Building a competitive local supply chain for sustainable growth

A local battery value chain is crucial for enhancing Europe's strategic independence, as it secures supply chains across vital industries such as automotive, energy, and defense. But the battery industry in Europe is under threat from low-cost, subsidized imports - jeopardizing its viability. Although demand is projected to reach 1.5 TWh by 2035, structural cost disadvantages and regulatory uncertainty threaten to shift value creation permanently to China. Decisive intervention is needed to ensure that the region is not risking the chance to create hundreds of thousands of jobs and billions in economic value in one of the century's most strategic industries.

The battery industry in Europe faces a fundamental test: whether it can translate projected demand growth into domestic value creation, or whether production will remain concentrated in China and other non-European markets.

Europe is expected to become one of the world's largest markets for

lithium-ion batteries,

with demand projected to reach approximately 1.5 TWh and a market volume of €130-150 billion by 2035, despite the recent slowdown in EV demand expectations. To meet the majority of demand with locally produced battery cells, a significant number of manufacturing facilities are already operational, representing an installed production capacity of approximately 200 GWh and having created roughly 80,000 direct and indirect jobs to date.

"Strong collaboration with established Asian battery players is critical for building European capabilities and competitiveness. Their operational and technical experience can significantly shorten our learning curve, enable faster innovation and lower costs."

Despite this potential, the industry faces considerable challenges. Structural cost disadvantages compared to Chinese imports, higher than expected ramp-up costs even for experienced players, and persistent market uncertainty — including slower electric vehicle demand and mixed political messaging on the trajectory towards zero emissions — are pressuring the competitiveness and viability of European production.

Furthermore, while many projects have been announced in recent years, a substantial share has failed, been discontinued, or postponed. This raises a fundamental question about the future of value creation in the battery sector: will Europe succeed in establishing a competitive, localized value chain, or will value creation remain largely in China and other regions?

