An update on developments in the global battery value chain, and their implications.

Raw materials: Resilient supply chains

By Wolfgang Bernhart, Isaac Chan, Kyle Gordon and Tim Hotz

How to overcome uncertainties to ensure stable, flexible supplies of critical minerals

The green transition requires a fundamental shift from fossil-fuel-based value chains to a new generation of clean energy technologies based on non-fossil minerals. As a result, demand for lithium, nickel, copper and other critical minerals is soaring. But with supplies struggling to keep up, and risk and uncertainties swirling around supply chains, how can players react? By making their supply chains more resilient.

"Making supply chains resilient is the key to dealing with uncertainties. They must be designed to maintain stability while also being flexible and able to mitigate risk."

Supply chains are changing. Once driven by fossil fuels, today they are increasingly focused on non-fossil minerals to supply a new generation of clean energy technologies. From battery components such as lithium and nickel to copper cabling and rare earth elements, these highly sought after materials are key to the green transition. Indeed, it cannot happen without them.

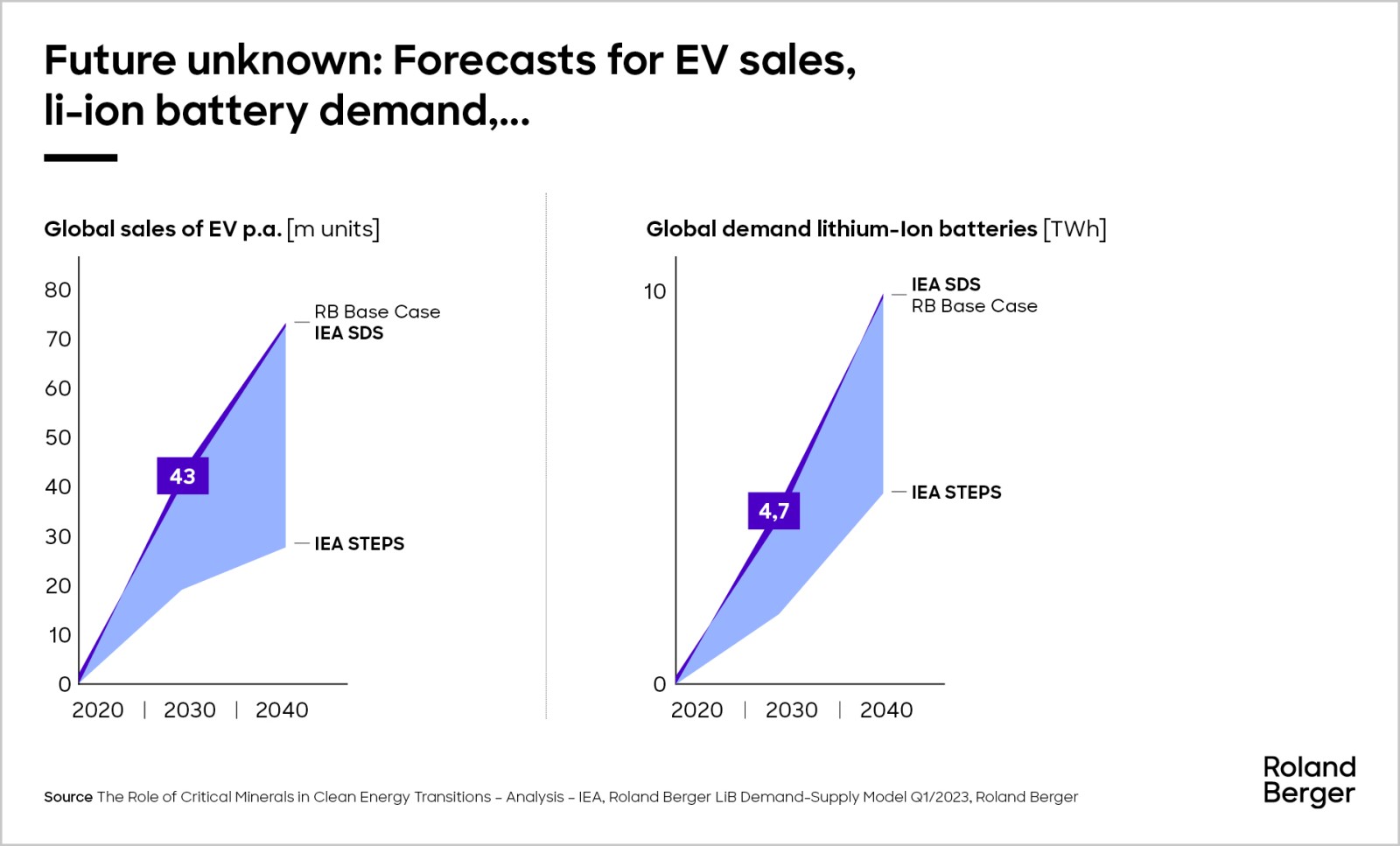

Clean energy technologies consume a large and increasing majority of these raw materials. Yet supplies, especially of lithium and nickel, are barely keeping up with demand. To complicate the situation, there are significant uncertainties and risks around clean energy technologies, such as the sales growth of electric vehicles (EVs).

As such, raw material supply chains will have to remain stable while becoming more flexible to prepare for the unknown. Put simply, they will have to be more resilient. In this new report, we assess the challenges, uncertainties and risks surrounding raw material supply chains, and outline an approach and recommendations to make them more resilient.

