Today's aviation industry is responsible for 2-3% of human induced CO2 emissions, but unlike many other sectors, aviation does not currently have a technological solution to decarbonize. Emissions reduction roadmaps have been published in an attempt to tackle the problem. Roland Berger deconstructs the roadmaps, focusing on the levers they intend to utilize and their potential impact and additionally take a look on non-CO2 emissions.

Cleared for takeoff

By Gabriel Schillaci and Nikhil Sachdeva

For aviation, the journey to sustainability starts at the airport

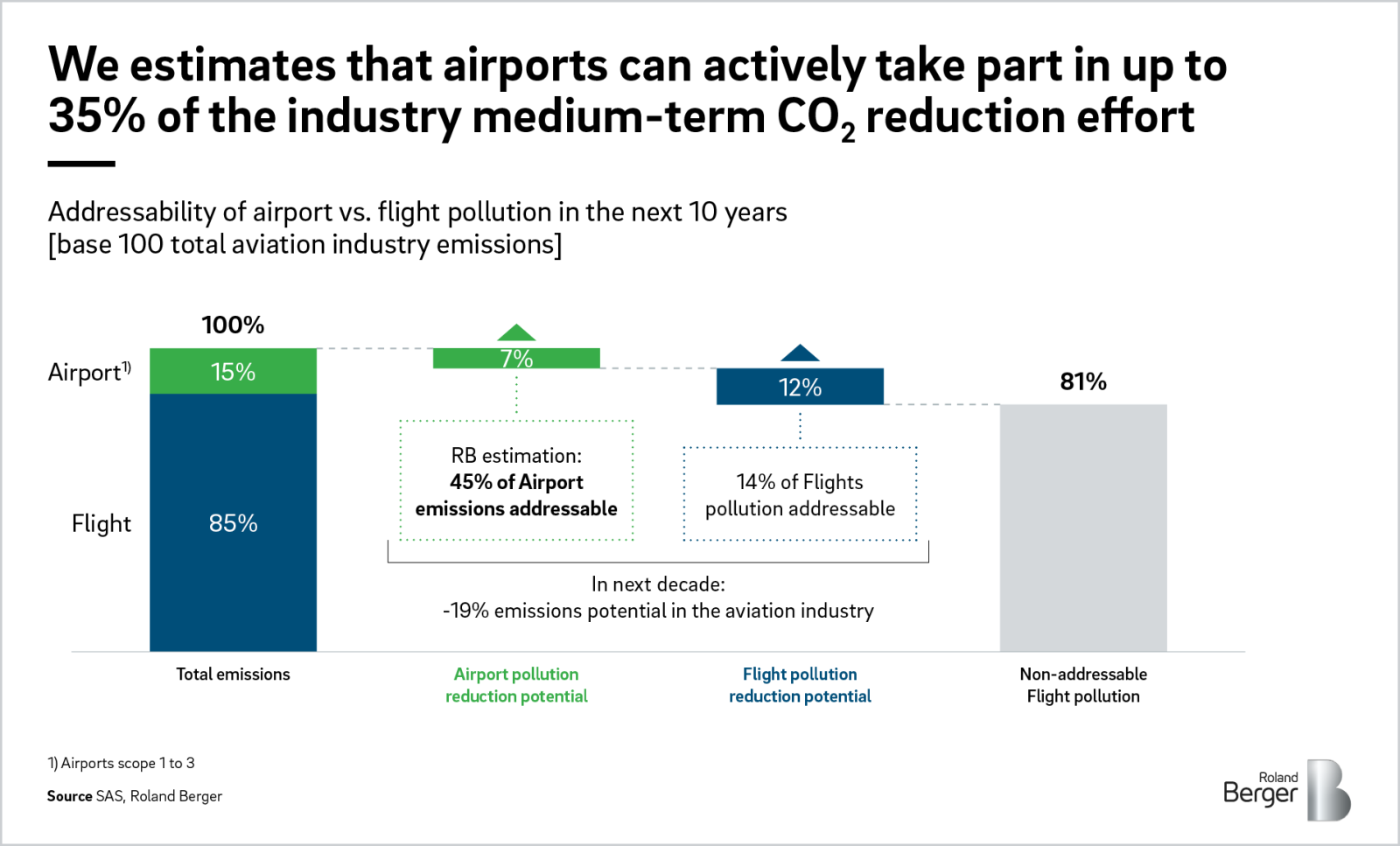

Making air transportation environmentally sustainable will require a joint effort by all players in the aviation industry ecosystem. While a large share of emissions is caused by flights, analysis by Roland Berger shows that as much as 35 percent of the CO2 that can be eliminated from the sector in the next decade will involve airports. Airports can play a critical role in enabling improved sustainability – and helping the aviation industry follow a roadmap to true zero.

