Volatile prices are posing challenges to companies across the sugar sector. Our Pricing Excellence program helps industry players enhance competitiveness.

Transformation in the European sugar industry

Challenges, opportunities and a framework for success

The European sugar industry finds itself at a pivotal juncture. Facing falling demand, changing consumer preferences, structural challenges and a raft of global headwinds, it must transform to survive. Our report explores the transformation options available to sugar producers. It looks critically at the challenges and potential opportunities they present, from diversification into emerging non-food markets such as biofuels, to embracing a demand-driven approach that turns producers into valorization engines.

The world’s appetite for sugar is insatiable. Whether as a sweetener in food and beverages, industrial feedstock or raw material for biofuels, growing populations and rising income levels are driving consumption to record highs. This should be good news for the European sugar industry. Tighter regulations, declining demand and changing consumer preferences are combining with global challenges such as volatile prices and disrupted supply chains to severely test the industry’s value model. It’s clear that change is now urgently needed. The question is, how?

"By embracing innovation, diversifying product portfolios, and shifting from supply-driven thinking to a demand-driven approach, European sugar producers can emerge as leaders in a new era of sustainable, value-added growth."

This report explores the key insights and strategic imperatives that will define the future of the industry. It looks in depth at the global and European sugar markets, the challenges the European industry faces and the opportunities for transformation, including innovation, diversification and demand-driven approaches. The report ends with a series of recommendations for European producers, based on Roland Berger’s strategic framework for transformation.

