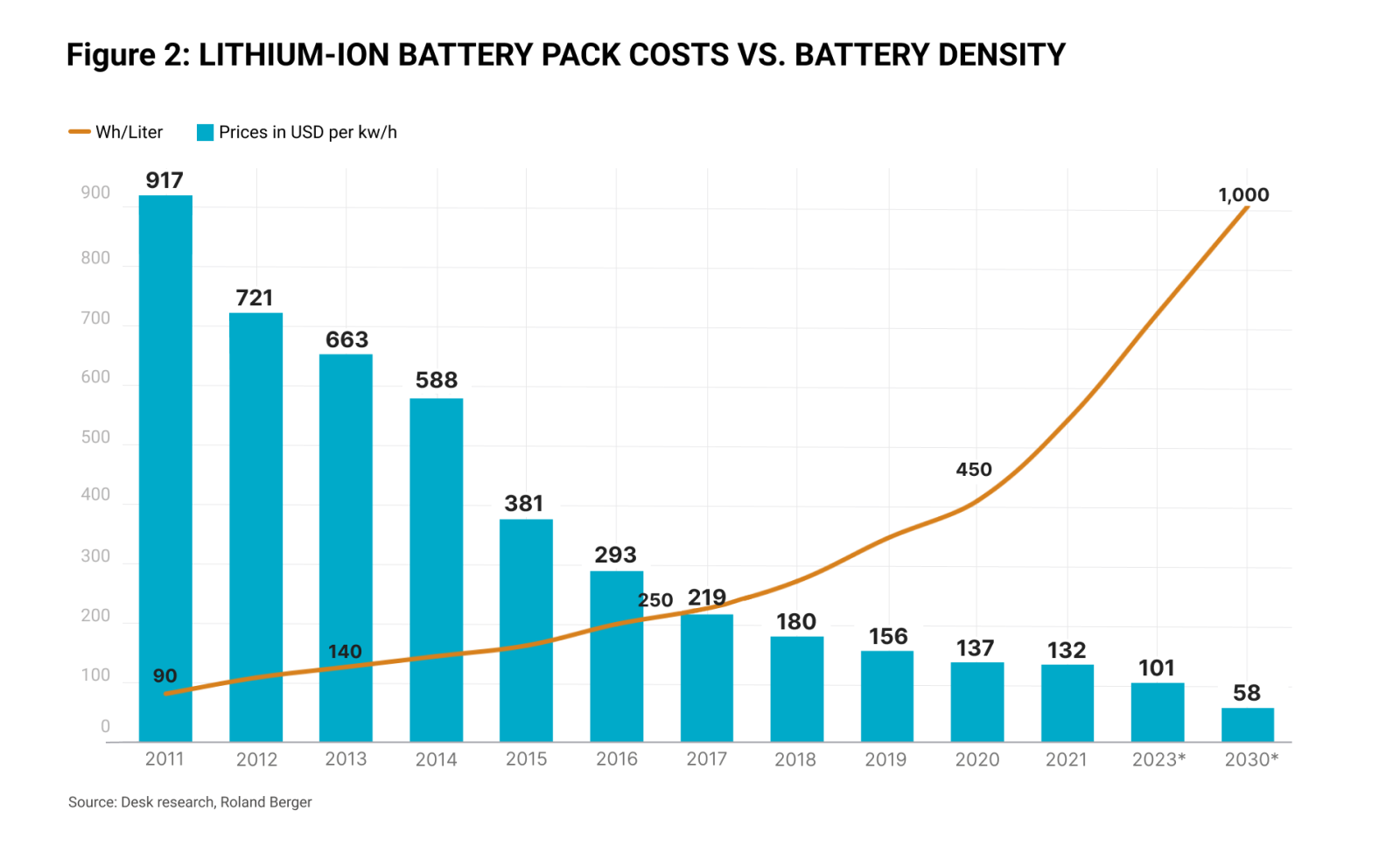

The falling price of lithium-ion batteries has helped to optimize drone cost and performance. And just as costs have fallen, battery densities have increased. It is thought that densities are improving by almost 10% a year, leading to lighter, more powerful batteries and smaller drones with a higher lifting capability. This is resulting in more attractive use cases, especially for cargo drones, which could now be used within warehouses, for example.

