Exclusive Interview: Felix Mogge on Auto Industry Dynamics, Inflation Impact, and Electric Mobility Evolution

Global Automotive Supplier Study 2023

By Florian Daniel and Felix Mogge

Major new Roland Berger study shows how automotive suppliers can successfully navigate the tough challenges ahead

On the face of it, “challenging” is something of an understatement when describing what the next few years appear to have in store for an automotive industry already mauled by three straight years of crisis. Roland Berger’s Global Automotive Supplier Study 2023 analyzes where the pandemic, supply chain disruptions, the war in Ukraine and rising prices leave both OEMs and suppliers today. It takes a deep dive into the reasons behind the structural threat to revenues and earnings that is now further putting the squeeze on suppliers in particular. But it also clearly reveals where digitalization, the powertrain transition and a significant geographical shift in the automotive market are creating fresh opportunities for profitable growth. Practical advice is then provided on how different players can adapt their strategies to overcome the many and varied obstacles they will encounter on the road ahead.

Modest market growth and shifting patterns

"Many suppliers need dedicated performance programs to stabilize their margins and secure the company against future uncertainties."

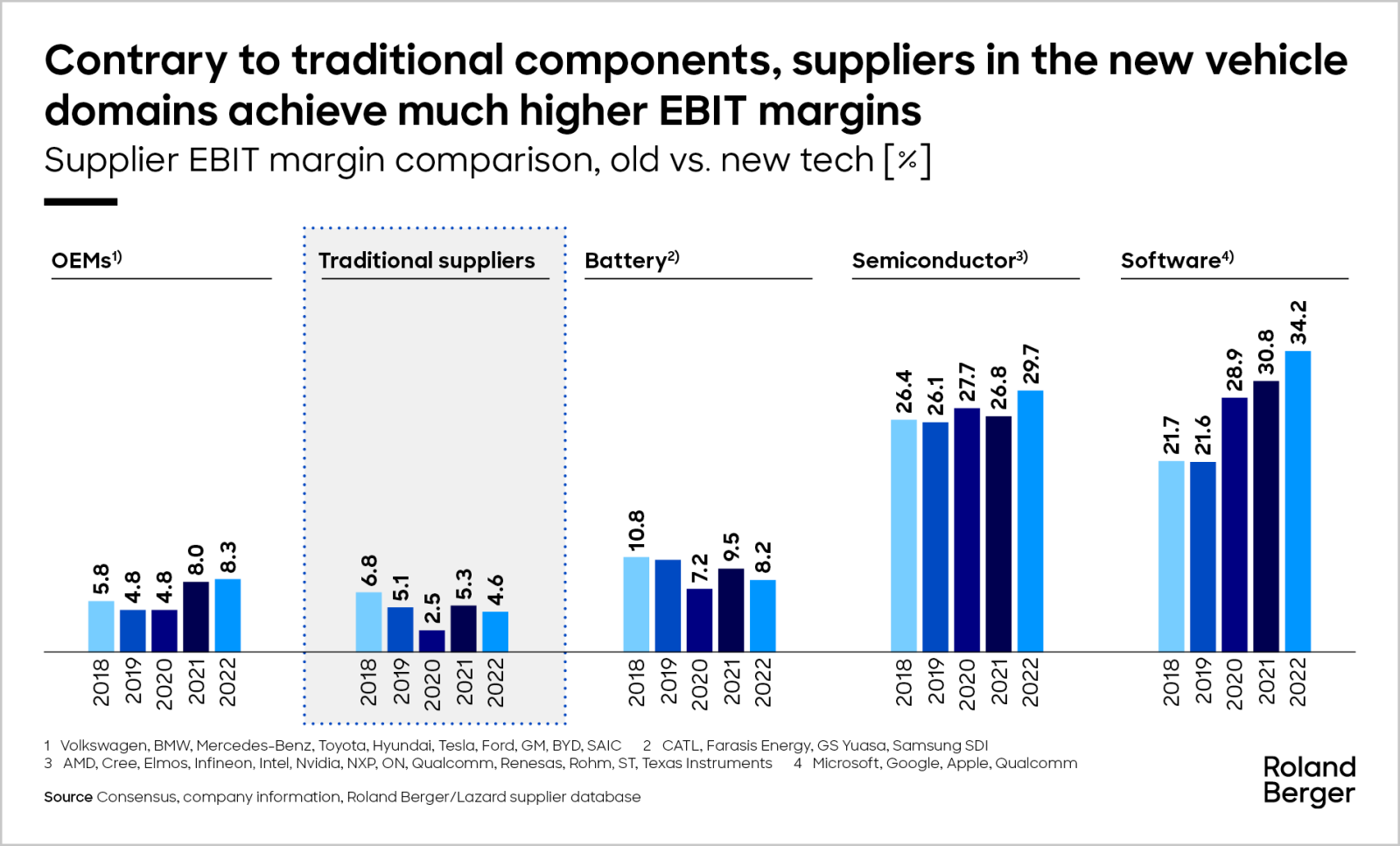

After an in-depth look at the nature and severity of the multiple struggles still facing every player in the automotive industry, the study highlights the importance of changing patterns of growth. Worldwide, growth is slowly returning to more stable levels. These, however, are much more modest than they were before the Covid-19 pandemic, and neither Europe nor North America are likely to return to such heady levels for the rest of the decade. Two factors make this situation even worse for traditional Western suppliers: One is that volume growth is visibly migrating eastward to Asia. The other is that conventional ICE-centric products are giving way to batteries, electrification components, software and digitalization as the principal sources of market growth.

Structural issues around profitability

Digging deeper, the study discusses the mechanics of how these seismic shifts confront North American and European suppliers with structural factors that are sharply eroding their profit margins. Here again, a conflation of many factors is clearly at work: Even as market volumes remain volatile, OEMs – who have themselves suffered and face their own daunting challenges – are increasingly unwilling to absorb cost increases from externalities such as high inflation. Suppliers therefore have to bear more of the risks themselves and can no longer fall back on the OEMs. This is also because the OEMs are increasingly facing more problems themselves as they have to cope with electrification and digitalization. Another key issue is the arrival of more and more tech-heavy newcomers in the automotive space – well-resourced players who are swiftly occupying those niches and areas where future growth will be most plentiful and lucrative.

