Roland Berger offers strategic approaches and proprietary solutions for sustained success in the financial services industry.

Retail Banking Survey: Not striving for any change of business models despite digitalization

Intensified competition at the customer interface and a lack of innovations are thwarting banks

The survey of around 60 European retail banks from 11 countries as part of Roland Berger's 4th Retail Banking Survey shows: The pandemic is an important catalyst for digital transformation, but it will not radically change the retail banking business. This is because most banks are continuing to digitalize primarily existing products and processes but still rarely work on new innovative solutions. And even if agile working is gaining importance and job profiles are changing due to digitalization, the fixation of the majority on a positioning as "customer experts" and the lack of strict focus on digital initiatives is preventing a true transformation of business models and thereby a differentiation from the competition. Banks should scrutinize their orientation more consciously and focus on additional offers and services if they do not want to be superseded by new competitors.

"Banks must now act more consistently in order to not be superseded by big tech companies or fintechs."

Due to the closure of branches and the strict home office regulations during the lockdown, European banks were forced to digitalize their processes. 60 percent have developed new products within this context in order to be able to serve their customers even during the lockdown.

Even though some German banks are planning a significant reduction of branches, other countries are much more reserved. 80 percent of them state that only a small portion of their branches will be closed in the short-to-medium term. And around 90 percent believe that up to half of the staff will continue to work from their home office even after the pandemic. In addition, over 60 percent want to create agile working conditions for selected areas or projects. This will change future job profiles in some areas very strongly away from conventional project managers to data management specialists, omnichannel specialists, and Scrum masters.

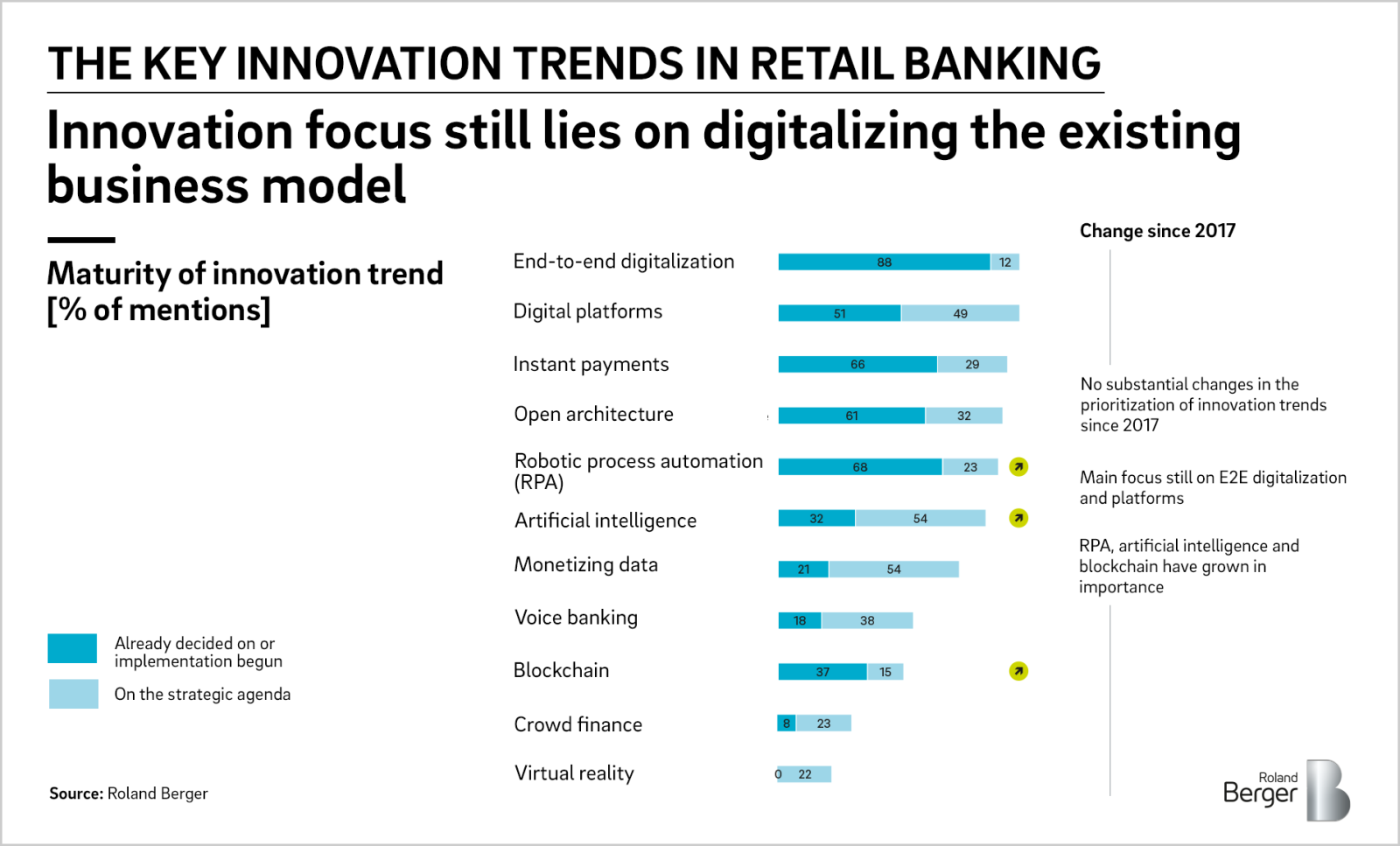

Digital maturity is increasing further, but the focus is not on innovative technologies

Even if 90 percent of respondents can conclude a consumer credit quickly and almost completely digitally, most banks are not moving forward in the implementation of innovative technologies such as artificial intelligence or blockchain, even though internal staff and cultural resistance to the digital transformation has fallen. The biggest hindrances continue to be the outdated, inflexible IT infrastructures (IT legacy).

Despite this, 92 percent of the respondents want to invest more in the digital transformation. It remains to be seen what these investments will fund, because approximately 70 percent of IT budgets are already now spent on maintaining daily business operations and meeting regulatory requirements.

Continuing fragmentation of the value chain, but no change of the business model

Despite the intense competition and oligopolization tendencies in customer acquisition, 81 percent of respondents still want to staff the customer interface first and foremost. Alternative strategic orientations as product experts or technology providers are not taken into consideration much.

The fragmentation of the value chain continues: Most banks are continuing to outsource processes, most of all in payment processing (73%) and compliance processes (49%). But there is no striving for a reorientation of the business model through these measures. Many banks lack a strict strategic orientation with an ambitious approach. Therefore, banks should scrutinize their focus on the customer inferface more consciously and focus on innovative offers and services. During the pandemic it became clear that telecommuting and digital interaction with customers are possible. Banks should now use these findings in a targeted way in order to approach the digital transformation more comprehensively and establish innovative solutions along the entire value chain.

Download study

Register now to download the study which shows you digitization processes in retail banking and get regular insights into our financial service topics.

Further reading

Our global network