Electric vehicle charging

Explore challenges and opportunities in the EV charging market. Learn how industry players are competing for profit pools and innovating to meet rising demand.

Norway remains one of the world's leading EV nations and edges up to second in our latest EV Charging Index, as EV sales rates continue to grow. Meanwhile, Sweden moves up slightly to 10th, with public charging infrastructure and user satisfaction improving. Here, we compare the two countries, highlighting both similarities and differences as Sweden looks to learn from its neighbor.

Sweden endured a challenging year for EV sales in 2024, with a 9% drop compared to 2023. However, the sales penetration rate only slipped from 61% to 60% – still comfortably the second-highest in our Index, behind Norway. There are signs that things are picking up in 2025 as Sweden's sales volumes rise again.

"Lower running costs compared with ICE vehicles is now the biggest EV purchase driver in Norway and Sweden."

Across the border, Norway recorded a 3% increase in EV sales, as the sales penetration rate rose to a massive 93%. Battery electric vehicles (BEVs) are dominant, representing 97% of all new EV sales in 2024. The government's aim is for all sales of new cars in 2025 to be zero-emission vehicles.

Norway and Sweden have long led the rest in terms of EV sales penetration rates, but Norway's longstanding commitment to electrification is reflected in the greater size of its electric car parc: just over a quarter of all cars in Norway (27%) are now BEVs, while in Sweden this figure is 7%.

Still there are many similarities in the reasons behind drivers going electric in Norway and Sweden. Lower usage costs and maintenance costs compared with an ICE vehicle is now the main factor in Sweden (named by 61% of respondents) and Norway (59%).

Home charging is important in both markets, but Norway's EV drivers are particularly reliant on it: according to our survey, 73% of miles driven are charged at home – well above the global average of 55% and European average of 56%. Sweden's EV drivers charge 62% of their miles driven at home.