Demand and supply

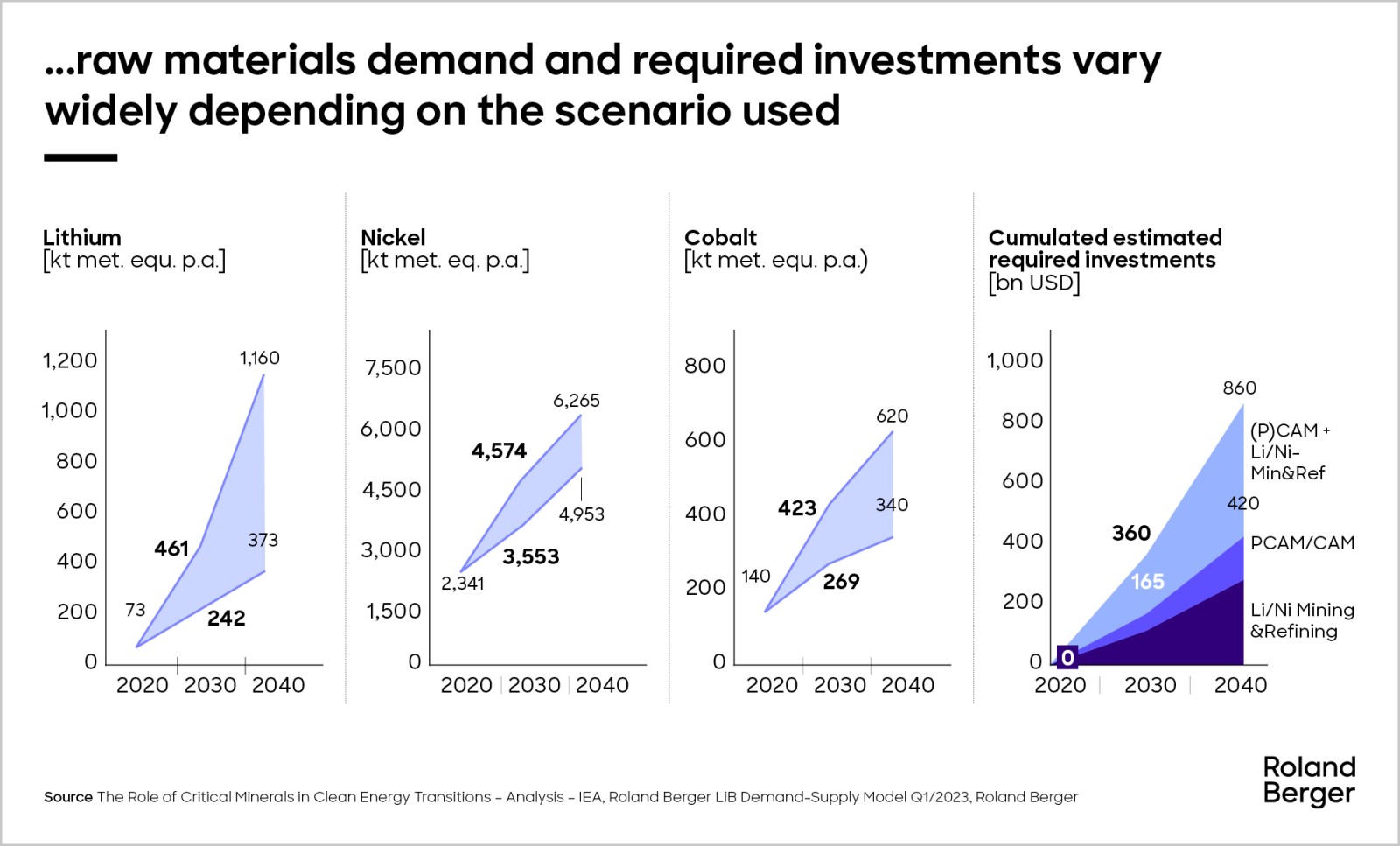

The green transition is driving exponential growth in demand for critical raw materials. Rapidly expanding sectors such as solar energy, wind power, electricity networks and EVs will account for almost 90% of lithium demand by 2040, 60-70% of nickel, and more than 40% of copper, cobalt and rare earth element (in particular, neodymium) demand, according to the International Energy Agency. This represents supply requirement increases of between 1.3x (copper) and 14.6x (lithium) compared to 2020.

