EV Charging Index 2025: Steady progress

Despite tough market conditions, global EV use and charging infrastructure showed continued steady growth in 2024. Learn more in Roland Berger’s latest EV Charging Index.

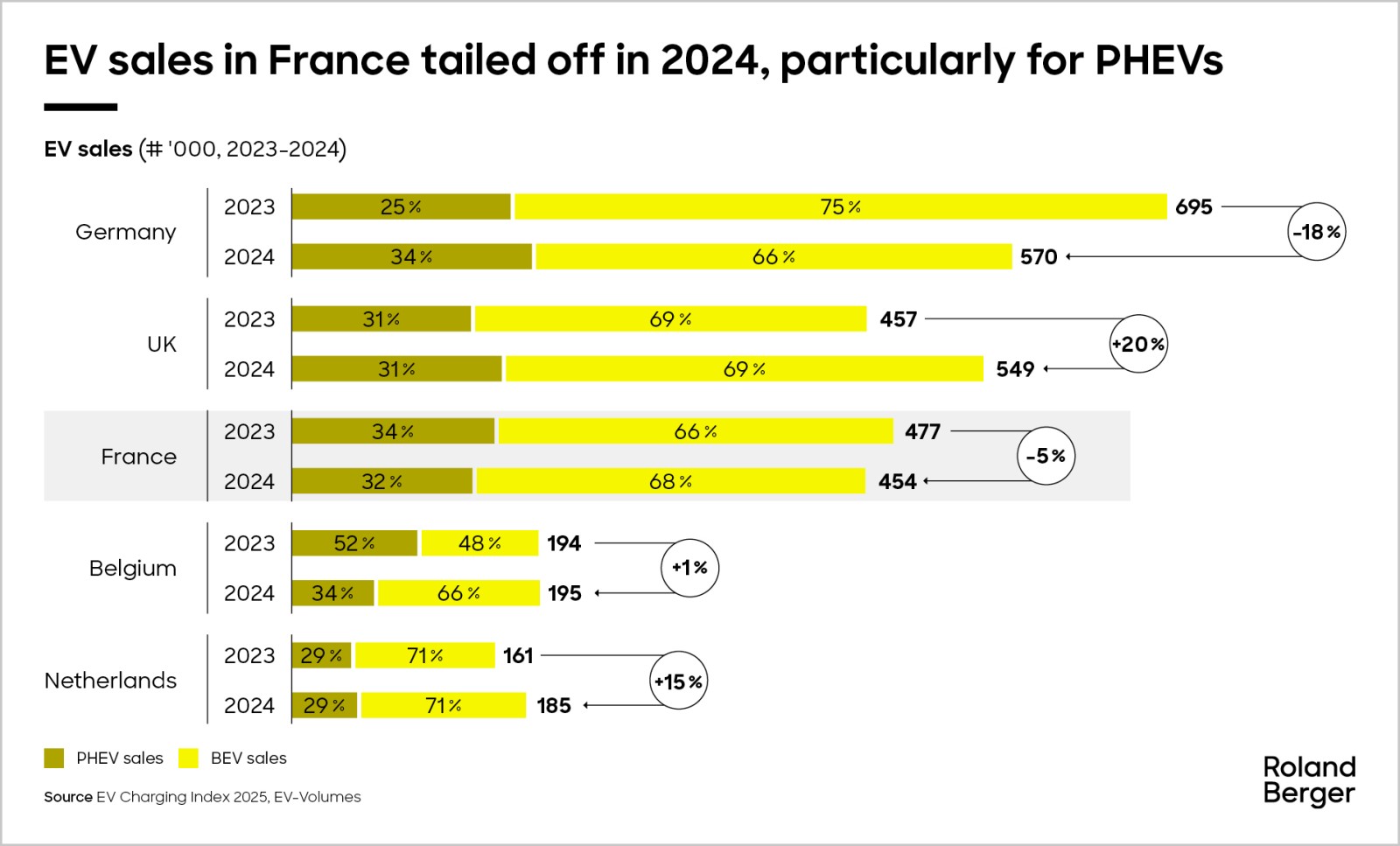

France continues to make good progress in mobility electrification and now ranks eighth in our EV Charging Index. EV sales fell slightly in 2024 in absolute value, but the sales penetration rate stayed the same. Public charging infrastructure growth is encouraging, though the markets are not yet clearly differentiated between slow and fast charging, probably preventing a faster development of the mass market, which would be supported by a cheaper slow-charging segment

After a major jump in EV sales during 2023, France suffered a slight drop in this metric during 2024 (-4.7%) thanks to lower government subsidies and stricter eligibility criteria. However, widespread macroeconomic concerns meant this was consistent with general stagnation in the auto market, ensuring the EV sales penetration rate remained steady at 26% – just above the European and global average of 25%.

