Advanced Technology

The latest innovations in technology, AI, and software solutions for industries including automotive, industrials, and energy, allowing businesses to adapt their operating models, strategy, organizations, and processes.

Not so long ago, cars were defined by their hardware; now, software is playing an increasingly important role in the auto industry. Software-defined vehicles (SDVs) feature an array of computer-powered features that can be continuously updated over a vehicle’s entire lifespan. SDVs promise to improve safety, efficiency, and convenience for drivers and passengers, as well as create new business models and revenue streams for carmakers and mobility providers. Despite these undoubted advantages, however, there are numerous challenges with SDVs – with rising costs among the biggest.

"There are fundamental differences in how OEMs approach the SDV challenge."

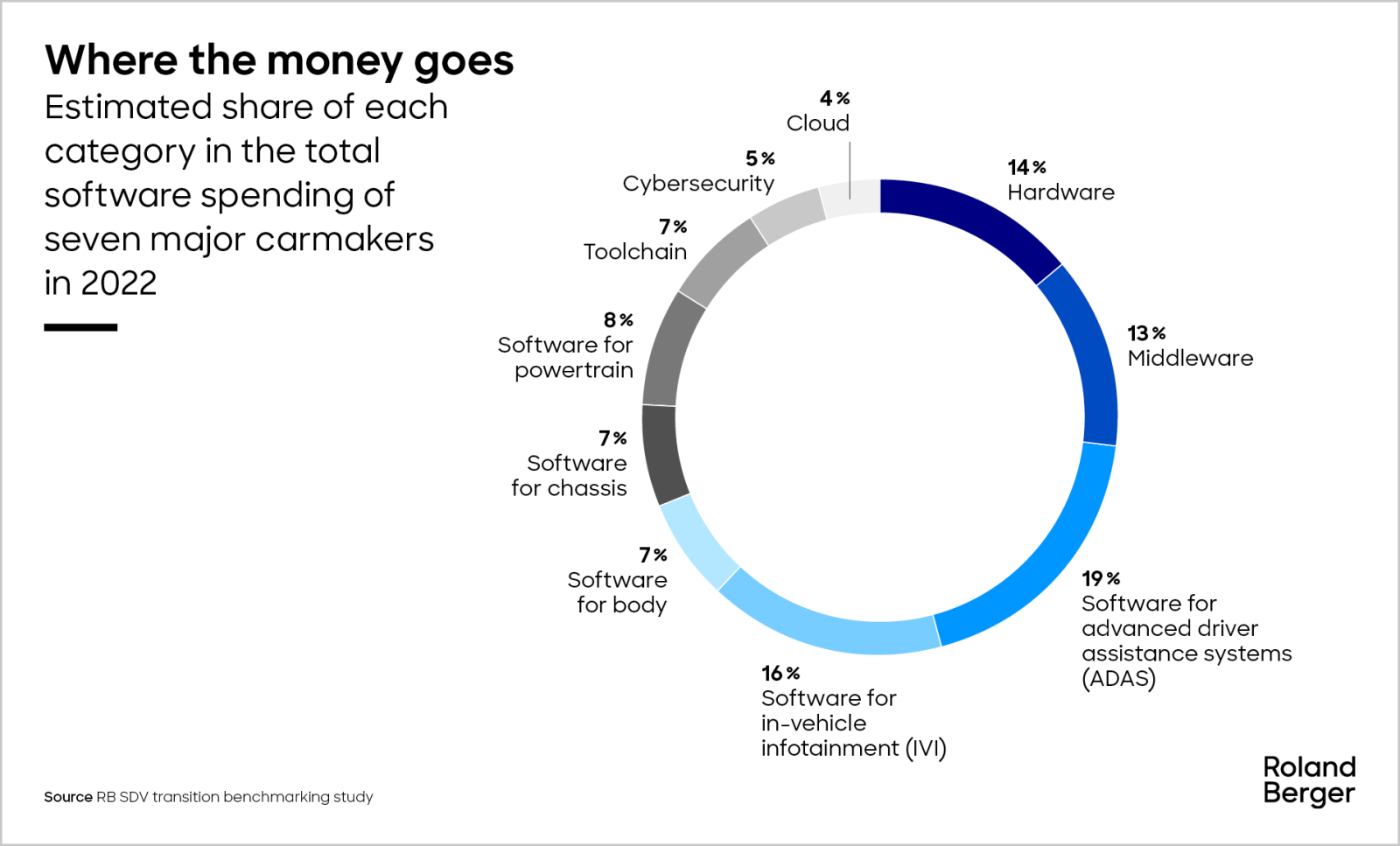

In our recent analysis of seven major automakers, we established they are currently each allocating between 25% and 30% of their R&D budget to software. In 2022, that equated to EUR 12.7 billion between these seven firms; by 2027, that sum will grow to EUR 15.4 billion, driven by the increasing complexity and functionality of software in vehicles.

For our analysis, we divided software spend into 10 categories, ranging from advanced driver systems and infotainment, to powertrains, and cybersecurity. We also identified the main drivers and trends for each category as well as the degree of outsourcing and insourcing of software development by carmakers.

The chart below shows the estimated share of each category in the total software spending of the seven carmakers in 2022, based on our data. Detailed insights into the latest trends in each category then follow.

Hardware (HW) includes high-performance computers, domain controllers, and electronic control units that enable the execution of software in vehicles. Some carmakers (e.g., BMW, Mercedes-Benz) are investing heavily in developing their own hardware to improve computing efficiency and reduce dependence on suppliers. This category is expected to grow at a moderate pace, as hardware costs decline and standardization increases.

Middleware (MW) provides the foundation and interface for software applications in vehicles. Most carmakers are increasing their MW spending to develop their own software stacks, often with the aim of maintaining sovereignty over data and remaining independent from partners. We expect rapid growth in this category due to increasing MW complexity and functionality, and the importance of differentiation for carmakers.

"Matching the leaders in software development efficiency will be critical for OEMs’ long-term competitiveness."