Roland Berger estimates that over the next decade, reducing emissions from flights will account for 65 percent of the aviation industry's total emissions reduction . The remainder will relate to airports, including aviation emissions from taxiing, takeoff and approach. Given that the aviation industry as a whole is responsible for between three and six percent of global GHG (greenhouse gas) emissions, this means that emissions involving airports currently account for one to two percent of global emissions. Airports and the infrastructure that they provide are a key enabler of the transition as they provide the necessary infrastructure for airlines, ground handlers and other stakeholders.

"From now on, our will be not just to communicate a list of initiatives but to tell the market things they don't want to hear, to make stakeholders open their eyes to the urgency of change. The risk of the industry's competitiveness being weakened, of aviation being considered the worst performer, is just too high."

Our research suggests that a proactive approach to sustainability by airports could help improve not only the aviation industry's emissions but also its overall image. The reason? For many people, airports symbolize the entire air transportation journey. It is therefore vital that airports demonstrate the industry's concern about sustainability, showcasing specific environmental plans and overarching efforts to reduce emissions – particularly as passengers may be feeling some guilt at choosing a means of transportation responsible for large amounts of emissions.

Just as importantly, airports need to transform their business model in order to remain economically sustainable. If carbon costs rise, as is expected, the push for greener aviation will become even stronger. The aviation industry may find itself squeezed for financing as sustainability funds gain momentum. In Europe alone, "green funds" now hold over EUR 4 trillion in assets, representing 42 percent of the institutional investor market – and these funds are keen to have a positive ecological impact on the business models of the assets they acquire or finance.

These issues are no secret to airport operators, of course. A rapidly growing number of airports have launched ESG (environmental, social and governance) plans in response to concerns voiced by passengers and investors, as well as pressure from regulators. In 2010, for instance, just 17 airports were enrolled in the Airports Council International's Airport Carbon Accreditation; their number has grown to 304 today. Some 75 of those airports have reached Airport Carbon Accreditation Stage 3+, meaning that they have committed to offsetting residual carbon emissions for Scope 1 emissions (those owned and controlled by the airport operator) and Scope 2 emissions (those created by the off-site generation of energy that is then purchased by the airport operator), and also committed to mapping a stakeholder engagement plan for Scope 3 emissions (those owned and controlled by airport tenants and other stakeholders).

