From damage assessment to crisis preparation - an outlook on the PE industry

By Thorsten Groth and Christof Huth

Expecting a strong rebound towards the end of the year and the road to recovery

"A crisis is always an opportunity. "

With Covid-19 also having an impact on the PE market, some industries remain relatively unscathed while others deal with insolvencies and financial pressure.

In this interview, Senior Partner Christof Huth (CH) and Principal Thorsten Groth (TG) give insights on the current PE market development and some good advice for future crisis preparedness.

"Commercial due diligence is now more important than ever when it comes to new investments."

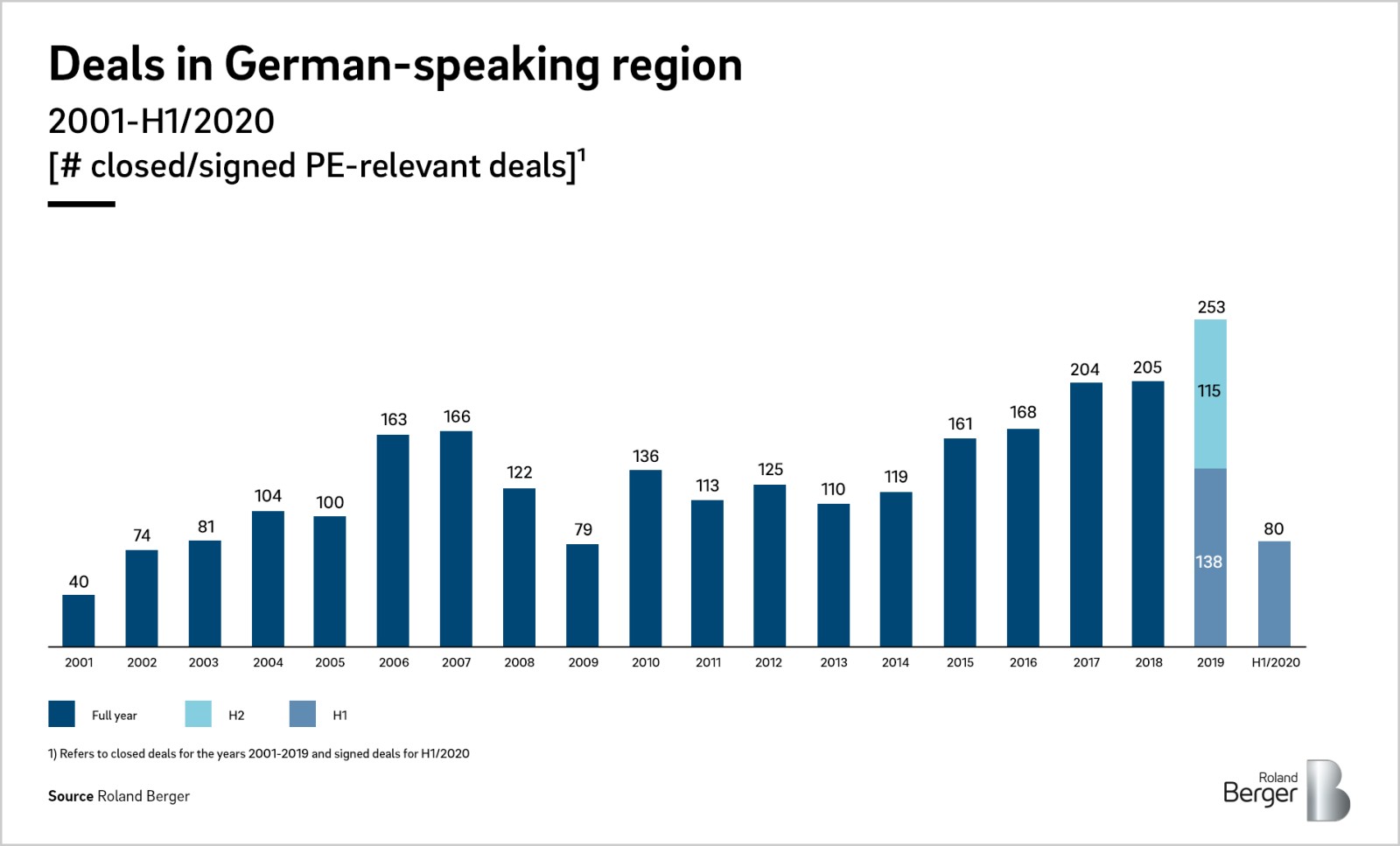

At the beginning of the year, Roland Berger's 2020 PE Outlook indicated that the industry was rather cautious and ready for more challenging times in 2020. However, virtually no one could have anticipated the disruption witnessed during the last few months – What has the impact of COVID-19 been on the PE industry and how do you expect the events of the next few months to unfold?

