Automotive & Commercial Vehicles

Elevate your business with our automobile consulting services. We provide expert advice, tailored for industry professionals seeking efficiency.

The car of tomorrow is becoming a software-enabled, cloud-connected device. New, more centralized electronics architectures and increasingly standardized software platforms are disrupting the automotive industry. Tier 1 suppliers play a vital role in the modern automotive value chain, supplying the complex electronics that are woven into the DNA of modern vehicles. But with growing pressure from technological disruption, value chain reshuffling and the emergence of a new software market, suppliers will find that they need to define a new role for themselves if they wish to retain their key position in future years and decades.

In Parts 1 and 2 of this series, we discussed how automobiles are transitioning from being little more than a means of getting from A to B, with the engine as their main feature, to a "system within a system of systems". Most innovations now take place in the area of electronics and software. Cars, with their online connections, automatic traffic updates, sensors, apps and integration into the Internet of Things (IoT) , have become essentially computers on wheels.

Traditional suppliers of these complex electronic systems play a critical role in the production of vehicles. But Tier 1 suppliers are increasingly under pressure – in three key areas.

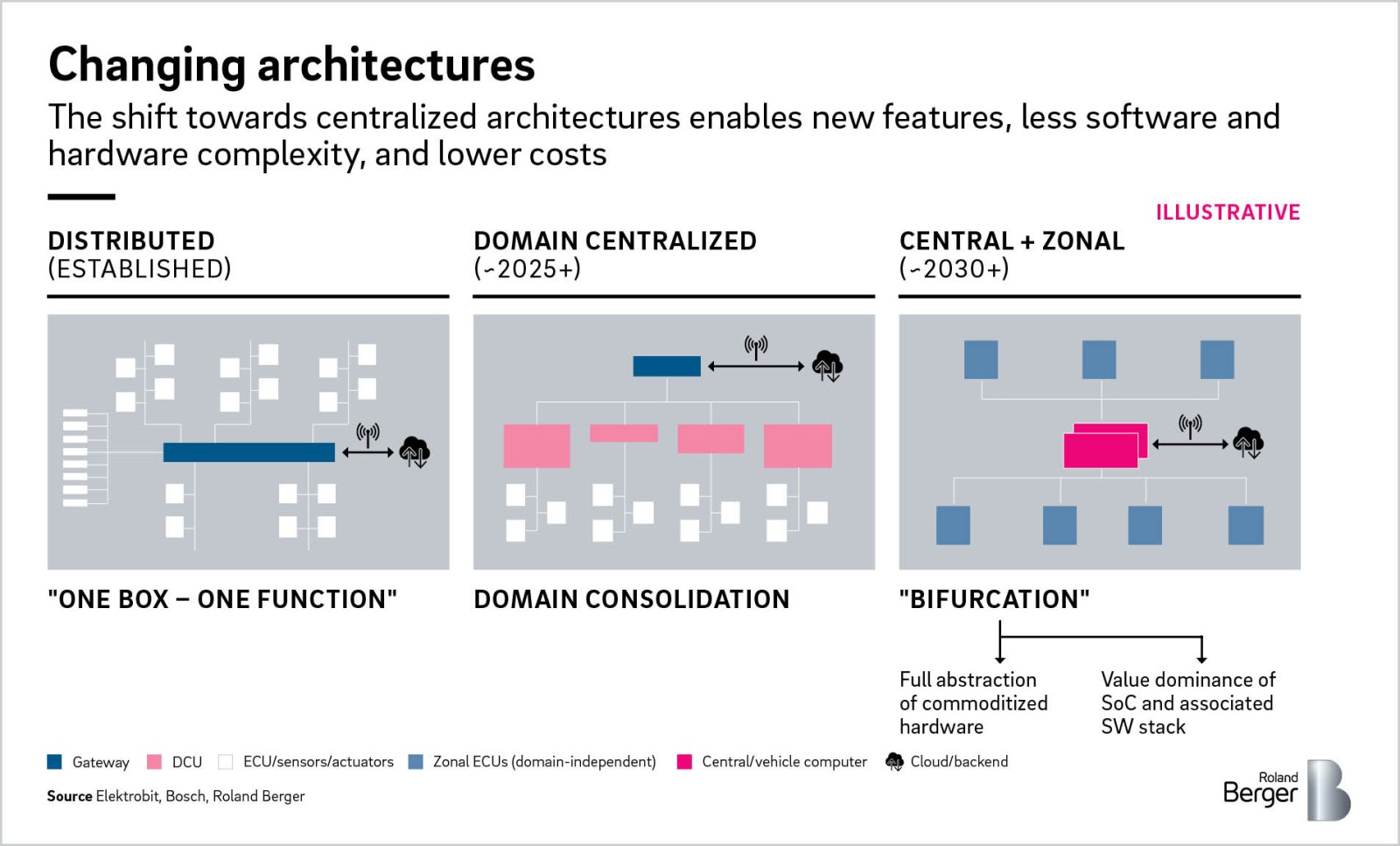