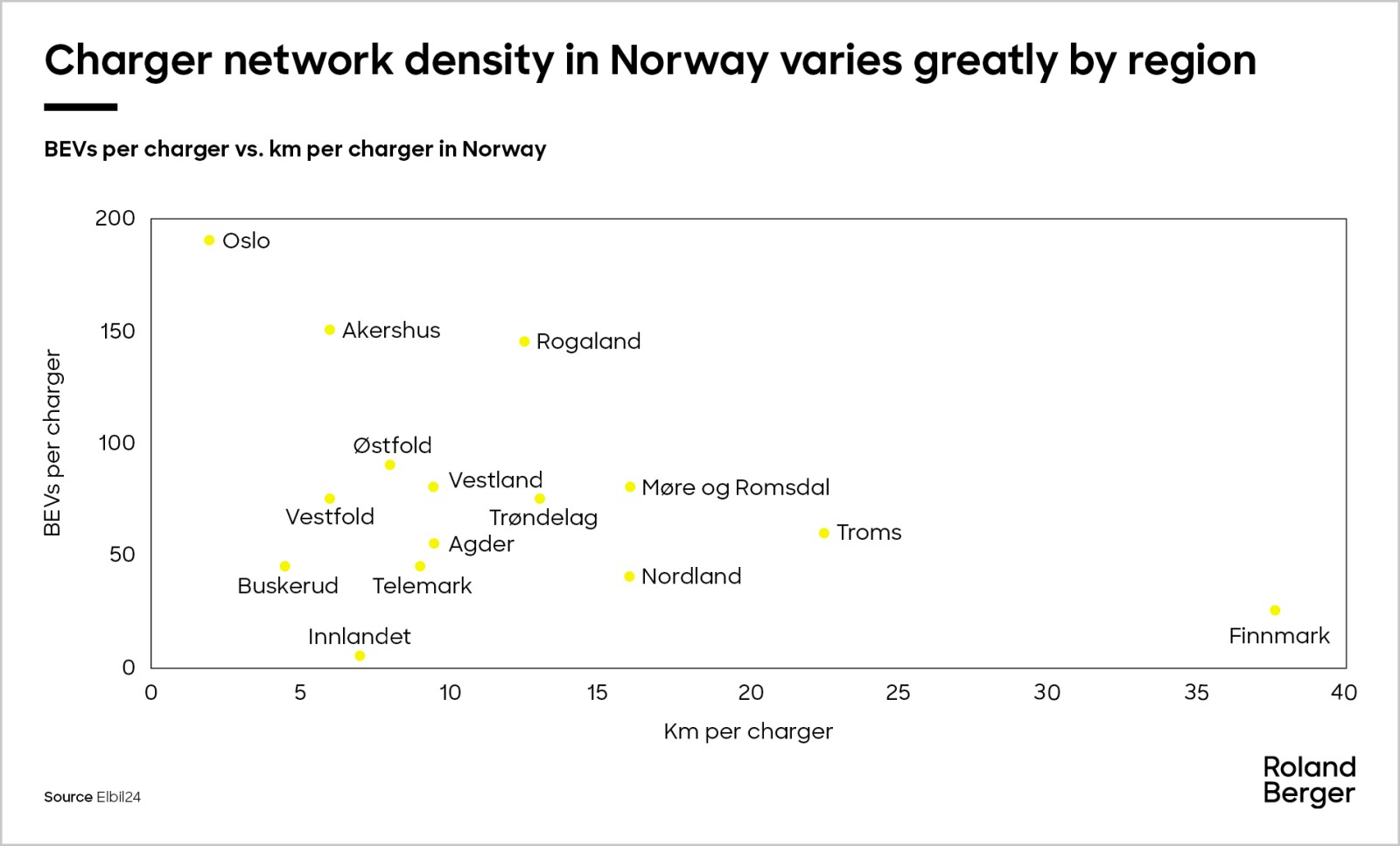

This partly explains why public charging infrastructure sufficiency remains poor in Norway: there are 34 EVs per public charging point, which is well behind the European average of 14. Growth in public charging infrastructure has been slow, measuring just 5% in 2024 – a long way off from the 35% average in Europe.

By contrast, Sweden is showing signs of improvement. Public charging infrastructure grew by 34% in 2024, and its ratio of EVs to public charging points improved to 15.

Where Norway does lead Sweden in public charging is its greater prevalence of faster DC charging points. Almost half of Norway's public charging points are DC (45%) – much higher than the 16% in Sweden. This is reflected in user sentiment: two-thirds of survey respondents in Norway (66%) feel public charging speeds are generally fast enough, compared with just over half in Sweden (55%).

Norway and Sweden are both offering subsidies to support charging network expansion, particularly for larger electric vehicles such as trucks.

In Sweden, there are subsidies available for tenant-owners' associations and businesses when installing chargers for tenants or employees. These represent up to 50% of the CAPEX or SEK 15,000 (EUR 1,400) per charging point. There is also a subsidy for private users comprising 50% of charger installation and material costs.

Norway also offers subsidies for tenant-owners' associations and private parking operators in some regions, providing up to NOK 15,000 (EUR 1,300) per charging point. There are no subsidies for private users for charger CAPEX; however, there are subsidiaries for smart energy controls.

Satisfaction levels with the overall charging experience are fairly comparable across both countries. In Sweden, 88% of respondents feel satisfied or very satisfied, with this metric at 90% for Norway. The percentage of people feeling very satisfied has increased considerably in the last two years, likely due to the increase in public charging stations and charger capacities.

For EV drivers in both markets, the least satisfactory aspect of EV charging is the charge time. This is followed by insufficient public charging infrastructure, although this is more of an issue in Sweden than in Norway.

"Charging-point operators must differentiate via quality, uptime and location, rather than pure expansion."

Charging market dynamics vary across Sweden and Norway.

In Sweden, charging network growth is currently outpacing growth in EV sales. We expect various implications for charging-point operators (CPOs), as focus will shift to differentiating via quality, uptime and location, rather than pure expansion.

Price competition among CPOs is set to increase, with price differences across networks already considerable: prices for 150 kW-plus chargers, for instance, can range from SEK 1.80 to SEK 6.80 per kWh.

CPOs are exploring new retail formats. Circle K recently opened a charging location in Gothenburg with ultra-fast EV chargers only (no gas pumps) as well as a convenience store. Improving the payment experience in line with the EU's Alternative Fuels Infrastructure Regulation is also a focus. CPO Recharge has enabled card payment at all fast chargers in the Nordic region, for example.

Meanwhile, Norway's large BEV fleet may make the utilization risk for ultra-fast chargers relatively low, but here, too, CPOs must focus on differentiating via uptime, queue management and attractive retail offers. However, the needs differ by region e.g. as its easier to find chargers (shorter distance between each charger) in southern areas such as Oslo, Akershus and Rogaland, yet much more difficult to find chargers that are not busy.

Sweden and Norway are increasingly turning their attention to electrifying heavy-duty road transport.

While sales numbers remain relatively low, growth is starting to accelerate rapidly. Norway saw 371 electric trucks (12-plus metric tons) sold in 2024 and Sweden has already seen 302 units sold in the first seven months of 2025 – after just 97 in the whole of 2024. For Sweden, this represents around 8% of all new truck sales.

This rapid ramp-up means the rollout of charging stations for electric trucks is also gathering pace. Between 2022 and 2024, approximately 60 charging stations for electric trucks were built in Sweden; by the end of 2025, Sweden plans to expand this to 250, with the forecast for 1,000 by 2030.

To support this expansion, the Swedish Energy Agency recently announced SEK 600 million (EUR 55 million) in funding for new truck charging facilities.

In Norway, the government has allocated NOK 1.2 billion (EUR 100 million) to subsidize electric truck purchases. However, prices remain prohibitively high for many, and industry associations have called for greater political action to improve the business case for investing in electric trucks.

Register now to to discover the latest insights, emerging trends and upcoming challenges in the EV and EV charging markets.