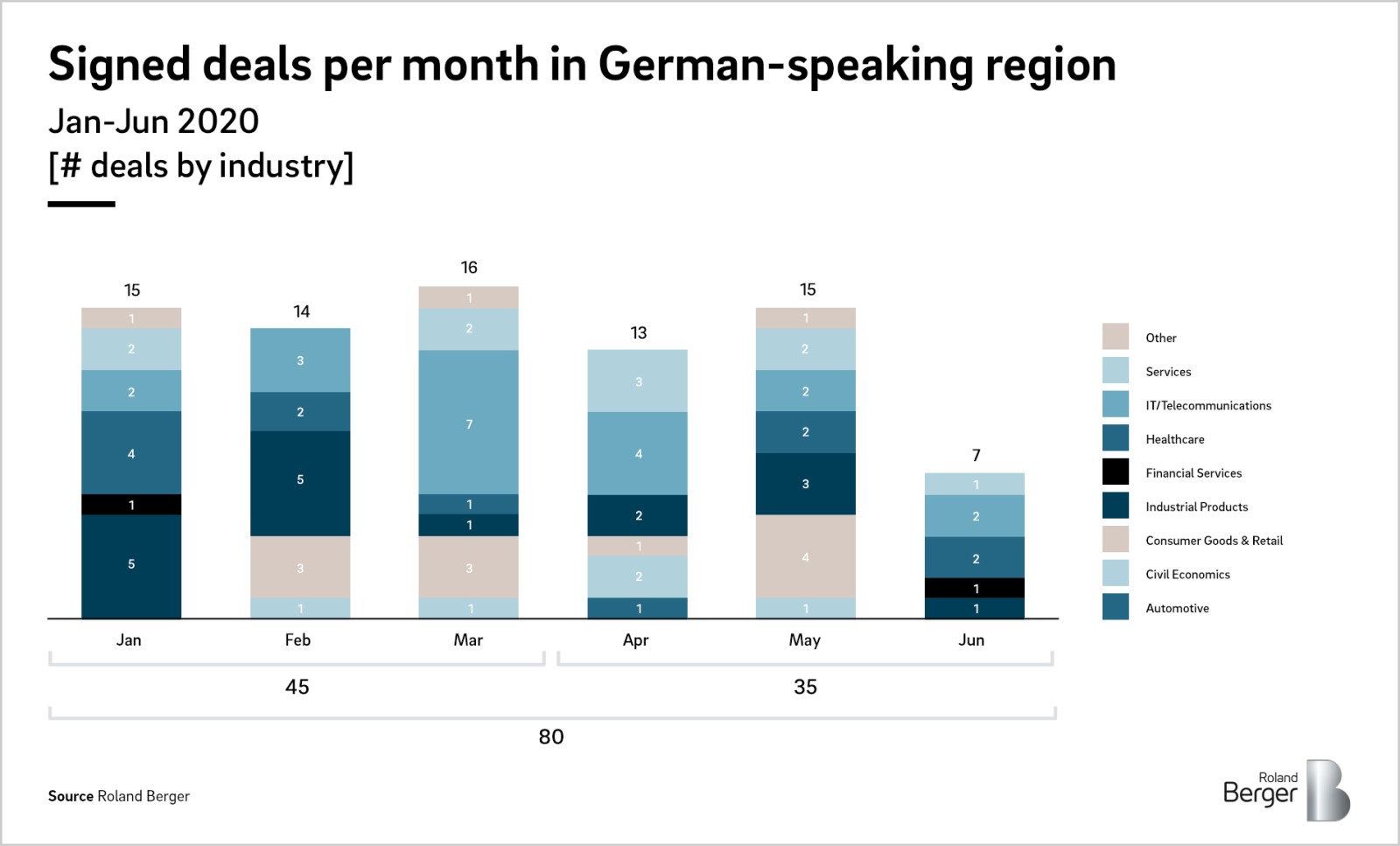

CH: COVID-19 has resulted in the strongest economic crisis I have experienced in my professional career, probably even more so than the economic & financial crisis of 2008/2009, and it has profoundly impacted all economic players including PE firms. In April, we experienced an almost complete halt to PE-related deal activity as the market digested the implications of the crisis and firms focused on the needs of their existing portfolio companies. But now, we are seeing a cautious return to deal-making in the DACH region, which we expect will accelerate in the coming weeks and months.

TG: We are seeing this return especially in those industries that have been relatively unscathed (e.g., software, technology, healthcare) or in those with long capital cycles where there is a search for "value-for-money" deals over the long term. However, there remains considerable uncertainty around the different COVID-19 recovery scenarios and agreements on valuations will remain a sticking point for many potential transactions. It may appear to be a buyers' market, but sellers are largely not willing to take significant discounts. In addition, we are seeing a fast-growing distressed M&A market, fueled by insolvencies and financial pressure in many industries as a result of COVID-19.

Given the very unequal economic impact of COVID-19, which industries and sectors do you expect will experience the most deal-making activity in the second half of 2020? What does this mean for the PE industry in 2020?

CH: Sectors such as healthcare, logistics and food & beverage have performed well despite the crisis and could experience significant interest from investors. On the other hand, we anticipate lower levels of activity in automotive and industrials, aside from distressed M&A. Overall, we expect sellers to extend holding periods rather than exit on unfavorable terms, which will result in a lower level of transactions initially. Given the high level of deal-making in the DACH region over the last couple of years, this could mean a very strong rebound towards the end of the year or in 2021.

TG: The current situation could accelerate trends that we were already seeing last year, notably high deal activity in software/IT/telecommunications/healthcare, given increased emphasis on digital solutions, and ongoing consolidation in healthcare , which continues to represent an attractive non-cyclical opportunity.

What has this meant for financing? Has this impacted transaction sizes?

CH: Lenders have taken a step back given the uncertain fallout from the situation and what this could mean for acceptable risk and leverage levels. This favors firms that can (temporarily) offer all-equity deals.

TG: Financing has been especially difficult for larger deal sizes. In the long term, however, we do not expect credit markets to remain frozen, as there continues to be significant funds available.

Which measures should PE firms take to weather the crisis and thrive in a post-COVID-19 world?

CH: First, understand the risks the current situation poses to your portfolio companies. Then work out what measures you can undertake to mitigate those risks and what value-creation proposition you can offer them. Finally, recognize that a crisis is always an opportunity, as was the case for those firms that acted boldly in 2009.

TG: Commercial due diligence is now more important than ever when it comes to new investments. You cannot predict the future, but you can understand a company's profile based on potential risk and recovery scenarios and test for resilience.