First, software and hardware are separating and architectures are gradually becoming centralized. This makes it possible to add new, more complex features faster and more cost effectively. It also leads to greater standardization of software and hardware, pushing down costs. Ultimately, it may lead to a unique situation for hardware suppliers in which complete electronics assemblies are fully commoditized, while individual semiconductor components dominate the bill of materials and hence the share of value.

"Developments are now moving incredibly fast. It's not so much the incumbent automakers that are calling the tune, but primarily the big tech companies and innovative startups."

Second, the value chain is being disrupted. New entrants, such as the tech giants Google, Amazon and Baidu, are muscling in on what was traditionally the territory of Tier 1 suppliers in particular domains, infringing on what has to date been their section of the value chain. Vehicle manufacturers are also beginning to subcontract directly to electronics manufacturing service (EMS) providers or "contract manufacturers", who buy components in bulk, leveraging their scale and commoditizing the market.

Third, a new software market is emerging. Of course, a software market of some sort has always existed. But what we are now witnessing is its true coming of age, as OEMs start to source software separately from hardware. The automotive market for embedded software solutions could be worth as much as USD 35 billion by 2030, depending on the level of standardization and consolidation in the industry. The consolidation of platforms, functional domain stacks and individual software elements that comes in the wake of this development will have an enormous impact on market size, driving down total costs. At the same time, it will push up the profitability of individual players to levels closer to those seen in other SaaP (software as a product) and SaaS (software as a service) markets.

