The latest innovations in technology, AI, and software solutions for industries including automotive, industrials, and energy, allowing businesses to adapt their operating models, strategy, organizations, and processes.

Battery Monitor 2022: An overview of the battery market

The market for batteries is growing, creating new challenges in sustainability and availability of raw materials

In this first in a series of articles covering the chapters in the Battery Monitor 2022 report, developed by the Production Engineering of E-Mobility Components (PEM) unit of RWTH Aachen University and Roland Berger, we look at the battery market. While sustainability, availability of raw materials and future overcapacity are major challenges, technological progress, especially around specialized products, is helping to mitigate these threats and ensure market growth.

"Europe and North America are currently focusing on nickel-based materials, so will likely stick to the technology."

The battery market has transformed in the past couple of decades, driven by the fast-growing electric vehicle (EV) market and demand for ever-more powerful batteries. We believe that three key performance indicators, based on the life-cycle phases of lithium-ion batteries (LiBs), help to best define its current characteristics. These are sustainability, technology performance and market competitiveness. Below we outline the full report’s findings on each.

Sustainability: Regulations set to bite

Largely as a result of the EV boom, LiB battery production has soared. This is putting pressure on raw material availability and placing the entire battery life cycle under increasing scrutiny. Sustainability is now becoming a key priority for market players.

The phasing out of the internal combustion engine (ICE) – which several countries, including Germany, the UK and Canada have already announced – will have a huge impact. It is discussed in later articles in this series. Battery regulation, especially in Europe, will also affect sustainability. In particular, there is a push to lower battery-related CO2 emissions and increase the share of recycled materials used in production. The European Union’s (EU’S) Battery Directive, for example, proposes an incremental increase in the recycled share of some key battery materials, such as 12% for nickel by 2035.

The EU’s Carbon Border Adjustment Mechanism (CBAM) could also affect the European battery value chain. Beginning in 2023, it will levy an import tax on emissions “embedded” in imported goods, such as metals produced outside the EU. If battery materials are covered, which is currently uncertain, CBAM could push up the price of cathode active materials by up to USD1.60 per kilogram.

Technology performance: Specialized products take off

There are several general trends in LiB development, covered in detail in the full report. The first involves the proliferation of cells for specialized products.

To date, most batteries used in new applications have been derivatives of existing cells. But the growing and maturing market now offers a stronger platform to cost-effectively produce entirely new systems for novel and existing uses. Batteries for the electric vertical take-off and landing (eVTOL) aerospace industry are a good example. These aircraft have rapidly advanced in the past few years, and typical consumer cells no longer meet their energy and power density needs. Instead, high-performance cells with features such as high-silicon anodes and pre-lithiation are being specifically developed and produced for eVTOL applications, as a critical demand of multiple GWh is reached.

"Installed overcapacity will lead to low utilization and ultimately low returns. Consolidation, as well as stranded investments, are likely. Players without significant battery experience face the strongest challenges."

With resources at apremium, another general trend is markets’ efforts to secure their supply of materials, which will lead to lock in effects. For example, Europe and North America are currently focusing on nickel-based materials and battery players secure this material via long-term agreements or direct investments, so will likely stick to the technology as they know they can recycle the nickel in the future. Indonesia, meanwhile, has legislated to ensure that most of its local available raw materials, such as nickel, can only be processed in country. A closed-loop project with CATL, for example, requires the battery giant to process 60% of its nickel on Indonesian soil.