Software for advanced driver assistance systems (SW – ADAS) covers features such as lane keeping, adaptive cruise control, and parking assistance. This is a major focus for carmakers as they seek to differentiate themselves from competitors. In the long term, some carmakers (e.g., Mercedes-Benz, BYD, General Motors) will look to maximize their in-house development of ADAS software, while others rely on suppliers or partners. This category is expected to grow extremely quickly.

Software for in-vehicle infotainment (SW – IVI) is a key spending area for carmakers, and includes entertainment, navigation, and connectivity features such as multimedia, maps, and voice assistants. These features are crucial to user experience and, in the long term, some carmakers (e.g., Volkswagen, BMW) will aim to control more of them in-house; others will prefer to rely on suppliers or partners. This category is expected to grow rapidly.

Software for body (SW – Body) includes features, such as lighting, climate control, and door locks. This is a stable spending category as most of the software functionality is embedded in the hardware offerings of suppliers. As a result, the pace of growth will be slow.

Software for chassis (SW – Chassis) covers steering and braking features like power steering, anti-lock brakes, and stability control. Like body software, this is a stable spending category, expected to grow slowly.

Software for powertrain (SW – Powertrain) controls engine and transmission features including the battery management system, engine control unit, and transmission control unit. This is a growing spending category as carmakers are developing more complex software for electric powertrains. Some (e.g., GM, Scania) are willing to increase their insourcing of powertrain software. We expect moderate growth in this sector.

Toolchain software supports the software development lifecycle including continuous integration, continuous delivery, testing, and debugging. This is also a growing spending category, with many carmakers outsourcing the work to suppliers or partners due to a lack of in-house capability. This category is expected to grow at a moderate pace.

Our analysis shows that although the seven companies share similar spending patterns, there is a major gap between the highest-spending OEM and the lowest: Despite similar levels of target functionality, the top spender invests five times more in software than the lowest spender.

While this can partly be attributed to portfolio complexity and other objective factors, there are fundamental differences in how OEMs approach the SDV challenge: some approaches can generate significant cost efficiencies and help curb soaring SDV budgets. In future articles, we’ll explore these topics in more detail as well as outlining how to create an efficient SDV roadmap and the benefits this can bring.