Roland Berger is a thought leader in environmental issues and the response demanded from organizations. Our publications cover all relevant areas.

Clean energy and the reshaping of global value chains

By Torsten Henzelmann and Dieter Billen

How countries that pursue green energy policies put themselves at a competitive advantage

RELATED EXPERTISE

Over the last few decades, many multinationals have globalized their value chains, relocating their manufacturing operations to lower-cost destinations that offer abundant labor and more attractive input costs, including cheaper energy. Emerging markets have benefited greatly from this globalization. They have invested in major infrastructure projects, such as large-scale power generation facilities and grid infrastructure, to support the rapid inflow of manufacturing FDI (foreign direct investment). Until recently, these investment projects were mainly built around fossil-based electricity, such as coal.

But these policies of cheap fossil-based energy have come at a tremendous cost to the environment. According to figures from the International Energy Agency, Asia's electricity production based on coal increased from 990 TWh in 1990 to 7,332 TWh in 2018, for instance. Unsurprisingly, in 2019 – before the COVID-19 pandemic – the region accounted for 55 percent of global CO2 emissions, or 20 billion out of a total of 36 billion tons.

Now, however, the tide appears to be turning. As the fight against climate change becomes a global priority, countries are realizing that pursuing clean energy policies can put them at a competitive advantage internationally. Most countries are now moving away from their old-fashioned policies based on fossil fuel. Providing green energy has become the new paradigm.

Rebalancing value chains

Global value chains are being reshaped. In the past, multinationals tended to set up their plants in well-known manufacturing hubs such as China, Bangladesh, Eastern Europe or Mexico. But countries such as Vietnam, Indonesia, India, Colombia and parts of Africa are now emerging as manufacturing hubs. Europe and North America are also becoming increasingly attractive as manufacturing investment destinations again as a result of developments such as the rise of "Industry 4.0" (automation based on smart technology) and new labor-replacing technologies.

The choice of which country to locate your manufacturing operations in depends on a number of factors, of course. Increasingly, access to green energy is becoming a major factor in such decisions – for reasons that we discuss below.

"CO2-free power generation from renewables increasingly becomes a competitive advantage for emerging economies."

Senior Partner, Managing Director Central Europe

Frankfurt Office, Central Europe

The clean energy factor

Sustainability and decarbonization have moved up the corporate management agenda. Many multinationals are making strong commitments to decarbonization, several even pledging to become carbon-neutral. The NewClimate Institute reports a threefold increase in the number of businesses setting net zero goals, from 500 at the end of 2019 to 1,565 in October 2020. Driving this shift from fossil fuels to renewables is, on the one hand, pressure from customers, employees, investors and financers. On the other, there is the fact that choosing clean energy is in itself becoming more attractive, as the cost of generation and storage falls.

This shift in priorities is making countries that have a high share of renewables in their energy mix increasingly attractive for multinationals. Such countries can now position themselves as clean investment destinations, helping companies meet their decarbonization commitments, especially in the case of energy-intensive activities such as manufacturing or running data centers. As the cost of clean energy rapidly falls, this does not need to come at an additional cost compared to fossil fuels: Renewables have already reached grid parity in most countries or are expected to do so in the next few years. In addition, from an investor's point of view, a CO2-free energy supply is less risky in times of rising CO2 prices. Europe's carbon border tax plan would further boost the attractiveness of clean energy countries for manufacturing.