Environmental protection remains the primary purchase driver for EV users in France, with 54% of respondents citing it as the main reason to get an EV, higher than the European (47%) and global (46%) averages.

However, EV drivers in France seem less convinced by the economic benefits of going electric. According to our survey, only 54% believe the cost per kilometer is lower than in an ICE car – below both the European (59%) and global (61%) averages. Similarly, only 36% of EV users in France identify lower usage and maintenance costs as a key purchase driver, compared with averages of 43% in Europe and 47% globally.

"Fast charging is important, but a distinct market for slow charging still needs to be developed. It should be much cheaper."

According to our survey, the share of high-mileage BEV users in France (15% driving over 20,000 km annually) is slightly below the European (17%) and global (19%) averages. However, daily use patterns are encouraging: 44% of French BEV users drive their vehicle almost every day – on par with the European average (44%) and close to the global benchmark (46%), outperforming Belgium (42%), the Netherlands (35%) and the UK (36%), but trailing Germany (52%).

These figures suggest France is in a transitional phase of EV adoption: while long-distance use remains limited, regular daily usage is becoming more established. This signals untapped potential for broader usage and deeper market penetration, especially as future improvements in battery range and charging infrastructures help overcome current limitations

When it comes to charging habits, BEV drivers in France are broadly in line with their European and global counterparts, with some slight variation.

Two-thirds of respondents in France (67%) use a private home charge point, while 17% of BEV drivers have no access to a home charger – almost identical to the European averages (66% and 17%, respectively). On a global level, these metrics are 64% and 15%.

BEV drivers in France are slightly more reliant than average on home charging: 60% of miles driven are charged at home, a little above the European (56%) and global (55%) averages. A quarter of miles driven are charged using public facilities, with shopping centers and highway charging the most popular.

The overall charging experience in France has improved significantly. In Edition 5 (2024), just 75% reported feeling (very) satisfied with general EV charging, but this rose to 92% in our latest edition – just above average on both a European and a global level.