The sugar market is facing disruptive changes

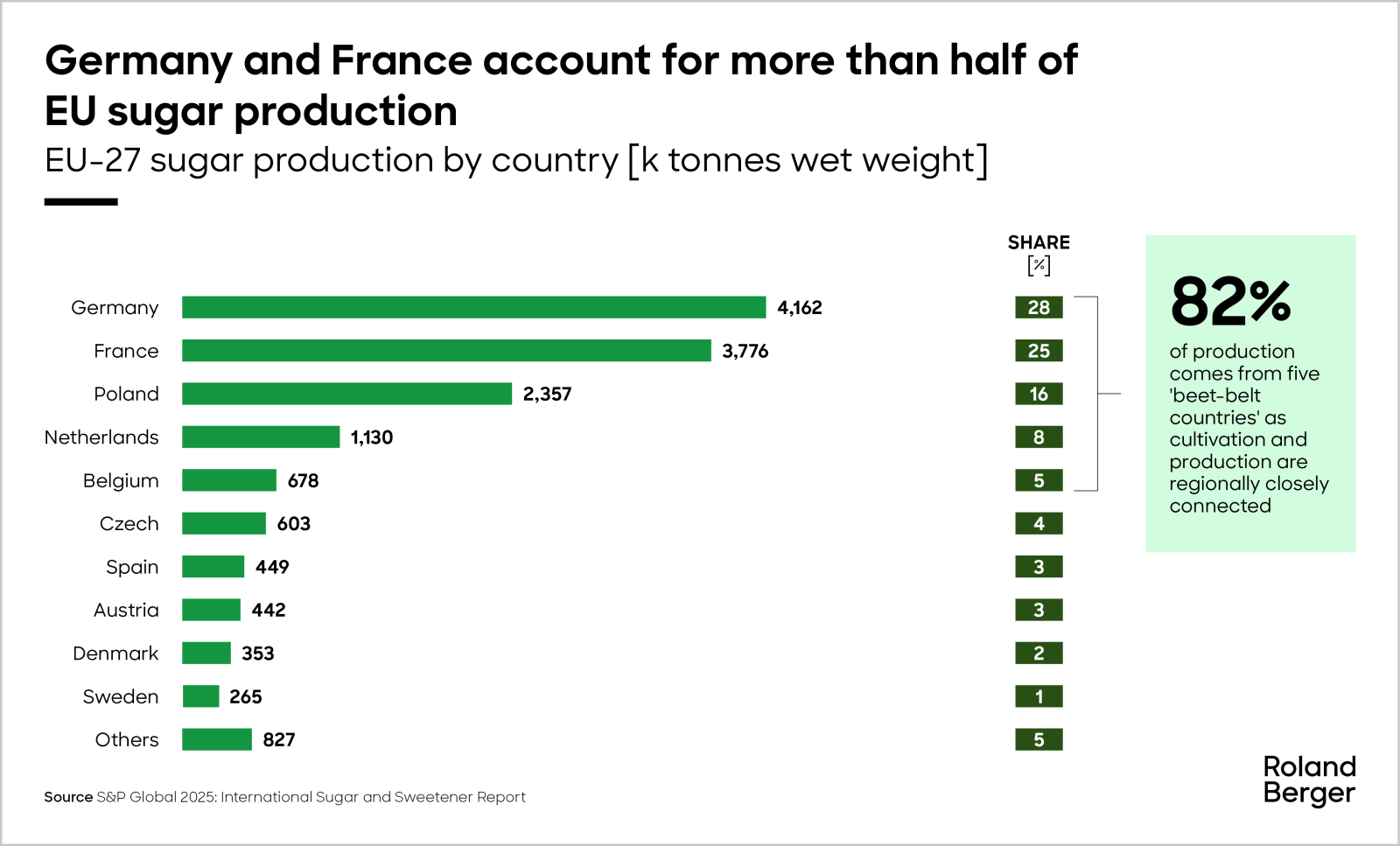

The global sugar market is expected to grow at a compound annual growth rate (CAGR) of 5.2% through 2029. But this growth will be unevenly distributed, with different regions performing at different levels. While Asian-Pacific countries such as India, China, Thailand, and Indonesia are driving overall consumption growth thanks to their burgeoning populations, developed countries have reached a saturation point. Health trends, regulatory pressures, and the proliferation of low- and no-calorie sugar alternatives are curbing demand, especially in Europe, a key sugar beet producer. Price volatility, caused by factors such as climate events and geopolitical tensions, is exacerbating the problem. The benchmark price of raw sugar fell by around a third to roughly 400 EUR per tonne between 2023 and 2025, for example. And in Europe, while the market is concentrated in just five countries (France, Germany, Poland, the Netherlands, and Belgium are responsible for 82% of production), production sites are highly fragmented, squeezing profitability.

"The industry must move beyond traditional boundaries, embracing an end-to-end valorization model that maximizes the value of every output and by-product."

As a result of these challenges, Europe is already running a sugar surplus. An oversupply of one million tonnes is expected in 2025/26, and the problem is only likely to increase in the coming years. Producers are therefore looking to valorize the by-products of sugar beet production, such as beet pulp and molasses, and find new markets, especially in the non-food industry. This offers significant potential: Most sugar in the European Union (77% of total volume in 2023/24) is sold to food and drink manufacturers, whereas only 3% reaches the non-food market (biofuels, biogas, paper, bioplastics, fertilizers, chemicals, and cosmetics).

The main part of the report looks at the options producers have to exploit such opportunities. In particular, it outlines strategies to diversify sugar production away from the falling demand for refined sugar and into new areas to capture growth. These include sugar alternatives, such as nutrition solutions; alternative sweeteners, for example the growing market for natural sweeteners such as stevia; fermentation, which can be used to produce a myriad of in-demand food and other ingredients from sugar; and biochemicals, such as bioethanol and natural plastics. Other strategies outlined include managing price volatility, insecure sourcing, regulations, investment and consolidation opportunities.

Lead the change

The recommendations section of the report provides strategic responses and leadership imperatives to guide industry stakeholders through the market transition. It focuses on achieving the required shift toward demand-driven, end-to-end thinking, in which players not only process sugar but also maximize the value of every output, by-product, and partnership. Roland Berger’s strategic framework for sugar producers forms a core part of this, detailing a roadmap approach that ensures resilience, growth, and long-term value creation. The report also provides a practical four-step plan to implement the roadmap and wider transformation.

The report concludes with a series of key takeaways for leaders, from prioritizing strategy and sustainability to building alliances with stakeholders and investing in new capabilities. For more information, download a copy of the report or contact one of our experts.

Request the full PDF here

Register now to access the full study. Furthermore, you get regular news and updates directly in your inbox.

Further readings