What are the current key trends in US e-mobility?

In general, the tone in the US is not an aspiration for ‘global leadership’, rather an increasingly positive mix of themes that have a

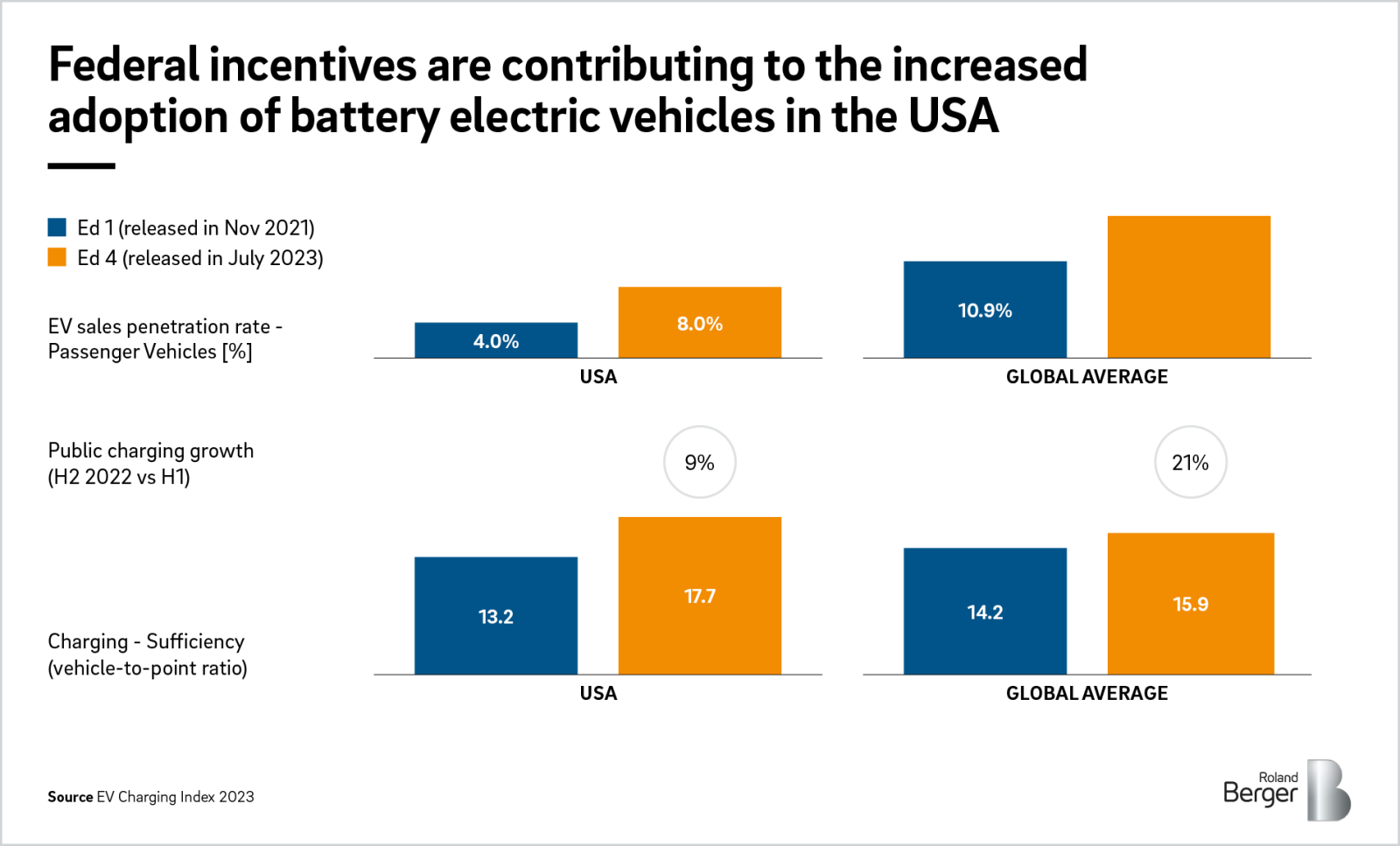

beneficial impact on EV adoption : energy independence, improved performance and better fit for preferred lifestyles. The significant subsidies for purchase in the Inflation Reduction Act (IRA) – up to USD 7,500 – and price cuts from major OEMs are adding to the perception that EVs are entering the mainstream, with charging logistics and experience displacing the traditional concerns of affordability and technology risk. The recent major consolidation around the Tesla charging standard and network is an important step.

More than most other global markets, the US is embracing larger EVs such as Rivian’s R1 range, Ford’s F-150 Lightning and SUV models from existing OEMs. Given their large battery sizes, this necessitates proliferation of DC charging and accelerates obsolescence of many early ‘convenience’ chargers as 7kW/hr has minimal impact on an SUV or truck with a 135kw battery.

How is the EV market evolving?

There is an emerging awareness of the volatility of gasoline pricing versus the relative stability of retail electricity rates. However, as consumers move towards more DC public charging, the rates for those sites are significantly higher than retail electricity, and perhaps not-coincidentally, similar to ‘per gallon’ equivalence with gasoline. That said, most American EV owners do the vast majority of their charging at home at a much lower cost.

The EV sales penetration rate has steadily increased over the last several years, up to 8% of passenger vehicles in the second half of 2022 and moving higher in the first half of 2023. This is still behind the global average of 16% and well below the top countries, but it is a significant increase over the penetration rate of 4% indicated in our first edition, only two years ago. A key driving factor is the variety of new models from OEMs, including a much larger number of lower-cost options, changing the profile of the typical EV owner. The expansion of the charging network is a major facilitator for EV adoption as consumers continue to indicate range anxiety and inconvenience as a major roadblock to adoption.

How would you describe the current state of the US charging infrastructure?

Home charging dominates as most US EV owners have a dedicated garage space and it remains the most convenient and cost-effective charging option. For public charging, charge-point operators (CPOs) are recognizing that consumers want faster charging and a better customer experience. To this end, CPOs are swapping out older, slower chargers for higher-capacity fast chargers and upgrading the user experience, focusing on safety, convenience and cleanliness. None currently meet the standards of the Tesla SuperCharger network. This is evidenced by some OEMs announcing plans to utilize the Tesla network, with others forming a coalition to build their own network.

What role does government policy play?

A large part of the IRA focused on incentives for battery electric vehicles, including direct rebates for the end consumer. These are powerful incentives, lowering the upfront cost of the vehicles closer to traditional ICE vehicles. The infrastructure bill, passed in 2021, contains the majority of federal funding focused on infrastructure development, although the IRA does contain an extension of the investment tax credit on charging infrastructure. It is unlikely there will be more legislation at the federal level and there remains an outside possibility that with a change in administration, there could be a claw-back of some of the IRA funding.

![{[downloads[language].preview]}](https://www.rolandberger.com/publications/publication_image/23_2077_ART_EV_charging_index_deep_dive_USA_Cover_download_preview.jpg)