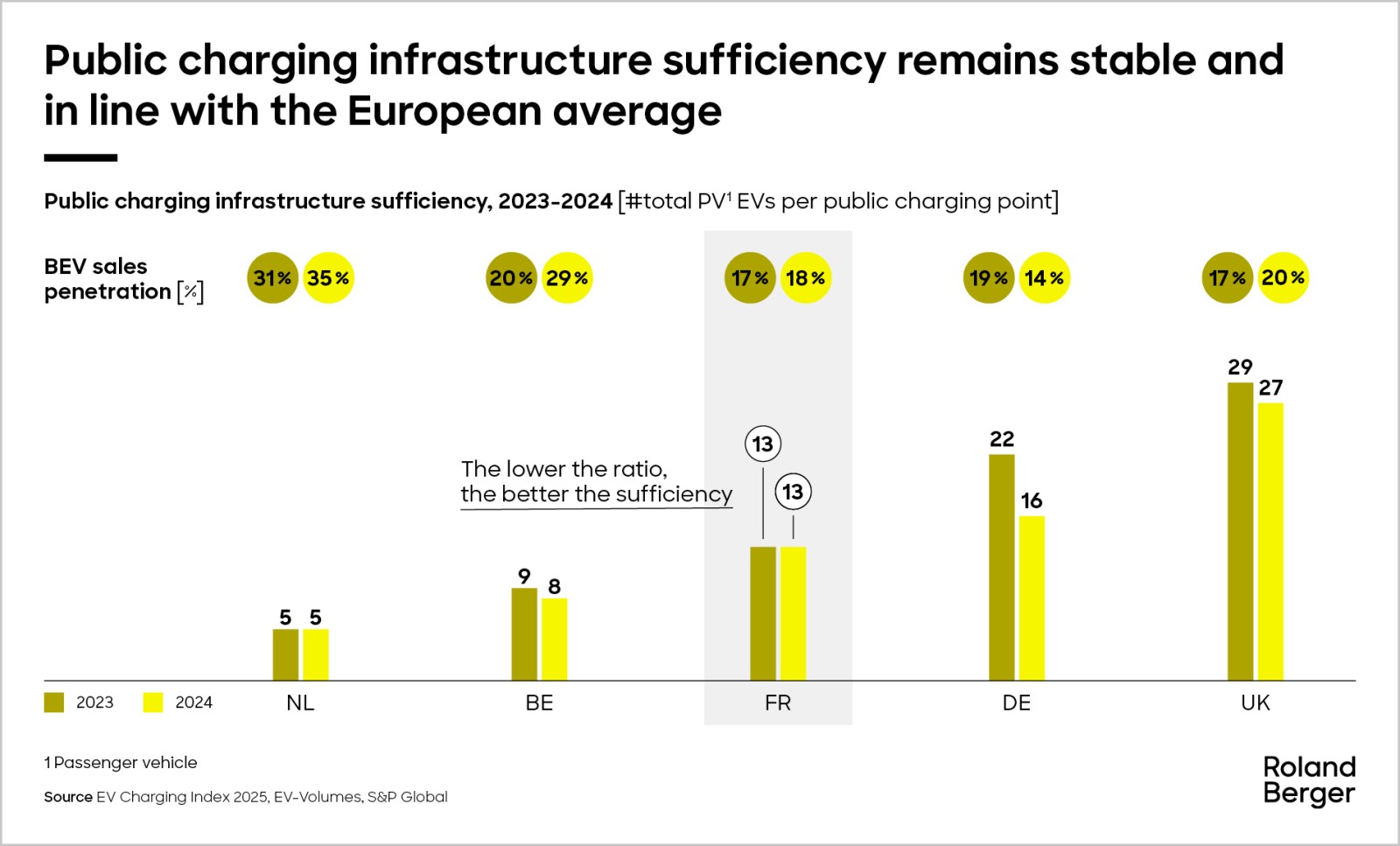

As with most markets, charge times and public infrastructure sufficiency remain the key concerns. France scores averagely here, according to our survey.

Growth in France's public charging infrastructure was solid at 31%, which is just below the European average of 35%. It's a similar story for the ratio of vehicles to public chargers, which remained steady at 13 – again, consistent with the European average.