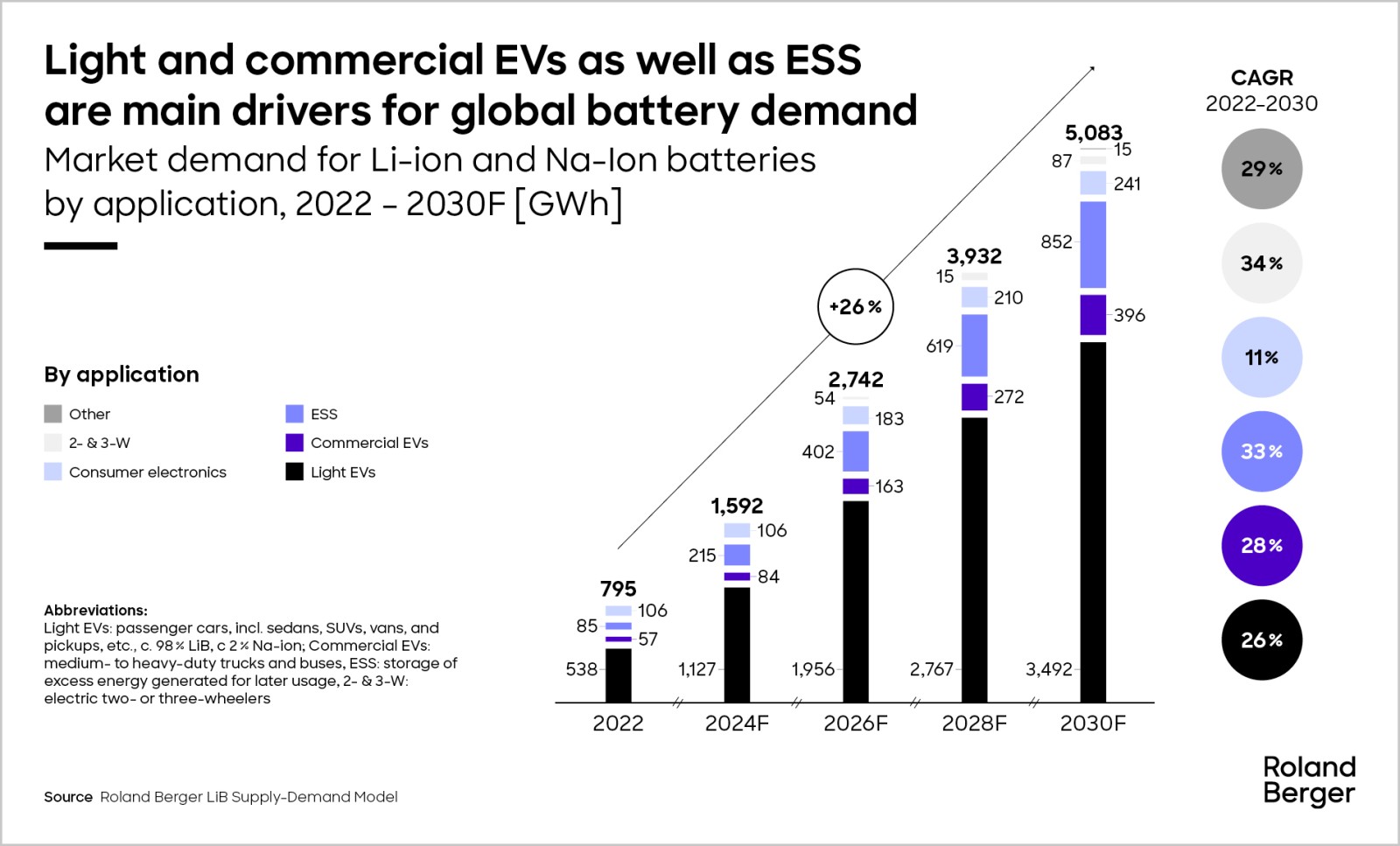

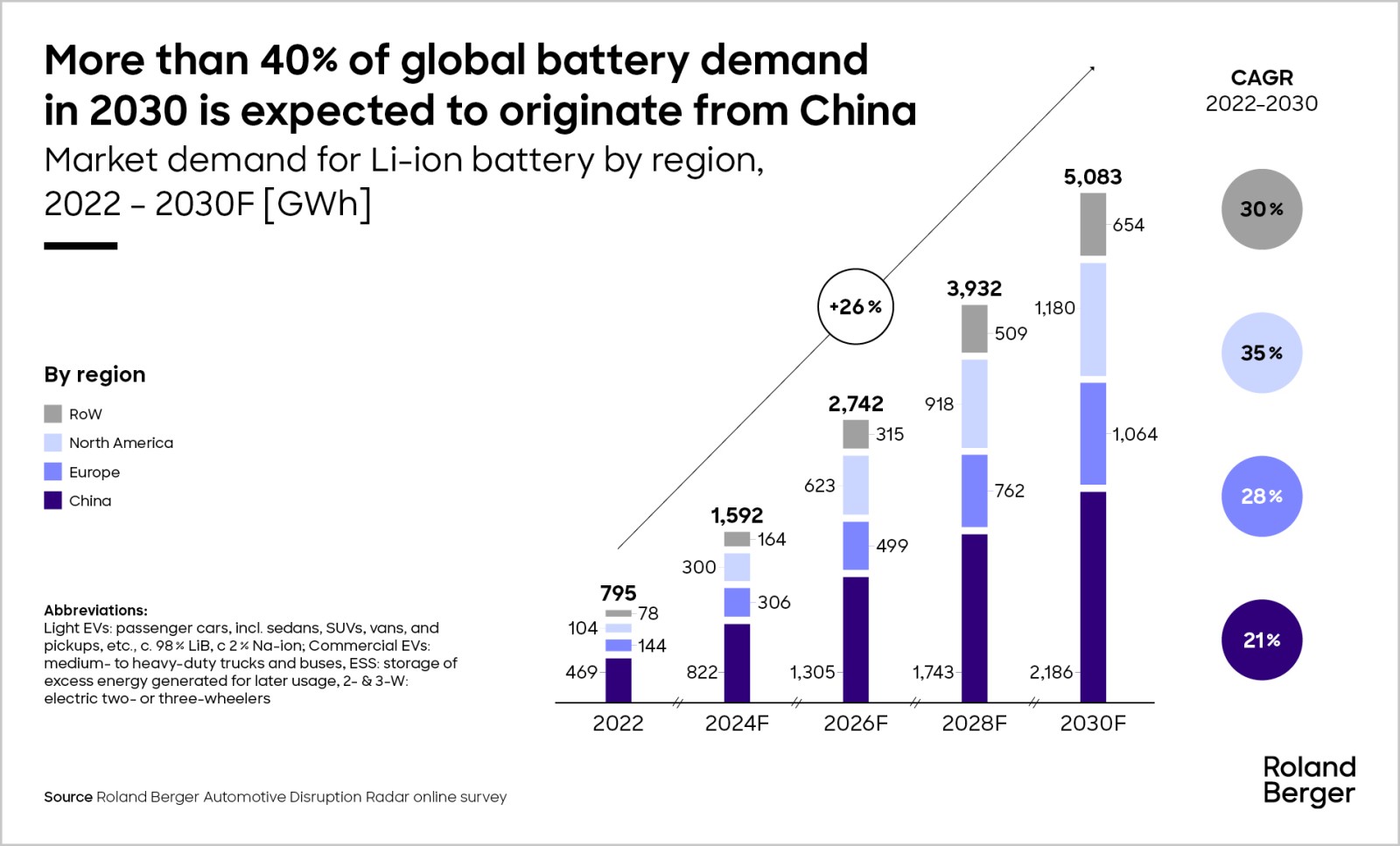

The main driver for these increases is demand for batteries, particularly lithium-ion (Li-ion) cells for EVs and energy storage systems (ESS). From a base of around 795 GWh in 2022, we estimate that market demand for Li-ion and sodium-ion (Na-ion) batteries will soar to almost 5,000 GWh in 2030. China is set to remain the biggest market, and EVs the largest customer. ESS is expected to be the strongest growing segment, with a CAGR of 33%.

The rising demand for key raw materials is expected to seriously test supplies. According to current capacity plans, mined supplies of lithium, nickel and cobalt are forecast to be sufficient through to at least 2030. But gaps are appearing. For example, new mining projects will be required to satisfy 2030 demand forecasts for lithium, with each facing significant obstacles in the form of technology, skills and financing. In the case of nickel, demand is set to reach around 4.9 million tonnes (Mt) in 2030, with overall nickel supplies forecast to hit 5.9 Mt. However, the long lead times involved in setting up conventional new nickel mines in Indonesia, the main producer, could compromise supply estimates.

Uncertainties and risks