The cargo drone market also provides a perfect testbed for battery use in other applications. Batteries are a key component of technology validation, and once tested, can be transferred into other markets, such as the electric vehicle or passenger drone market. The rapid improvements in battery technology will allow drones to fly farther for longer, leading to many new use cases and applications, and unlocking untapped value for the drone industry.

Autonomous and artificial intelligence technologies

The progression and acceleration of autonomous and AI technologies (sense & avoid systems, cloud computing etc.) have changed the game in the drone industry. The two complement each other. Autonomous drones can gather information on their surroundings, process this data, interpret it and act on it without human intervention. While data collection is done via electronic components, such as sensors, it is AI that decides and controls the response to the data. This ability to link and interpret data from different sensors is making the drones smarter, giving them the ability to better understand and act on their environment themselves.

The rise in these technology domains opens new areas of applications and will not only lower the cost of cargo deliveries and improve delivery times, but also be a significant contributor to our economy. The equation is simple: the more drone functions become autonomous and intelligent, the greater the benefits and efficiencies will be. In addition, as attractive cargo drone applications emerge, a promising, large market develops. This raises the interest of investors.

Growth and investment: A strong and growing market with huge potential

The cargo drone market is projected to grow from USD 534 million in 2022 to USD 17.9 billion by 2030, with a CAGR of 55.1% in that period. This growth can be attributed to the rise in demand for on-site, on-time industrial delivery and emergency supplies, as well as a significant change in the regulatory framework that enables the operation of autonomous drones beyond visual line of sight. The continued development of disruptive technologies, especially autonomous and artificial intelligence, will further contribute to the strong growth.