Passenger concerns

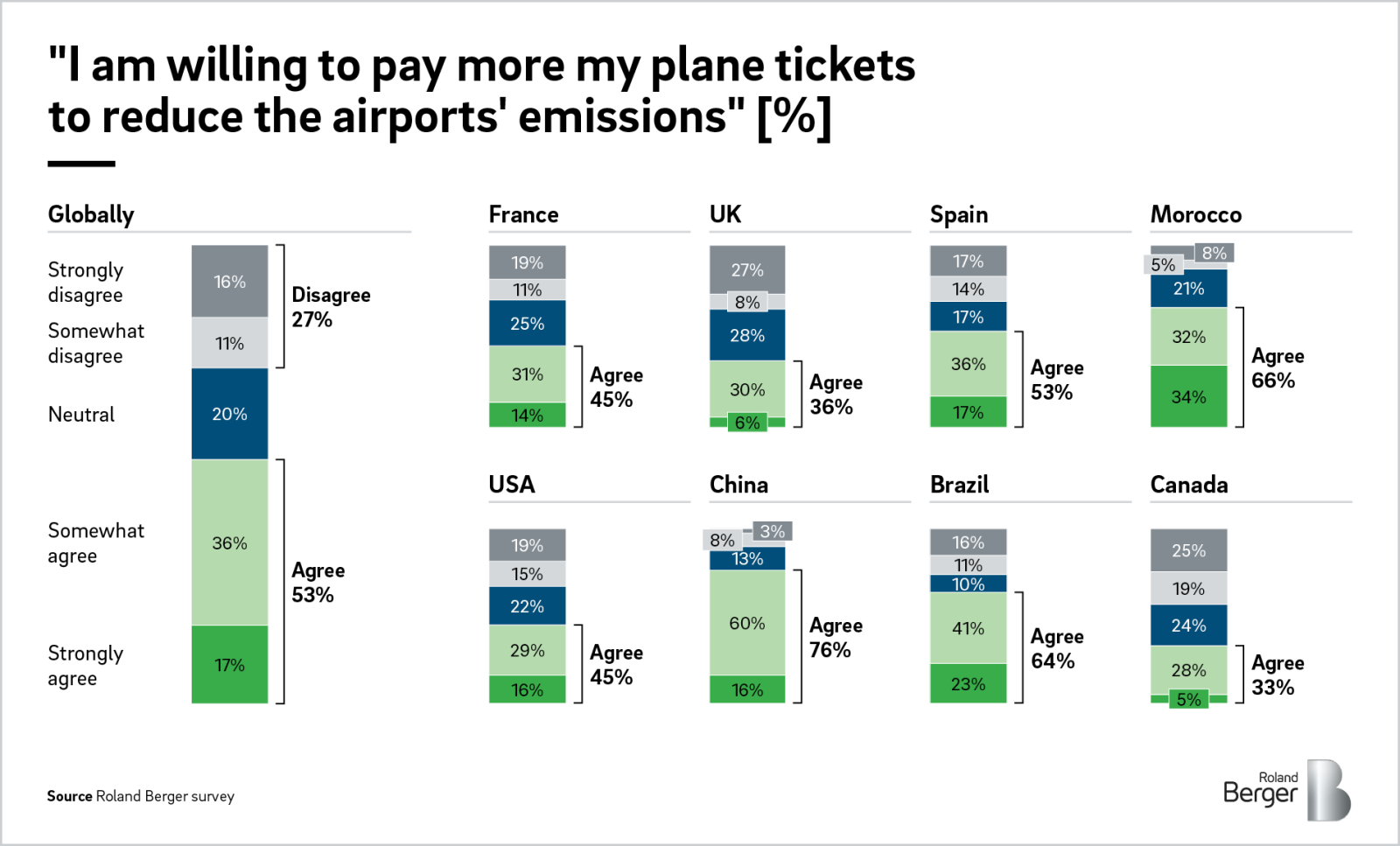

A survey of passengers conducted by Roland Berger in September 2022 in eight major countries – the United States, China, United Kingdom, France, Spain, Morocco, Brazil and Canada – reveals that around 60 percent of respondents believe that airports play a major role in air travel emissions, and need to act now. This confirms airports' role in passengers' imagination and the fact that they must embody the industry's transformation. The good news, backed up by the survey, is that as many as 53 percent of respondents are ready to pay more for their flights in order to help airports reduce their emissions. Interestingly, a significant number of passengers are ready to finance the transition regardless of which country they are in.

