Flyer

The German economy in the second half of 2021

![{[downloads[language].preview]}](https://www.rolandberger.com/publications/publication_image/20210901_RB_SAL_21_014_FLY_Konjunktur_2021_E_Cover_download_preview.jpg)

This study analyzes Germany’s economic development in 2021 and looks ahead to the coming months.

Published September 2021. Available in

By David Born

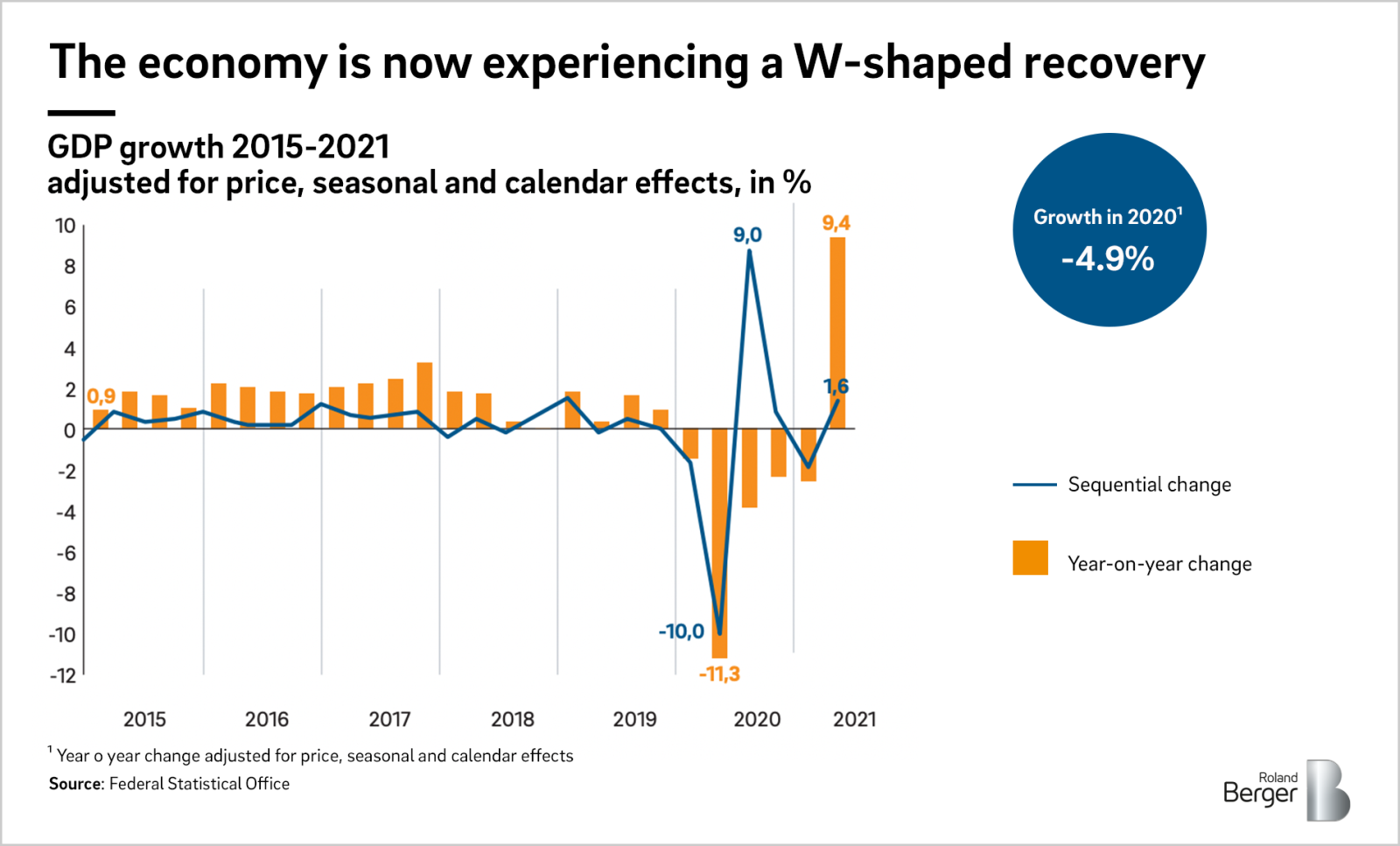

Hopes of a rapid economic recovery in Germany have been disappointed – not least due to the third wave of the coronavirus pandemic, which forcibly delayed plans to open up the economy in the spring. At the same time, the German economy continues to struggle with the fallout from last year’s production outages and the associated bottlenecks. This is seen most obviously in the lack of semiconductors and chips in the automotive industry, where some companies have once again had to scale back production.

It is therefore no wonder that, in the first quarter of 2021, GDP again fell by 2.0% sequentially and as much as 3.3% year on year. At least the second quarter proved a little brighter after the pandemic-related restrictions were revoked: Compared to the same quarter a year ago, GDP climbed by a full 9.2% between April and June 2021.

A close look at the economic data identifies higher consumer spending as the mainstay of current expansion. Private households in particular accumulated substantial savings last year – savings they are now increasingly spending. The service sector is one of the main beneficiaries, posting strong gains again now that measures to contain the coronavirus have been eased.