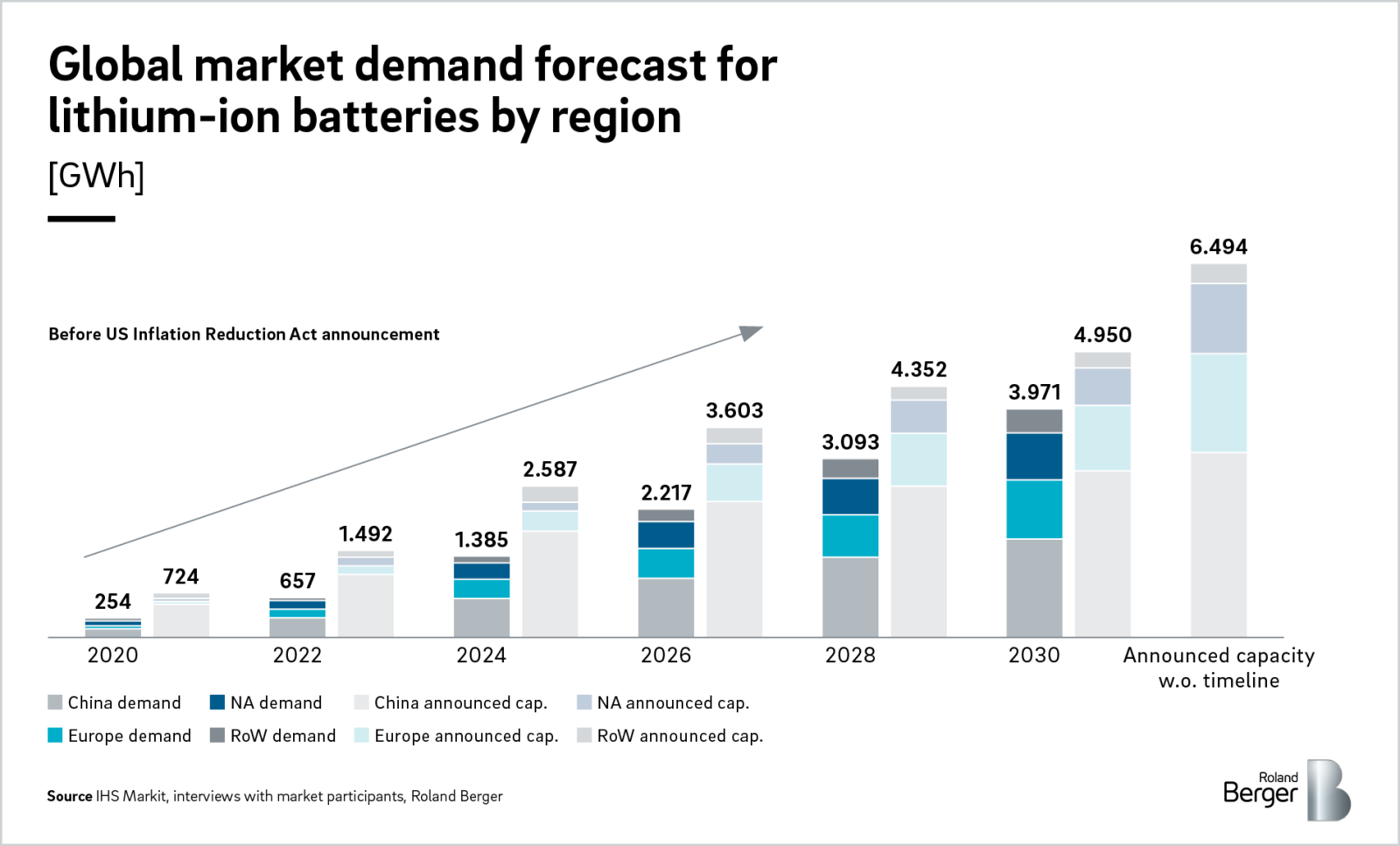

Competitiveness: Overcapacity looms

The LiB market is in danger of becoming overheated. Demand is insatiable, especially from the EV market, and producers are at the limit of their capacity to meet it. However, as more and more producers emerge, overcapacity will become a problem. The EV industry is forecasted to account for 90% of global battery demand in 2030, equivalent to four terawatt hours (TWh). However, announced global capacity for 2030 is more than 6 TWh by now. While demand forecasted are constantly adjusted to higher numbers, this initial announced installed overcapacity will lead to low utilization and ultimately low or negative profits. Consolidation, delay as well as stranded investments, are likely – as the battery industry also faces a huge war on talent.

An expected undersupply of raw materials, especially nickel, will be another major challenge. China has long been the global leader in refining, with around 70% of lithium and 30% of nickel processed there. This gives the country a significant competitive advantage. To counter it, there is a growing push towards localization, with governments regulating to ease battery producers’ reliance on China. In Europe, this includes the EU’s Battery Directive and CBAM. In the US, a “Buy American” strategy has seen tariffs of up to 25% placed on Chinese-produced battery cells, minerals and other materials, while the Inflation Reduction Act (IRA) of August 2022 offers further incentives for local sourcing, with up to USD12,000 of tax credits for Evs and their batteries.

For more information on all of these battery market topics, please download the Battery Monitor 2022 report. You can also contact us directly to discuss specific topics like specific market sizing, IRA impact on manufacturing and souring of cells and materials, cell and CAM should-cost estimation, or LiB recycling.

Download the full PDF

Register now to download the full BATTERY MONITOR 2022 - the value chain in the field of tension between economy and ecology - including key insights and latest developments regarding the current market situation for players in the battery industry. Additionally, you get regular insights into electronics topics.

All publications from this series

Further readings