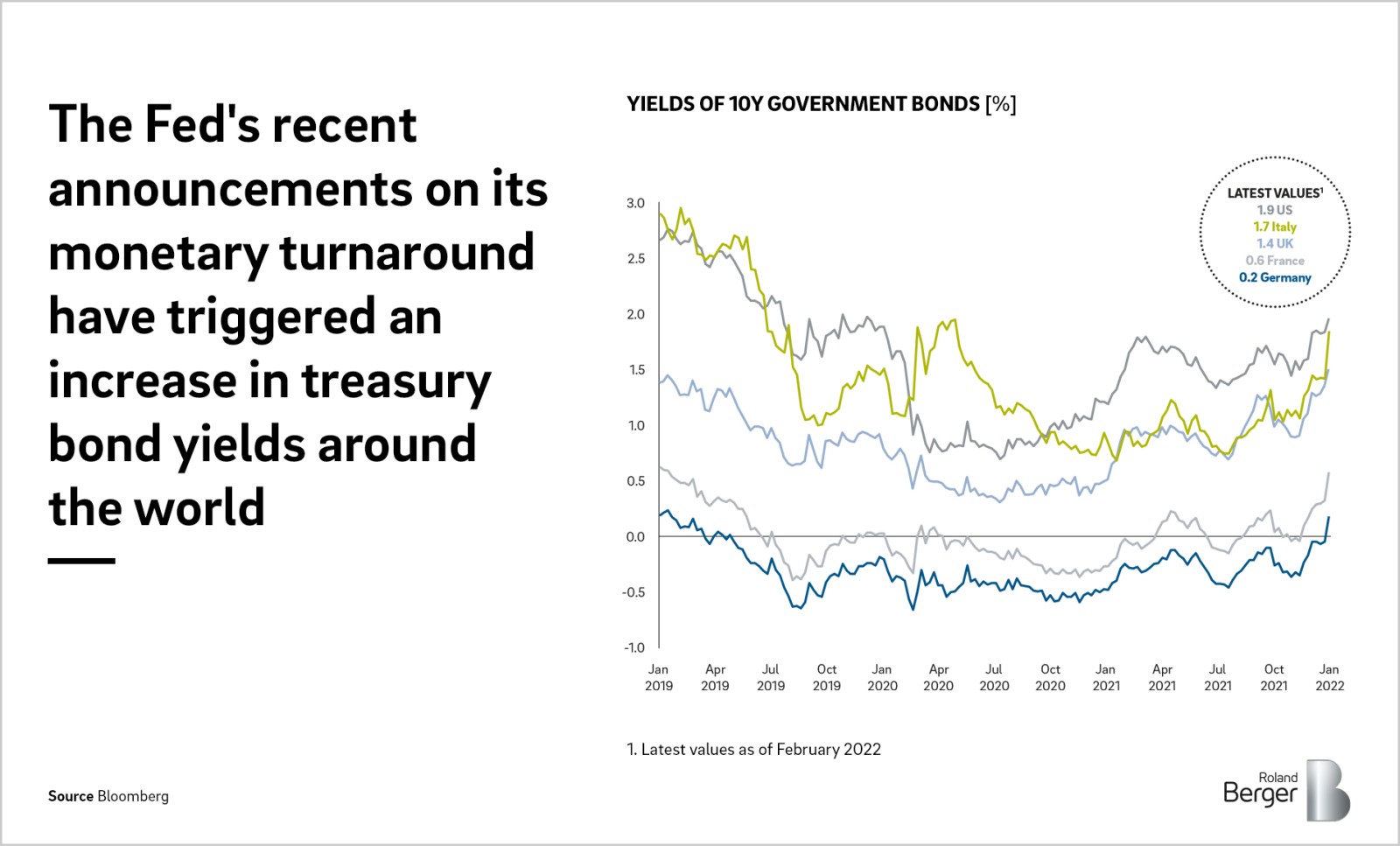

Figure 2 shows that the mere announcement by the Fed to end its bond purchasing program in March 2022 not only drove up the returns on U.S. government bonds but also had a knock-on effect on corresponding securities in the euro area's biggest economies. This demonstrates that investors not only react to actual market developments such as interest rate increases but rather anticipate these developments and factor them in accordingly.

Rising yields on government bonds increase the refinancing costs for commercial banks, who then pass these costs on to their customers in the form of higher interest rates on loans.

This brings us back to our initial question: What consequences will the ECB's interest rate increase have for the individual consumer, for businesses, and for the national economy as a whole?

A general increase of the interest rate will result in higher yields on savings deposits for consumers and will also lead to higher price stability as a result of a declining inflation rate. At the same time, loans will become more expensive, hampering private investment. In addition, higher interest rates could have a negative impact on consumption, hurting economic growth.

For businesses, an interest rate increase and the resulting decline in inflation would have the benefit of reducing the risk of a pending price/wage spiral. Businesses profit from price stability (including with regard to wages), as this facilitates planning regarding future costs and profits. Yet, higher borrowing costs would also make it more difficult for businesses to follow through with planned investments.

A decline in inflation would primarily protect those parts of the population that are particularly vulnerable to an increase in consumer prices as they use most of their financial means for everyday necessities. On the other hand, rising interest rates make government borrowing more expensive to obtain government loans, which could dampen public spending and thus weaken growth.

![{[downloads[language].preview]}](https://www.rolandberger.com/publications/publication_image/roland_berger_publication_02_fallback_download_preview.png)