The source of the problem

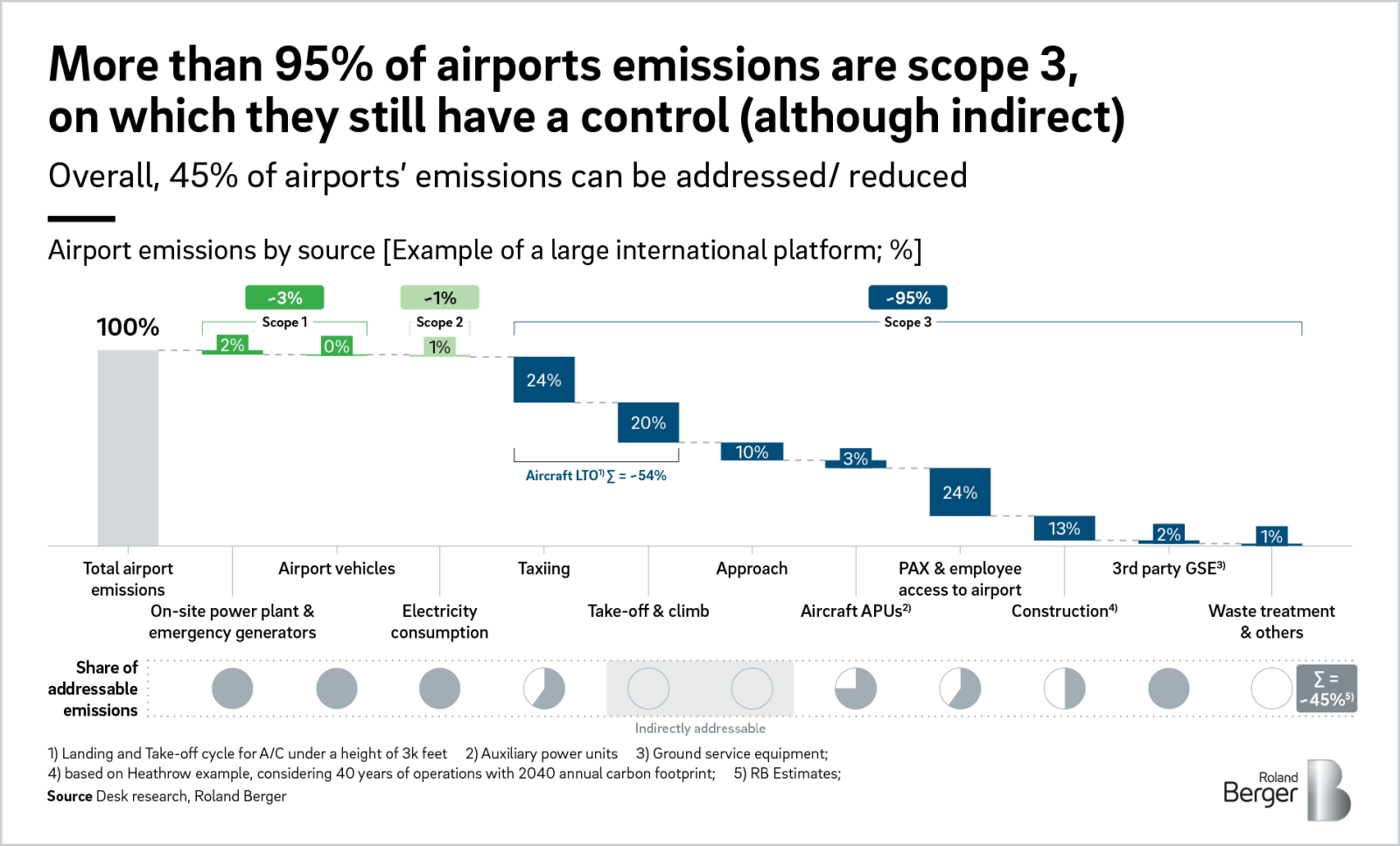

Of the three categories of emissions, Scope 3 is the most significant for airports, representing 95 percent of their total emissions (based on estimates for an international Tier 1 airport, using data from several major airports). Scope 3 emissions relate to pollutants emitted by the various different users of the airport platform, including airlines and ground services. For comparison, around three percent of CO2 emissions belong to Scope 1, stemming directly from the airport's onsite power plant or generators, and a further one percent to Scope 2, relating to the airport's consumption of electricity generated outside the airport.

Projects addressing Scope 1 and 2 emissions fall into three broad categories. First, we have projects aimed at improving energy efficiency, such as construction energy consumption audits and optimization. Next, there are projects aimed at reducing the use of non-renewable energy, such as renewable energy purchase, on-site generation of renewables and the use of electric vehicles. Finally, we have projects exploiting opportunities for carbon removal, such as onsite carbon removal and carbon offsetting.

When it comes to Scope 3 emissions, the role of the airport operator should be that of an enabler. Around 55 percent of airport emissions stem from airline operations, 25 percent from passenger and employee ground transportation, and 15 percent from airport construction. These are the areas where airports can take action, as many are already doing. Such actions include:

- Substituting diesel auxiliary units with "green" units (ground power systems, air conditioning units), which can cut total airport emissions by up to three percentage points. Similarly, using green equipment (cargo loaders, pushback tractors and so on) to serve aircraft on the apron can cut emissions by two percentage points

- Introducing electric taxiing systems, such as TaxiBot. This can have a major impact on the 20 percent or more of airport emissions generated by taxiing with conventional ICE vehicles

- Developing low-emission transportation alternatives for passengers and employees. Shifting from individual vehicles to public trains or buses and providing electric vehicle charging stations to passengers can cut airport emissions by as much as 15 percent

- Employing greener, lower-carbon building materials in new construction and maximizing structural efficiency with heat-reflective roofing, for example