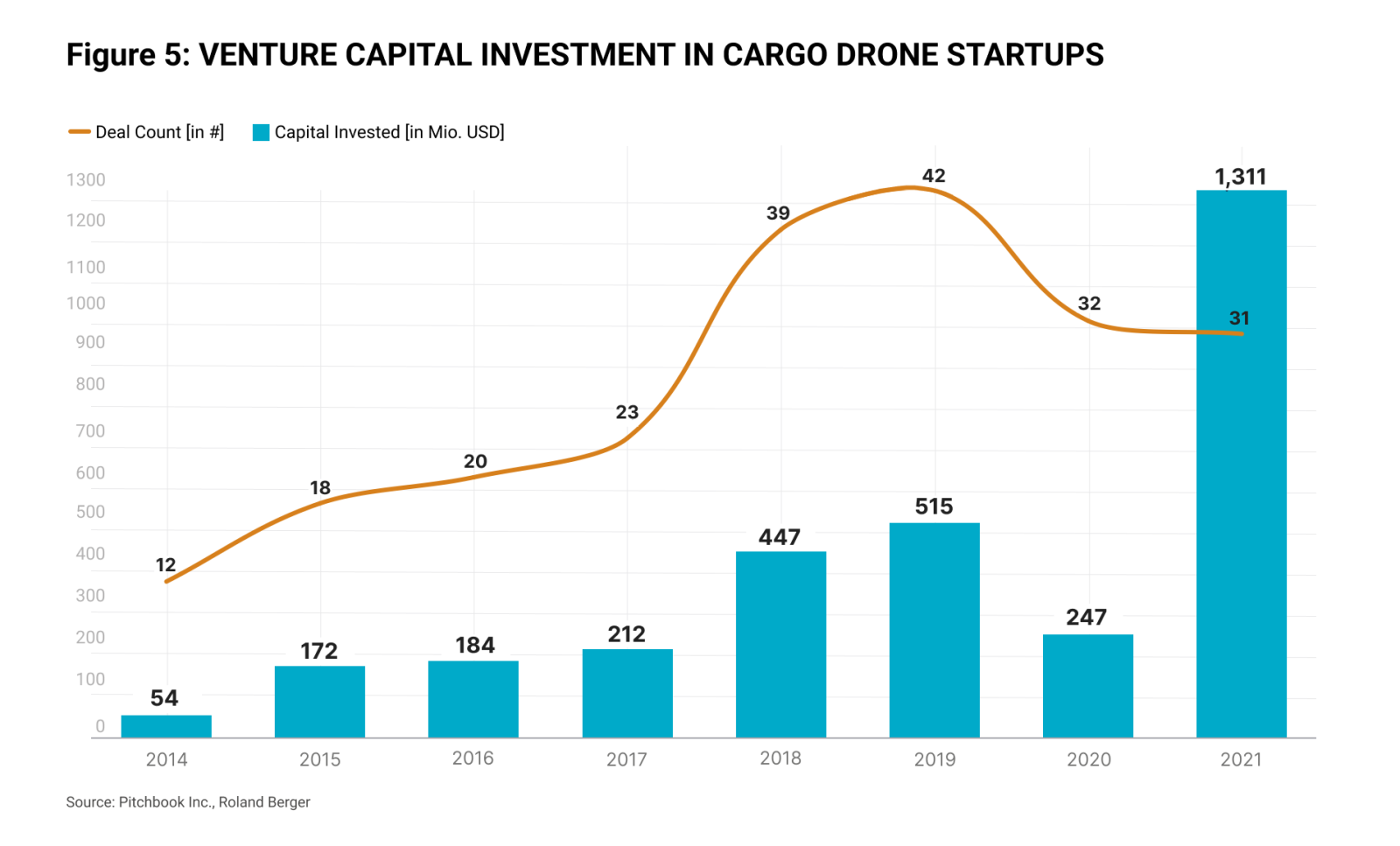

This growth has attracted investors, with venture capital (VC) rising continuously in recent years. VC funding in cargo drone startups, both in terms of deal frequency and dollar value, initially picked up pace in 2015. It then grew rapidly to reach a first major peak in 2019. After a dip in 2020, funding exploded in 2021 to levels exceeding USD 1 billion.

The decline in 2020 is related to the Covid-19 pandemic and with it the acceleration of many underlying trends. These include sustainability, which drove the investment hype in passenger drones and subsequently spilled over to the cargo segment. The number of VC deals in 2020 also fell from its 2019 peak, meaning Covid-19 had a direct impact on investor sentiment in this AAM sub-segment. Even in 2021, with its record levels of investment, deal size remained relatively stable and did not recover. This could be a case of investors betting heavily on the most promising players, a theory borne out by figures showing how the share of deals per VC stage has changed.

A look at these figures shows that the share of angel and seed deals is currently in decline, while both early and late stage deals are growing in relevance, now accounting for more than 75% of all deals. What does this trend mean? It suggests that not many new startups are entering the industry, with investors instead shifting their focus towards a handful of well-known players. The technological advances of established players raise the bar for newcomers, especially in terms of upfront R&D costs and engineering and deep tech expertise.

Recommendations: Players must work together to overcome the industry’s challenges

For the cargo drone industry to fully develop, players must first focus on and address its constraints. In this section we outline areas of action.

Regulation

First, to fully unleash the game-changing potential drones offer, policymakers must establish a clear set of guidelines for their safe and efficient operation, especially BVLOS (beyond-visual-line-of-sight). For example, will there be rules and guidelines on how to navigate drones within designated air space? What technical standards (5G or other?) will be required for communications between drone operators – and how will communications be standardized?

Public acceptance

Second, in order to fully integrate drones into our daily lives and gain public acceptance, the industry needs clear guidance on the safe and practical flight of drones over people and their houses. Consideration must be given to visual and noise pollution, and solutions found. This is especially the case for cargo drones as their use mainly benefits companies rather than end customers.

Smart infrastructure (ATM/UTM)

Third, we need a smart, efficient “virtual infrastructure” (air traffic management and unmanned traffic management systems). Like the current highway or train systems, a network of communication and guidance systems for low-altitude airspace will be needed if the cargo industry is to reach its full potential.

Ecosystem

Finally, despite the challenges, it’s clear that cargo drones have a distinct value proposition. To overcome the hurdles to large-scale implementation, the development of a collaborative ecosystem will be key. This should include national authorities, infrastructure providers and leading players to ensure standards and scaling across the industry.

Conclusion: The future is bright for the cargo drone economy

Cargo drones have the potential to form a significant part of the logistics delivery network, expanding the flow of goods between distribution centers or business and production sites. However, the full potential of drones will only be realized when autonomous operations become commonplace, and AI is fully exploited. The recent developments outlined in this article indicate that the industry is on track, and a bright future awaits it. Now it's time to focus on addressing the existing challenges to enable large-scale implementation.

Sign up for our newsletter

Register now to receive regular insights into Aerospace & Defense topics.

Further readings