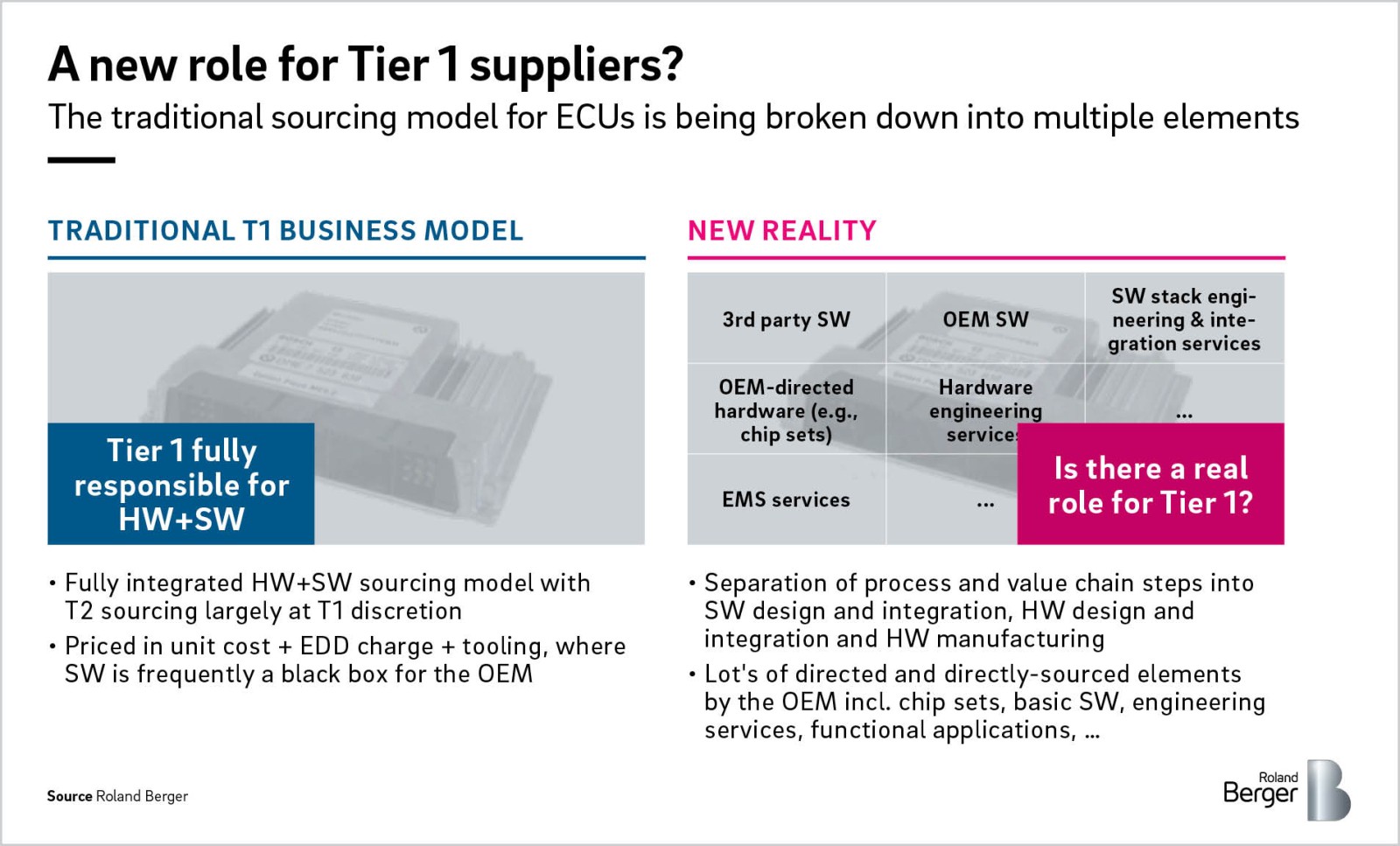

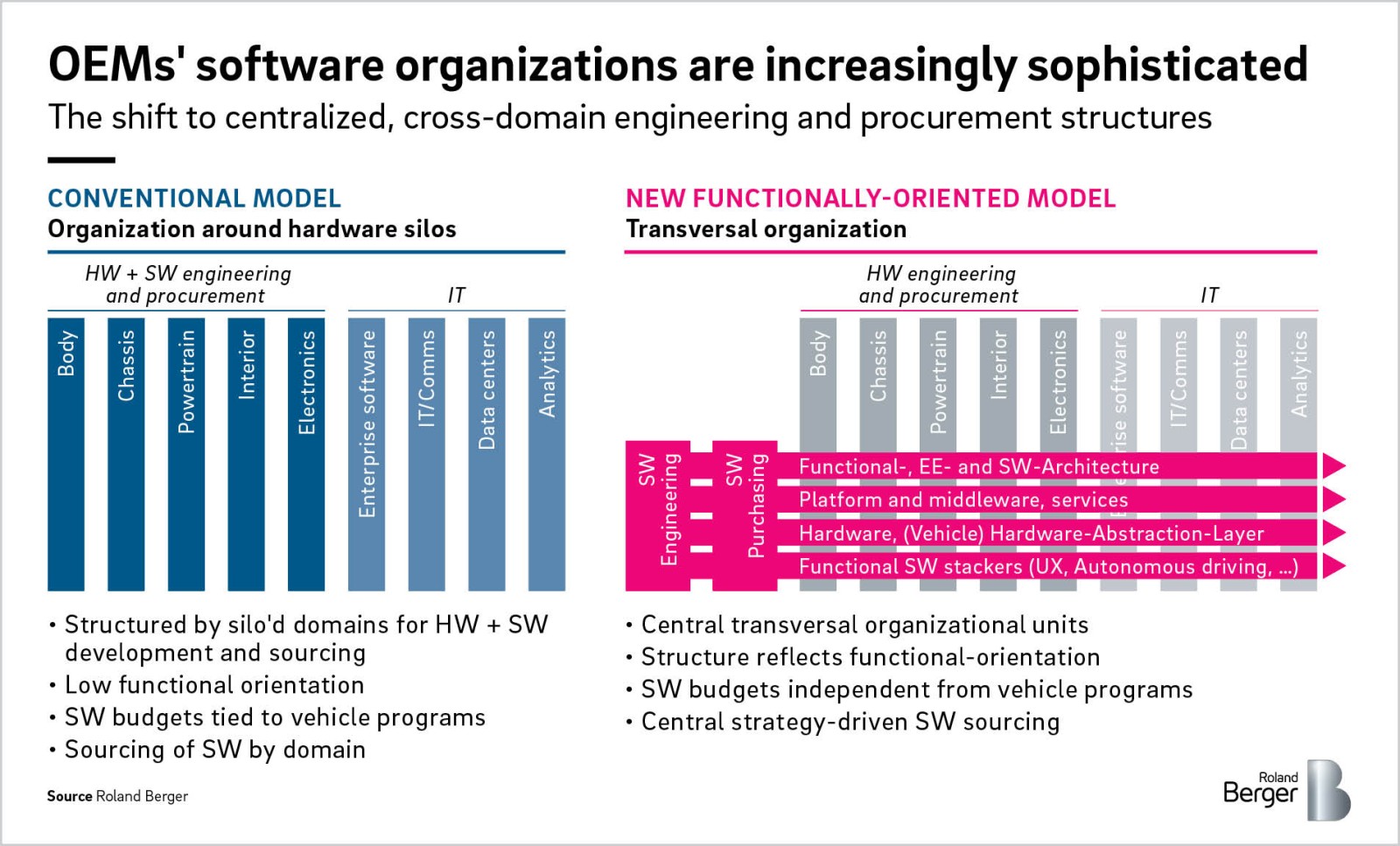

The general trends in electrical/electronic (E/E) architecture affect Tier 1 automotive suppliers and disrupt their established business models. Traditionally, OEMs sourced hardware and software from Tier 1 suppliers fully integrated into a single "box", the ECU (electronic control unit). Tier 1 suppliers, for their part, sourced from Tier 2 suppliers chosen largely at their own discretion. Now, the process and value chain steps are increasingly separated into three different sectors: software design and integration, hardware design and integration, and hardware manufacturing. Accordingly, suppliers need to manage a large number of software and hardware components produced by third parties and directly sourced by the OEM – from chip sets and basic software to engineering services and functional applications.

This is not the first time in history that we have seen such a development. The mainframe computers of the 1960s and '70s featured cutting-edge, custom-made hardware and custom software produced by the same manufacturer. By the time personal computers came along in the '80s, hardware had separated from software and we saw the emergence of distinct hardware and software platforms. In today's mobile devices, things have gone a step further, with the complete commoditization of hardware and software platforms ubiquitous across devices.