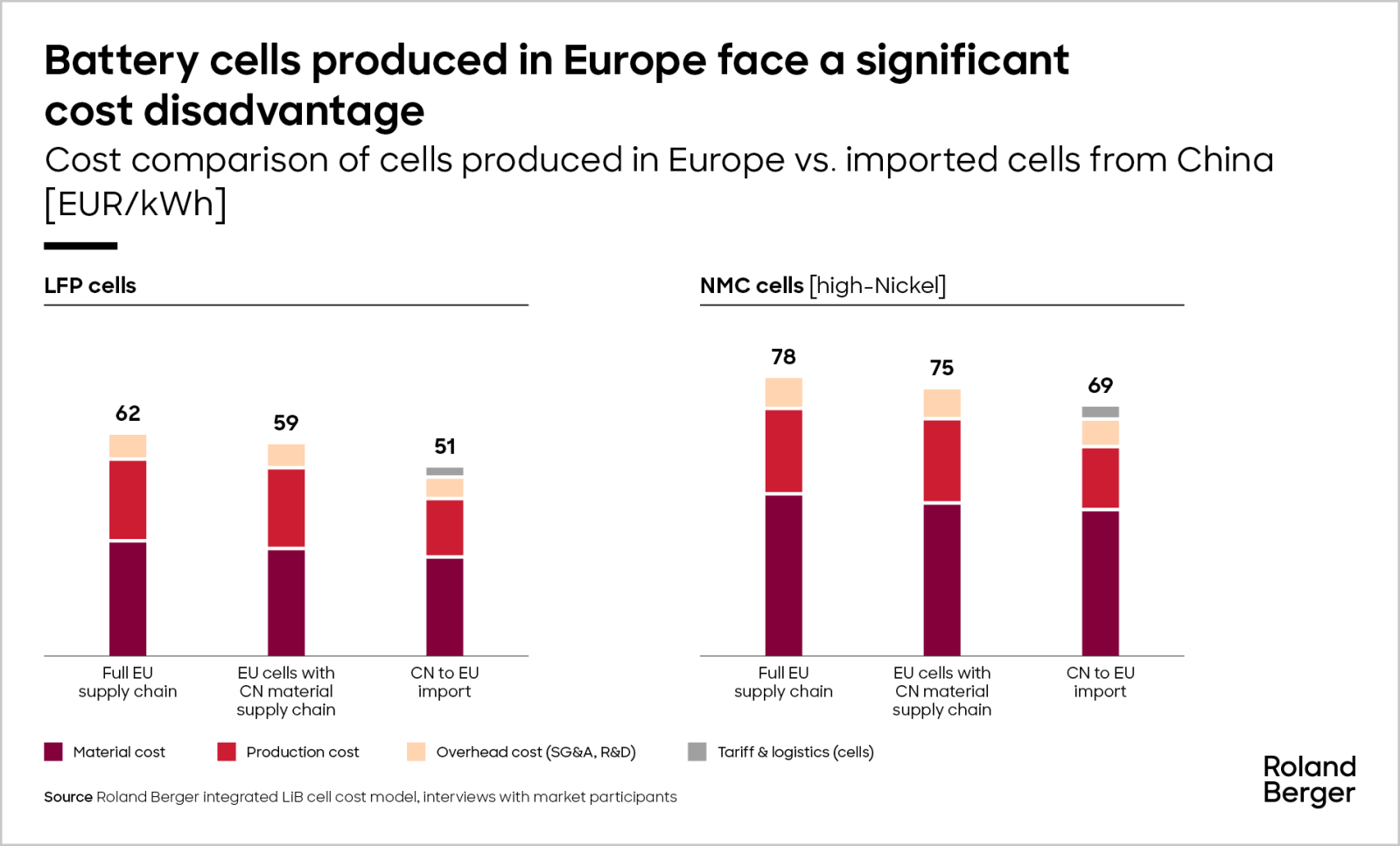

The cost challenge

Locally produced battery cells are projected to face a significant cost disadvantage, estimated at approximately 9-11 EUR/kWh compared to cells produced and imported from China. This gap stems from structural disadvantages in capital and operating expenditures that affect both new domestic entrants and established Asian players producing in Europe.

The

capital investment disadvantage

is estimated to be at least 50% to 100% higher for equipment and about 200% to 400% higher for building infrastructure, even for Asian manufacturers who largely replicate their facilities but must adapt them to local requirements. This results in additional investments of approximately €900 million to €1.1 billion for a 20 GWh facility. Operating cost disadvantages are mainly related to higher labor and energy costs. Ramp-up costs for new EU entrants are anticipated to add approximately €1.5 billion for a 20 GWh factory in Europe compared to new factories built by established Asian players.

Furthermore, significant overcapacity of cell production in China has intensified price competition, with prices approaching marginal costs. This situation presents considerable challenges for both emerging domestic manufacturers and established Asian companies operating in Europe.

Regulatory uncertainty and fragmented policy

Regulatory conditions in Europe threaten investment security, constrain rapid scaling, and increase costs. The core issue is a regulatory environment that is questioned repeatedly, and a lack of clear, long-term industrial strategy. Policy signals and detailed guidance that survive across election cycles are insufficient, unlike the more consistent, centrally coordinated approach seen in China.

The absence of a coherent, EU-wide battery industry strategy has led to fragmented regulation and planning uncertainty. Many measures, such as the Net Zero Industries Act (NZIA) and the Critical Raw Materials Act (CRMA), lack incentives for local content and binding requirements, offering limited leverage for true value chain localization. Current instruments are relevant, but their impact is diluted by slow rollout, non-binding requirements, and difficulties in accessing or allocating funds efficiently.

A central challenge is that current regulations are often not tailored to cell factories. Fire safety and building codes are major cost drivers, frequently prescribing detailed technical solutions rather than performance-based requirements. Hundreds of regulations, combined with the need to deal with a two-digit number of authorities to get the needed permits for a single plant significantly hinder project execution speed and increase costs. A “single point of contact”, responsible for facilitating and coordinating the entire permit-granting process”, while demanded within the NZIA, does typically not exist.

"A robust local battery industry is essential for Europe's strategic independence in critical sectors, reducing reliance on external sources and mitigating geopolitical risks. It also has the potential to create hundreds of thousands of jobs and significantly drive domestic value across the region."

Establishing a local battery value chain is crucial for enhancing Europe's strategic independence, as it

secures supply chains

across vital industries such as automotive, energy, and defense. The battery industry has the potential to make a significant contribution to Europe's economy. Our analysis shows that successfully addressing the challenges ahead could generate up to 310,000 jobs and contribute approximately €75 billion in value to Europe's economy by 2035 — but only with decisive regulatory intervention and coordinated strategy among all stakeholders.

The battery ecosystem currently supports approximately 80,000 direct and indirect jobs and contributes roughly €9 billion to Europe's economy. It comprises a diverse network of established companies, startups, and industry institutions spanning the entire battery value chain, from raw material extraction and refining through production of key battery materials to recycling and reuse projects.

Download the full report

to explore detailed scenario analyses and our six key enablers for building a competitive European battery ecosystem.

Iskender Demir, Konstantin Knoche, and Marco Koch also contributed to this article. We also gratefully acknowledge the support of Fraunhofer ISI, whose expertise helped us review and refine the assumptions underlying our assessment of the economic impact.

Report

Two outlooks for the future of battery manufacturing in Europe

Can Europe compete in battery production? Explore the challenges threatening local manufacturing and what's needed to secure strategic independence.

_person_144.png?v=1687234)

![{[downloads[language].preview]}](https://www.rolandberger.com/publications/publication_image/25_2419_MMP_european-battery-industry-forecast-thumbnail_download_preview.png)

_person_320.png?v=1687234)

_person_320.png?v=1687234)