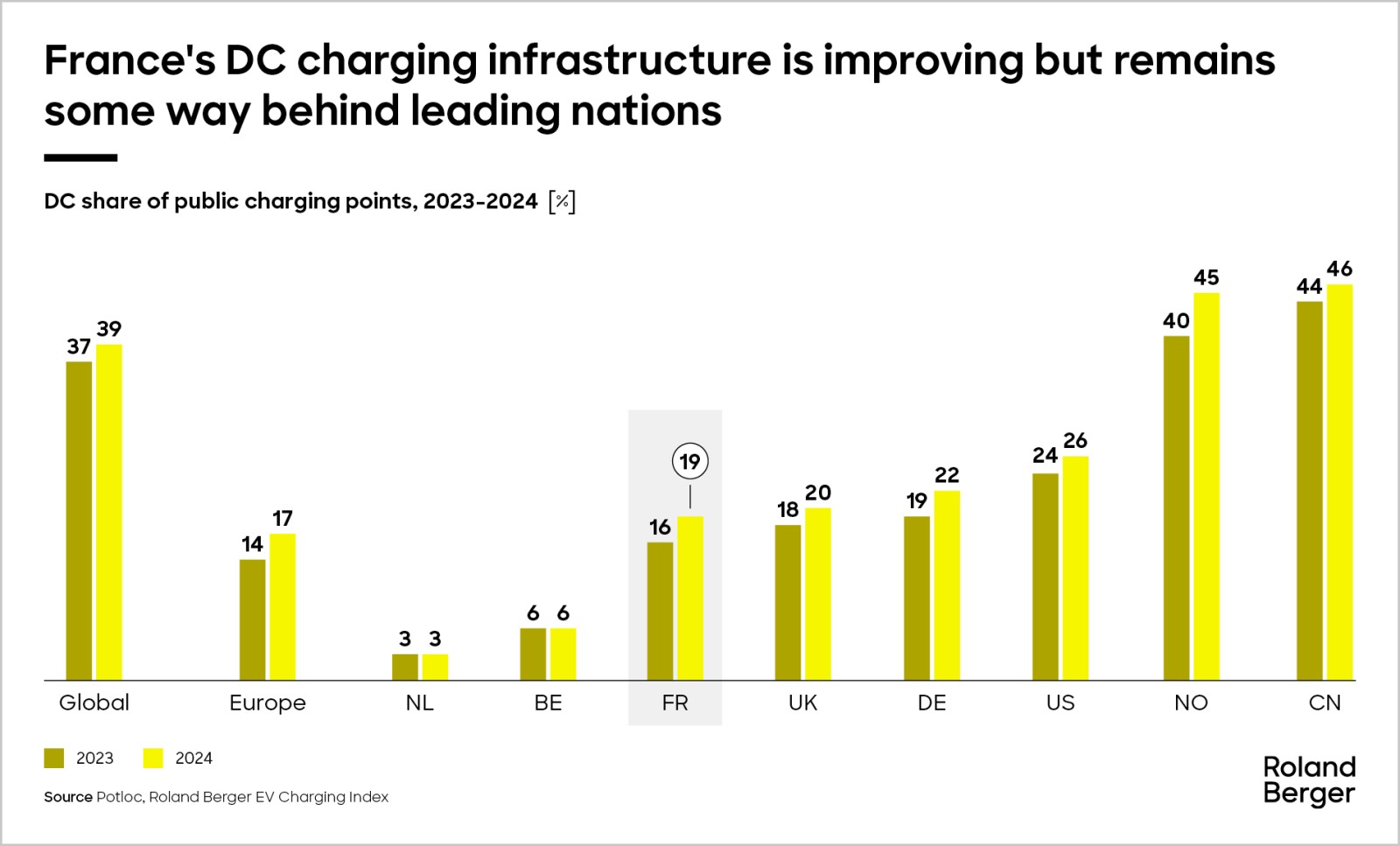

Meanwhile, the percentage of faster DC chargers in France's public charging network edged up to 19%. This is just above average for Europe (17%), but ranks poorly on a global scale, where the average is 39%, driven by strong ratios in Asia-Pacific and the Middle East.

In terms of charging speed, 61% of French EV owners feel satisfied with public charging times – almost identical to the European and global averages of 60%. This is a major improvement on the previous year, when this metric was just 38% – a trend seen across Europe as more DC charge points are installed.

When it comes to charging sophistication, however, France has work to do. In contrast to other comparable markets, its share of non-smart home chargers is growing and is now 54%. By comparison, neighbors Germany (40%), the Netherlands (33%) and Belgium (38%) have a much lower share of non-smart home chargers.

Meanwhile, concerns over charging costs remain, with 36% of EV drivers in France saying public charging should cost less. This is slightly above the global average of 33% but lower than some neighboring countries such as Germany (38%) and the UK (45%).

The highly volatile price of electricity has become a key differentiator among charge point operators. Negotiating favorable contract terms and managing price risk on this front is a crucial success factor. It's not yet clear whether this favors integrated players, such as subsidiaries of major utilities, or whether pure players can succeed with more agility.

Ultra-fast charging is attracting significant investment, particularly on highways as it addresses a key user need, but there is little price differentiation with slow charging. Even though the share of fast charging should continue rising, there is potential to develop a market for slow charging, offering much cheaper charging, especially for the "destination" use case, such as shopping malls or supermarkets, and for owners of smaller, more affordable EVs.

In addition to private consumers, EVs are also gaining traction in the B2B segment.

Here, we believe business models that center their value proposition around well-designed fleet-management features, such as optimizing EV usage, generating revenue from flexibility and contributing to the grid via batteries, are set to grow in importance.

Beyond passenger cars, viable business cases in heavy transport are beginning to emerge. These involve very different use scenarios, in which price is a central factor.

Precise management of routes and fleet assets, minimizing en-route charging costs, and maximizing revenues from batteries and charging station flexibility will be key themes.

Register now to to discover the latest insights, emerging trends and upcoming challenges in the EV and EV charging markets.