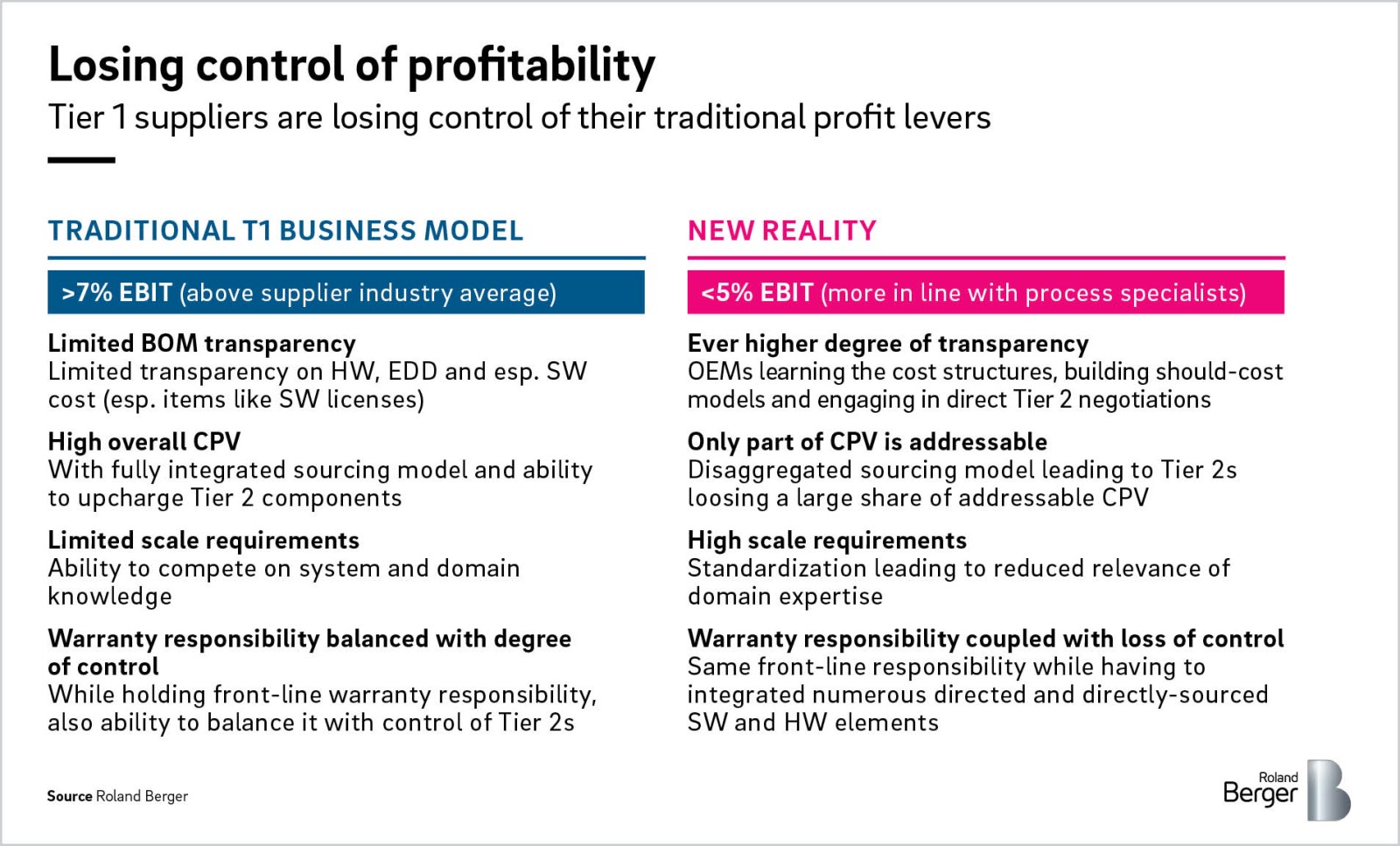

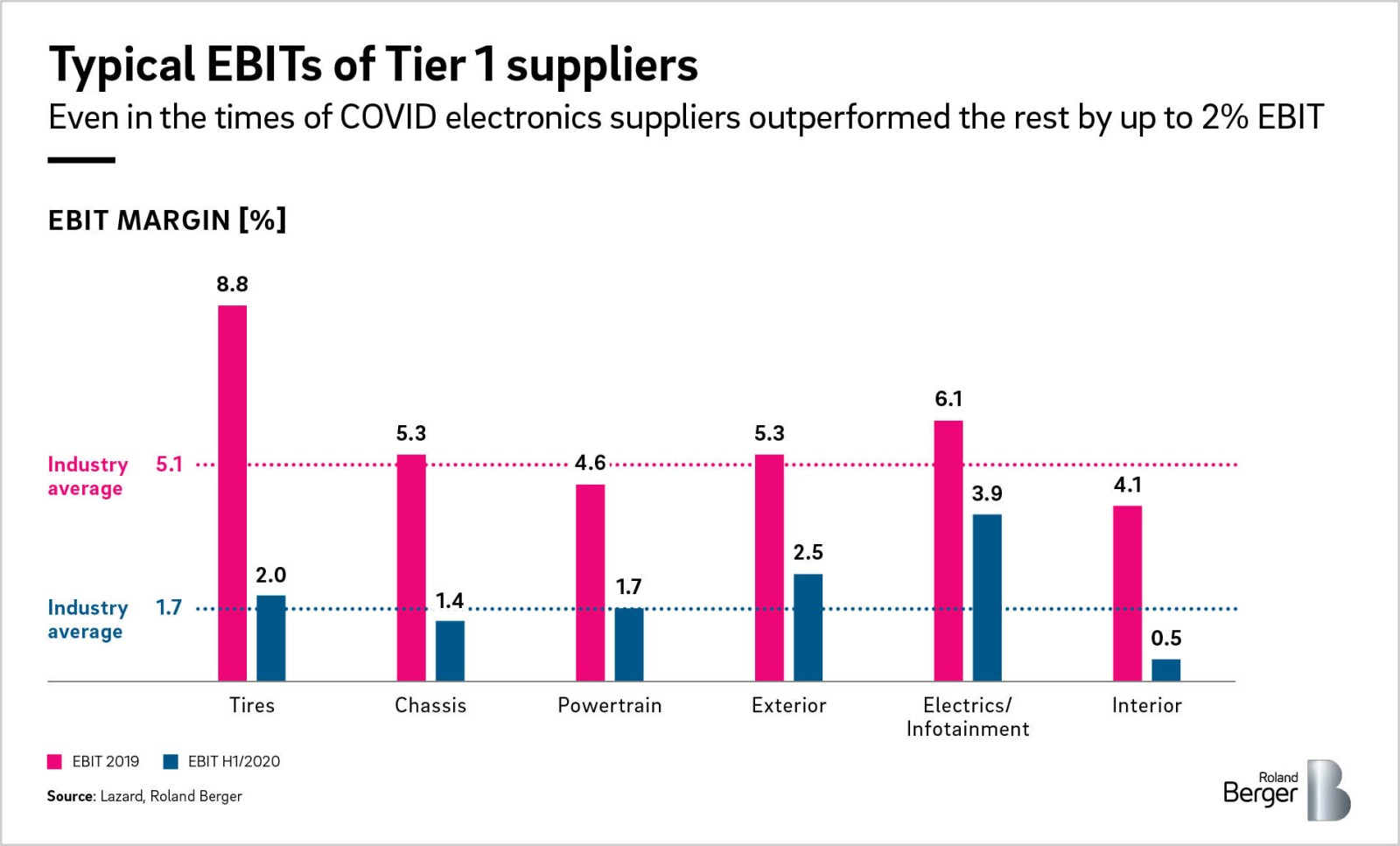

For the automotive electronics world, this change in business model means that Tier 1 suppliers are rapidly losing control of the profitability levers previously available to them – levers such as limited transparency over the bill of materials, high overall content per vehicle (CPV) and moderate scale requirements. This loss of control over profitability translates into real figures: Tier 1 suppliers of electronics enjoyed EBITs that were typically two percent above the average for suppliers (excluding those supplying tires, due to the high profitability of the aftermarket). This applies to both pure-play electronics suppliers (like infotainment) and diversified powertrain and chassis players with electronics products in their portfolio. Anecdotal evidence from recently sourced programs suggests that EBIT can even drop below five percent, a figure more in line with process specialists.

Tier 1 suppliers are also having to deal with functionally oriented organizational models – electronics, software engineering and sourcing organized "transversally". This new approach cuts across traditional silos and creates scale and transparency. That is great for OEMs but not so advantageous for Tier 1 suppliers. However, this disruption will not take place overnight. It will also vary by system domain, region and type of OEM. Thus, we are expecting to see disruption in areas such as ADAS and infotainment earlier than in vehicle propulsion or the chassis, say. Moreover, we are currently seeing regional differences in the speed of adoption: Premium European OEMs are already further along the path than OEMs in the United States, while China is somewhere in between.