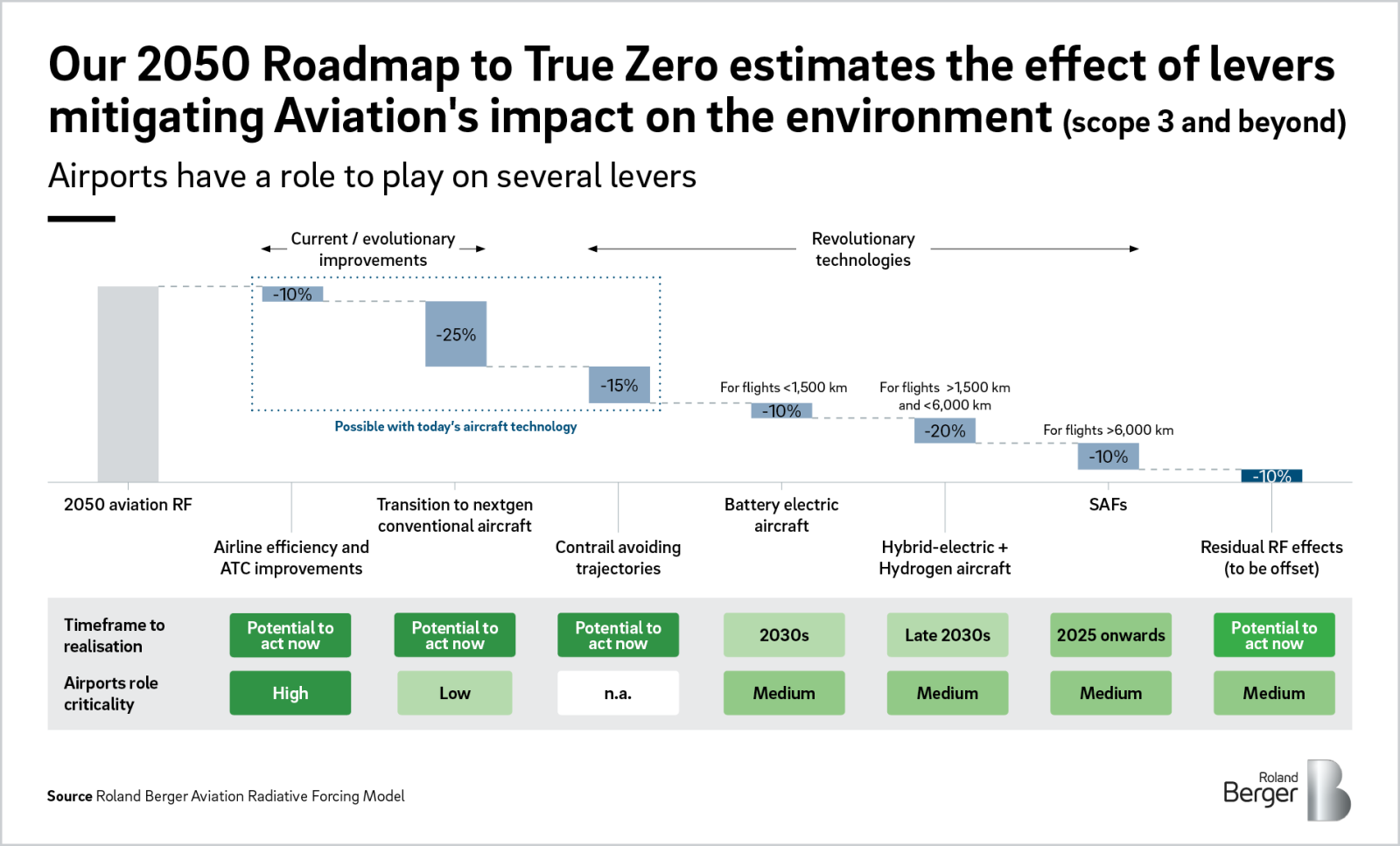

That said, the bulk of airports' efforts should be focused on helping airlines achieve greater sustainability, as fuel burnt by aircraft engines is responsible for most CO2 emissions and a strong factor in radiative forcing. One major area where airports can influence this is by pushing improvements in air traffic control (ATC), with the goal of limiting air approach waiting times and suboptimal flight paths, both of which lead to additional fuel burn. Other areas where airports can act as an enabler is in the use of sustainable aviation fuels (SAF) and, over the next 15-30 years, the introduction of battery electric and hydrogen-powered aircraft.

"Decarbonization is a matter of life or death for the aviation industry. Good news is that all players are mobilizing resources in order to cooperate and conjointly drive the ecological transition of the sector – with airports as enablers."

Sustainable aviation fuels – a near-term solution?