The road ahead?

"Overall, the supplier market remains a growth business, albeit with different components, for different customers, and for other suppliers than today."

Close examination of the Chinese automotive market – which, along with Southeast Asia, will host the majority of anticipated growth in the years ahead – reveals that the make-up of this market is itself in a state of flux. The study traces how, encouraged by government incentives, indigenous Chinese suppliers are upping their game and increasing their share of Chinese OEMs’ business. This is happening even in the luxury vehicle segment – until recently the undisputed preserve of European marques in particular. Paradoxically, therefore, the still-growing Asian market could in effect shrink for European players who do not embrace the technological transformation and increasingly find themselves on the outside looking in.

This detailed picture leads the study to some sobering conclusions for traditional Western suppliers: With new players in the ascendency on traditional markets and Asian suppliers enlarging their own domestic footprint, incumbent suppliers must make good use of their remaining strengths – scale and deep pockets, in many cases – to reposition themselves and avoid becoming irrelevant to the future development of a market that is still growing.

Practical proposals for players with potential

As bleak as this outlook may seem overall, the study insists that where there is growth, there are opportunities. And where there are opportunities, there will be winners. There is no question that traditional Western players have a lot of thinking and a lot of work to do if they want to stay among those winners for the rest of the decade and beyond. However, they have it in their hands to do so if they radically realign their strategies and swiftly develop a sharp focus on five key areas: improving their performance, pivoting to Asia, procuring the new skill sets they need, partnering for scale (and skills), and carefully choosing the portfolio and positioning they wish to occupy.

Download the full Global Automotive Supplier Study 2023 and discover how your company can turn the challenge of change into realistic opportunities for profitable growth.

We look forward to engaging with you in a deeper discussion of the road ahead and how you envisage your company’s future.

Download the full study

Register now to access the full study, that explores how automotive suppliers can successfully navigate the tough challenges ahead. Furthermore, you get regular news and updates directly in your inbox.

Further readings