These supply concerns are compounded by significant uncertainties affecting the entire supply chain of critical materials. Several factors stand out. First, uncertainty over EV sales has a significant impact on demand for batteries, cathode and raw materials, and investments – estimates for total investments required by 2040 for lithium, nickel and cobalt mining and refining, and production of cathode active materials, vary by tens of billions of US dollars, for instance.

Second, raw material prices cannot be reliably predicted. For example, lithium hydroxide (LiOH) prices averaged around 9.6 USD/kg in 2020. In 2021, they were forecast to remain broadly flat until 2027. But in reality, prices shot up to 72.9 USD/kg in 2022. Third, geopolitics. China manufactures 75% of batteries, and this dominance concerns other countries. But their actions to redress the balance, such as the US’s Inflation Reduction Act, which restricts the use of non-US battery materials, cause more uncertainty. Lastly, deep-sea mining could become a game changer in the supply of nickel and cobalt if the technology can be sustainably developed.

These uncertainties are heightened by the dead time required to implement raw material projects. For example, it may take up to 6-13 years to get a new nickel mine from conception to operation – a risky period during which unforeseen events may render the project worthless.

Our approach to resilient supply chains

Resilient supply chains aim to mitigate against all these challenges. They must stabilize by minimizing the impact of disruptions; increase flexibility to adapt to changing market conditions; improve visibility; enhance collaboration between all parties; and find the sweet spot between acceptable risks and costs.

In the full report, we outline a cyclical, scenario-based approach to resilient supply chains that fulfils all these requirements. It provides the basis for a supply-chain strategy built around stability, flexibility and contingencies – and based on “no regret moves”.

In addition, we present a series of risk containment measures that can be targeted at particular risk types. These include financial hedging, long-term agreements to secure supplies and investments in technology. Secondary risks, such as skills shortages and IP risks, are also considered.

Finally, we outline the five key success factors of resilient supply chains, from defining the “sweet spot” of acceptable costs and risks to ensuring a competitive edge. With roughly half of the projected processed lithium and nickel supply for 2025 reserved by early 2023, it is imperative that raw material players move quickly to implement them.

For more information, please download the full report or speak to one of our experts. We look forward to hearing from you.

Request the full PDF here

Register now to download the full study on "Raw Materials: Resilient Supply Chains" and get some insights on how to overcome uncertainties to ensure stable, flexible supplies of critical minerals.

Further readings

_person_320.png?v=1687234)