SAF would appear to be the most mature technology for powering aircraft in the near term, although it remains at an early stage of development. SAF production currently faces major hurdles, and a shortage of 1.5 Mtoe is expected in the year 2030 only. Such fuels are also much more expensive than kerosene at present, costing USD 9.5 a US gallon compared to just USD 2.6 for kerosene.

In terms of regulation, the future for SAF can best be described as complex but promising. Regulators are backing the technology as a means of decarbonizing the industry: For example, mandates in Europe and policies in the United States are currently aiming for 63 to 100 percent SAF uptake by 2050.

That said, adapting the fueling infrastructure at airports for SAF will be challenging. At the moment, SAF blends do not need separate infrastructure as they are designed to be integrated with traditional jet fuel, a process called "drop in". But if airlines wish to purchase different percentages of SAF blends, this raises a number of key questions. For example, if one airline wants to use 50 percent SAF and 50 percent jet fuel, and another wants to use 100 percent SAF, would an on-site blending facility be needed or could airports offer different SAF blends at different SAF farms, like at a gas station? Would blending facilities at airport gates best meet the airlines' needs? And what level of traceability would be required of airlines regarding the type of SAF purchased?

Other questions arise with regard to the production of SAF. For example, could production take place within or near to airports in order to avoid transportation costs? Local production coupled with airport blending facilities would mean that airport operators could purchase raw kerosene on the market and blend it with local SAF on the airport's premises. Resolving these and other questions will require close cooperation between oil companies, airports, airlines and aircraft manufacturers over the coming decade.

Hydrogen-powered aircraft – a solution for tomorrow?

Hydrogen-powered aircraft are even more efficient that aircraft using SAF, eliminating up to 90 percent of total emissions (in the case of green hydrogen) compared to 60-70 percent for SAF. However, the use of hydrogen technology is currently considered a longer-term goal. When it does come in, it will also likely have a more drastic impact than SAF on airport infrastructure, as hydrogen requires specific liquefaction facilities, storage facilities and refueling facilities, different from the current facilities for processing traditional jet fuel.

"Airport efforts should focus on helping airlines become more sustainable, as the fuel burned by aircraft engines is responsible for most CO2 emissions and is a major contributor to radiative forcing."

_person_144.png?v=1687234)

Nikhil Sachdeva

London Office, Western Europe

In fact, challenges exist along the entire hydrogen value chain. In terms of production, facilities could be located close to airports, as long as the necessary sources of renewable energy are found nearby. However, this would require a massive change of positioning by airports, which do not currently operate as energy producers.

With regards to transportation, hydrogen is usually transported in its liquid form: Hydrogen gas can be cryogenically liquefied to produce LH2 (liquid hydrogen), facilitating storage and transportation. In this case, liquefaction facilities would be required upstream, with the LH2 then being transported to LH2 storage facilities on the airport premises, or downstream at the airport if the hydrogen is supplied in gaseous form and then liquefied for storage and refueling on the aircraft itself. In terms of storage, dedicated H2 infrastructure would be required, either at the airport or at the production sites with the hydrogen delivered in liquid form by suppliers.

Finally, in terms of refueling, major changes would be needed. LH2 hydrant networks are needed in order to fuel aircraft at scale. This would necessitate massive investment and involve a complicated transformation of airport infrastructure. Given the complexity, on-board refueling would most likely be carried out by trucks at first.

Despite these uncertainties, airports should start thinking now about designing the necessary infrastructure, as massive hydrogen consumption is expected in 15 to 20 years' time.