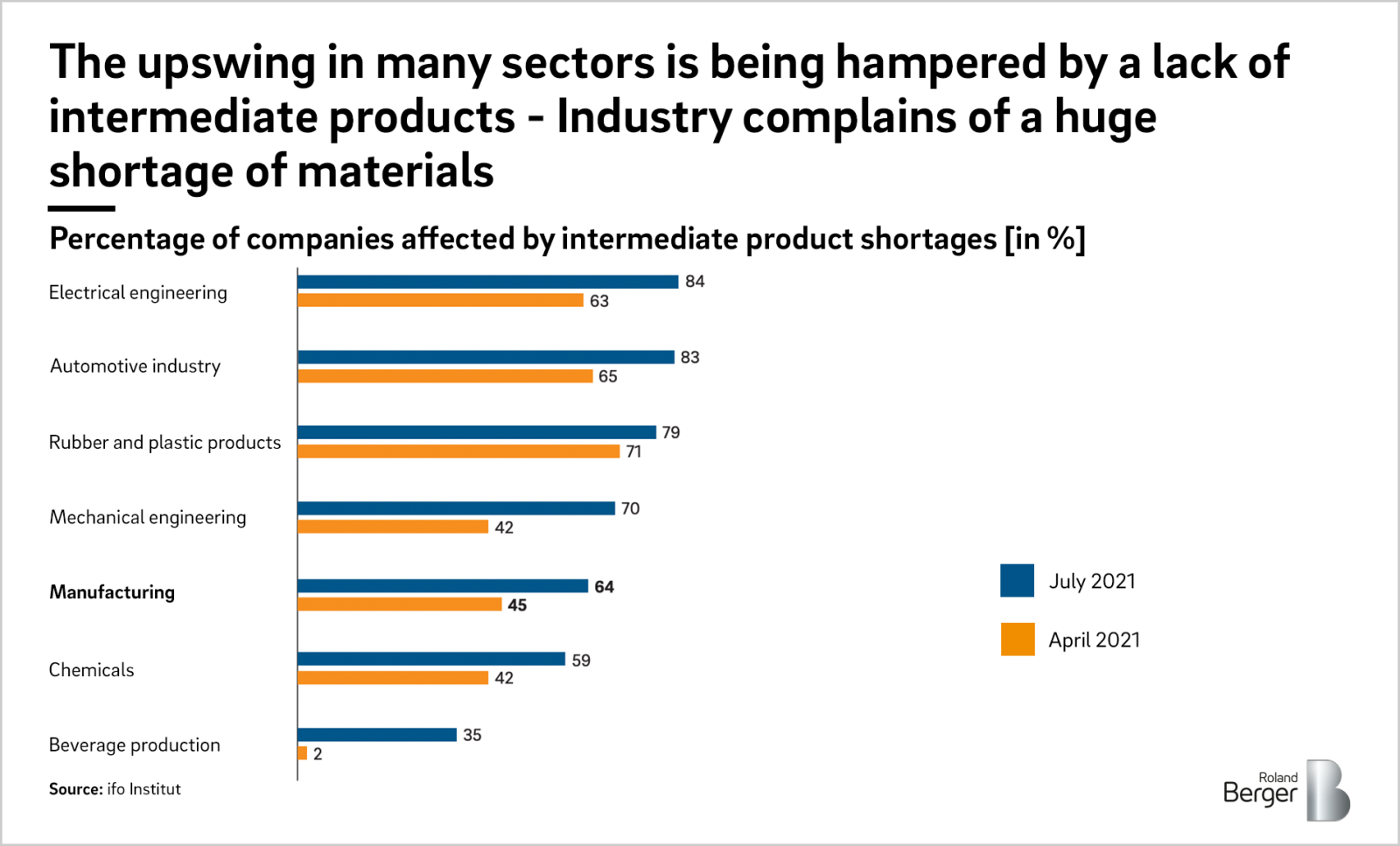

The manufacturing industry nevertheless gives cause for concern. According to one Ifo Institute survey, nearly two thirds of its players are reporting a shortage of intermediate products. Car makers in particular have had to scale back some aspects of production for lack of urgently needed semiconductors. These bottlenecks are likely to persist into next year.

The shortage of intermediate products is already feeding through into rising producer prices, with the cost of these products increasing by 12.7% year on year. Energy prices too are up by 16.9% on average, partially because of base effects and the newly introduced CO2 tax. Given that producer prices are generally seen as an early indicator of the trend in inflation, economists fear that at least a portion of price hikes in the coming months will filter through into consumer prices, causing the inflation rate to increase further – despite the fact that consumer prices have already risen faster than at any time in the past 30 years. The year-on-year inflation rate in July stood at 3.8%.

The good news is that, despite all the restrictions, the German economy could return to pre-crisis levels as early as the third quarter – especially if, in the context of measures to control infection, existing economic restrictions are lifted as expected by the end of the third quarter. If that happens, there is theoretically no reason why the retail and service sectors should not recover. Private consumption spending would once again be the mainstay of projected growth.

The bottom line is that we see the upswing on a shaky foundation. Whether and to what extent the economy does recover largely depends on what happens with the pandemic going forward. It thus comes as no surprise to find this uncertainty mirrored in the widely varying forecasts put forward by economic institutions. Pessimistic estimates put economic growth this year at just 2.7%, whereas the more optimistic forecasts point to growth of 4.0%. On average, the respondent economists anticipate GDP growth of 3.3%.

This study analyzes Germany’s economic development in 2021 and looks ahead to the coming months.

_tile_teaser_h260.jpg?v=1687234)