With OEMs taking greater control of the value chain and Tier 1 suppliers gradually but steadily losing their unique value proposition as integrators, it is clear that Tier 1 suppliers need to take action. The question is, what should their new role be going forward? How can they redefine themselves so that they retain some of the power they enjoyed in the past? We investigate some of the options open to them below.

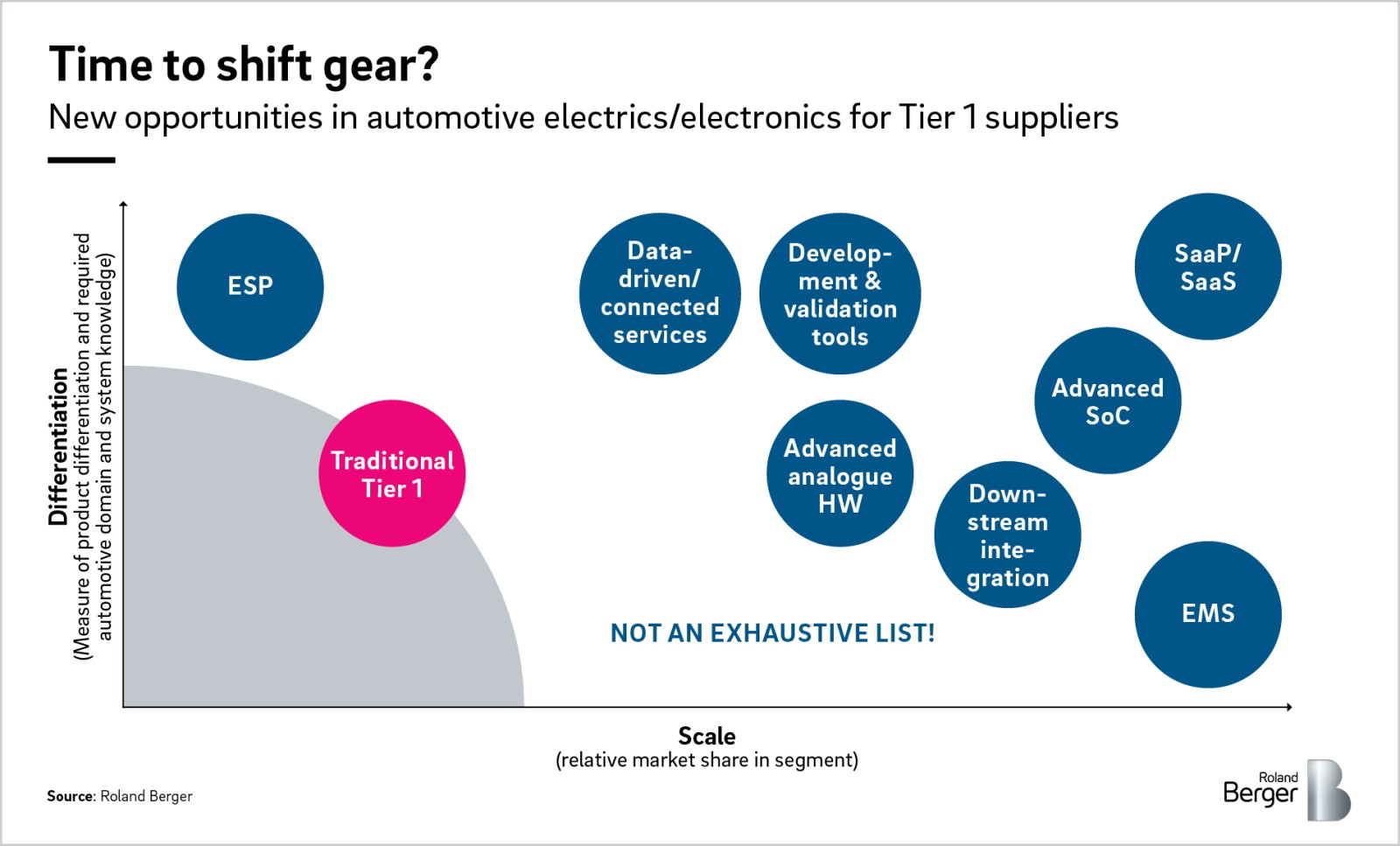

As the traditional business model in automotive electronics for Tier 1 suppliers gives way, a wide range of new options are opening up around which suppliers can carve out a new role for themselves. Models include becoming an engineering service provider (ESP), offering data-driven and connected services, creating advanced analogue hardware, downstream integration into modules and systems, advanced systems on chips (SoCs), and more. All of these options come with their own pros and cons: As is often the case, no one-size-fits-all solution exists. Some areas of specialization also call for unique capabilities, the ability to differentiate or to quickly achieve scale, as we examine further below.

Offering development services for hardware and software in a pure service model is a perfect fit with existing Tier 1 suppliers' competencies. It offers potentially higher margins even than those they enjoyed in the past if properly set up as a professional services business. However, the field is small and highly competitive, and suppliers will need to achieve meaningful size for shareholders in order to secure success. The size of this opportunity is comparable to the EDD (engineering design & development) fee charged by Tier 1 suppliers as a share of the overall lifetime value of the entire program.

Providing data and connectivity-enabled services directly to consumers, OEMs and other players has enormous potential as an option for Tier 1 suppliers – and indeed the entire ecosystem of players. However, solving the adoption challenge will be critical to success. This topic has been on industry's radar for at least 15 years, with very limited adoption so far. Challenges include hesitance and lack of understanding on the part of consumers, the cost of data transmission, archaic software architectures, and difficulties dealing with complex OEM organizations. Tier 1 players would also need to ensure that they have the "right to play", including access to data.

Designing tools and tool chains for the entire development and continuous deployment process – "shovels and pickaxes" for the industry – is an area of growing relevance and could be an option for some Tier 1 players. The market is small, however, and can only take a few players. As almost no Tier 1 suppliers currently have the necessary competencies, going down this avenue will generally involve acquiring an existing player in this field.