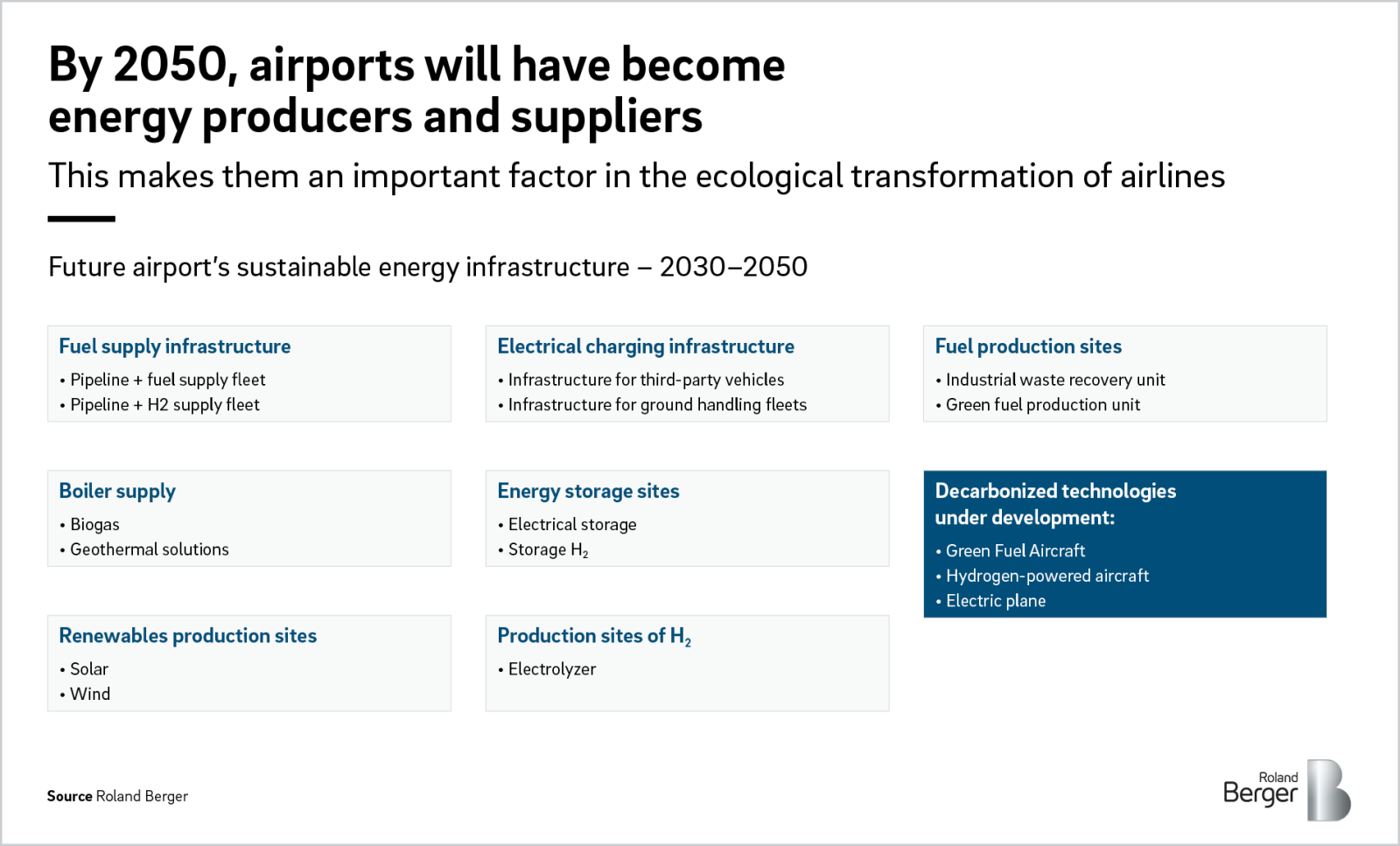

Airports as energy hubs

The shift from a "jet fuel only" approach to a "jet fuel + SAF + hydrogen" approach will have a radical impact on airports' infrastructure, operating model and business model. These new fuels open up an ocean of possibilities for airports – and a need for massive investments. Both SAFs and hydrogen can be produced locally, unlike kerosene, so airports should expect to become energy producers and suppliers by 2050 in order to best serve airlines' needs. This is an exciting, if challenging, opportunity for airports to disrupt the fuel production and distribution market. It remains to be seen whether they have the necessary investment capabilities and willingness to fight their way into an already well-established market with robust players.

Conclusion

The ecological transition is an exciting opportunity for airports – but one that comes with significant challenges. Airports that successfully demonstrate their ecological credentials to passengers, airlines, financers, public institutions and other partners can secure themselves significant competitive advantages. They will meet the needs of passengers who are looking for environmentally friendly ways to travel long distance. Airlines will be obliged to use SAF or hydrogen that is facilitated or even provided directly by the airport. And other stakeholders will see that airports are doing their part in global efforts to achieve sustainable transportation. All of this will require major investments – but the dividends for airports, passengers and ultimately the planet are clear.

We thank Vladimir Cabanis for contributing to this article.

Sign up for our newsletter

Register now to receive regular insights into Aerospace & Defense topics.

Further readings

Nikhil Sachdeva

London Office, Western Europe