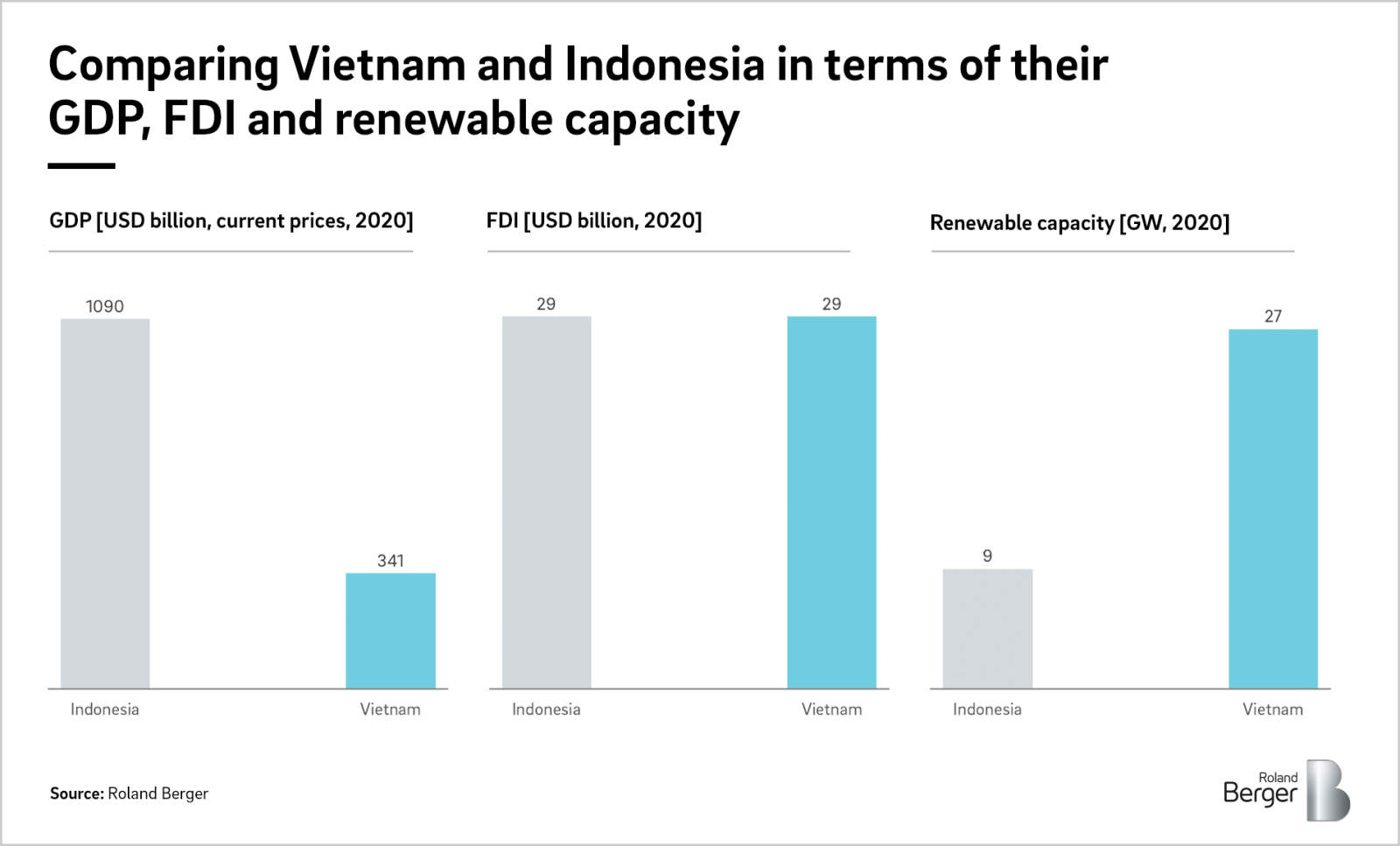

Case study: Vietnam vs. Indonesia

Vietnam and Indonesia are both emerging as major manufacturing hubs in South-East Asia. However, Vietnam has so far been more successful than Indonesia in attracting foreign direct investment (FDI), proportionate to its size. Thus, while Indonesia' economy (USD 1.1 trillion in 2020) is significantly larger than Vietnam's (USD 341 billion), the two countries' levels of FDI are similar at around USD 29 billion in 2020.

Vietnam's success is due to a number of factors. In addition to its strong infrastructure and location, it is also moving aggressively towards renewables – unlike Indonesia, whose renewable energy capacity including hydroelectric power is just 9 GW, one-third that of Vietnam's. For example, Vietnam experienced a 25-fold increase in solar generating capacity in 2020 alone. Wind power is also expected to take off soon in Vietnam, with forecast capacity by the end of 2021 greater than that of Thailand, Philippines and Indonesia combined.

Indonesia lags behind Vietnam in terms of renewables, as well as attracting FDI. Yet, the country has vast potential for green energy, including large-scale and small-scale solar. It can also produce hydrogen from fossil fuels, such as gas with carbon capture ("blue hydrogen"), leveraging its coal beds for carbon storage, and in the longer term produce hydrogen from renewable sources ("green hydrogen").

Attracting foreign investment

Many countries are already well aware of the competitive advantage that they can enjoy by pursuing clean energy policies. China, the world's largest manufacturing country, which has historically relied heavily on coal power, has pledged to become carbon-neutral by 2060. It is moving fast and aggressively on decarbonization: According to BloombergNEF, China built more new wind capacity in 2020 than the whole world combined in 2019.

This is an opportunity for emerging markets, some of which – but not all – are already moving towards renewables. It is also a chance for Europe and North America to adopt clean technology and position themselves as green investment destinations, bringing back some manufacturing value chains from overseas.

Opportunities abound

For multinational companies, the rebalancing of global supply chains presents them with a wider range of investment destinations to choose from than in the past. The availability of renewable energy will be an increasingly important criterion in their investment destinations. Indeed, it is not just the share of renewables in the energy mix of the country that is significant: Companies also increasingly rely on decentralized solutions, for example, on-site solar, wind or biomass generation, or procure energy directly from suppliers through corporate power purchase agreements (PPAs).

For countries, clean energy is becoming a key factor in attracting multinational companies keen to meet their own sustainability goals. Individual countries should not miss this golden opportunity to leverage renewables and put themselves at a global competitive advantage.

Sign up for our newsletter

Sign up for our newsletter and get regular insights on newest publications related to Energy & Utilities.

Further readings