Providing software as a product or software as a service – that is, selling the platform or the functional (application) software – has strong growth potential as an option for Tier 1 suppliers. It is also a good fit with some of their existing competencies. On the negative side, the content per vehicle (CPV) is lower than in some other areas, while the supplier would potentially assume a greater volume risk. Achieving scale and dominance with differentiating features in specific segments will therefore be critical for success.

Developing high-value SoCs with a high degree of functional software stack integration is attractive for Tier 1 suppliers looking for a new role, particularly as it offers a dominant share of the component value. However, Tier 1 suppliers currently lack competencies in this area and will need confidence to step into the chip-making world. This option is likely accessible only to a very narrow list of current electronics Tier 1s.

Designing high-value electronic and mechatronic components such as LIDARs – light detecting and ranging technology that uses lasers to measure distances – represents a good fit with existing Tier 1 suppliers' competencies. However, the current market is still of limited size and the technology is subject to commoditization. Continuous product innovation and active portfolio management are key for players entering this field.

Entering the world of full systems, potentially all the way to producing complete vehicles, is another option for Tier 1 suppliers. This tactic offers high CPV but at the same time requires new players to develop major new competencies, step up in the value chain and potentially engage in supply and partner relationships with current competitors. As yet, market demand is uncertain and will need to be validated. Entering into competition with your current customers also harbors a certain amount of risk.

Large-scale, built-to-print electronics manufacturing is an area of strong growth in a large market. Competition is also strong, however, and players will need to keep costs low by achieving scale – potentially outside the automotive world – in order to achieve success.

Which of the options above are the most promising for individual Tier 1 suppliers is far from obvious. Suppliers will need to evaluate their specific situation, the domain they operate in, their scale, resources and their current competencies. On this basis they should then develop a clear portfolio strategy, define an appropriate operating model (potentially including partnerships) and draw up a roadmap for transforming their traditional business model into one that will stand up to the coming disruption. In some cases, they will likely have to operate several different business models in parallel. The need for Tier 1 automotive suppliers to shift gear is clear. But which direction – or directions – they should head in must be determined on a case-by-case basis.

Sign up for our newsletter and get regular updates on Automotive topics.